Financing the Big Market Delusion — Why the AI Build-Out Puts the Loss on Credit

E15 — Aswath Damodaran (NYU Stern) on why the AI market is arithmetically capped, why lending on an equity narrative breaks corporate finance, and what the corporate life cycle says about risk.

Over the past two years, the AI data‑centre build‑out has moved from being funded primarily out of hyperscaler retained earnings to being financed at the margin with term loans, ABS and JVs. Equity holders still own the upside; for credit, the big‑market AI story is no longer someone else’s bubble — it is increasingly our problem.

I. The arithmetic ceiling and who is long it

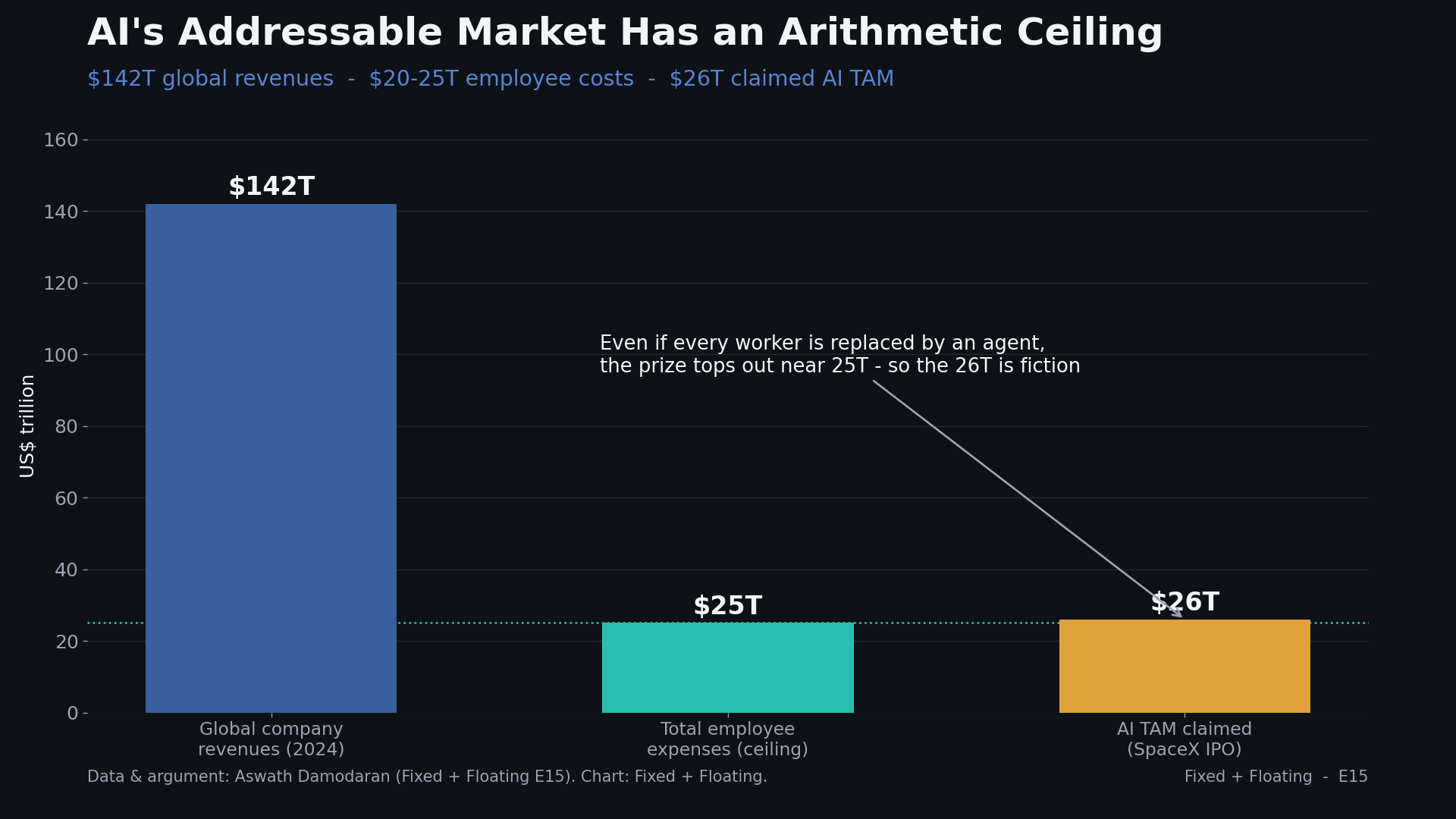

Global listed companies generated roughly 142 trillion of revenues last year. Against that, total employee expenses ran between 20 and 25 trillion. Those two numbers put a hard ceiling on any “AI replaces labour” story: even in the extreme case where every worker on earth is automated away, the prize for AI is bounded by the wage bill, not by whatever number appears in a pitch deck.

When you see AI TAM slides pointing to 20–30 trillion of annual revenue, you are not looking at an aggressive scenario; you are looking at something that is arithmetically impossible in aggregate. Damodaran’s point in his “big market delusion” work is precisely this aggregation problem: each AI company can be priced off an internally consistent story, but the sum of those stories does not fit into any plausible market.

Equity can live with that for a while. If you own a basket of AI names, you only need a handful of big winners to offset the write‑offs. Credit cannot. Credit gets paid a capped coupon on every name and takes a full loss when the story breaks. Once this delusion is being financed with leverage rather than retained earnings, it stops being a harmless equity bubble and becomes a credit problem.

II. How the delusion moves into credit

The funding mix of the AI build‑out has changed. On estimates cited in the pre‑recording brief, 500–600 billion of spend since 2023 has been funded largely from hyperscaler retained earnings. The marginal dollar is now debt, ABS and off‑balance‑sheet JVs. Morgan Stanley expects 250–300 billion of hyperscaler‑related issuance in 2026 alone.

CoreWeave is the cleanest live example of how equity narratives are now setting debt terms. Its unsecured risk trades around 500 bps in CDS, roughly where you would expect a speculative‑grade name with volatile cash flows and heavy capex. At the same time, its asset‑backed infrastructure stack includes an 8.5 billion delayed‑draw term loan, rated A3 / A‑low, and a 3.1 billion syndicated, GPU‑ and contract‑backed facility, both on investment‑grade terms. The whole capital structure tightens as the equity trades up and the backlog narrative improves.

From a lender’s perspective, that is the wrong way round. The unsecured and structurally subordinated pieces are being paid for single‑B risk. The “infrastructure” debt is being paid for as if it were a mature, regulated asset with stable tariffs and demand, not a highly levered bet on early‑stage AI workloads and a fragile ecosystem of counterparties. You are getting IG spreads on assets whose economics are still in price‑discovery mode.

Damodaran’s comment is blunt: if your spread is being set by the market cap and the story, you have lost the script as a lender. You lend against current cash generation and tangible assets, not what equity investors hope the business might be worth in five years.

The real issue is structural. Within the same issuer, the best assets are pledged to the most senior tranches. Unsecured and holding‑company creditors are effectively lending against residual value in a technology stack with short half‑lives and no guaranteed secondary market bid. If the delusion breaks, the losses do not sit in the IG‑labelled paper that funded the GPUs; they sit in the parts of the structure that were priced as if they were one notch above “core infra” but are in fact equity‑dependent residuals.

III. Financing should act its age

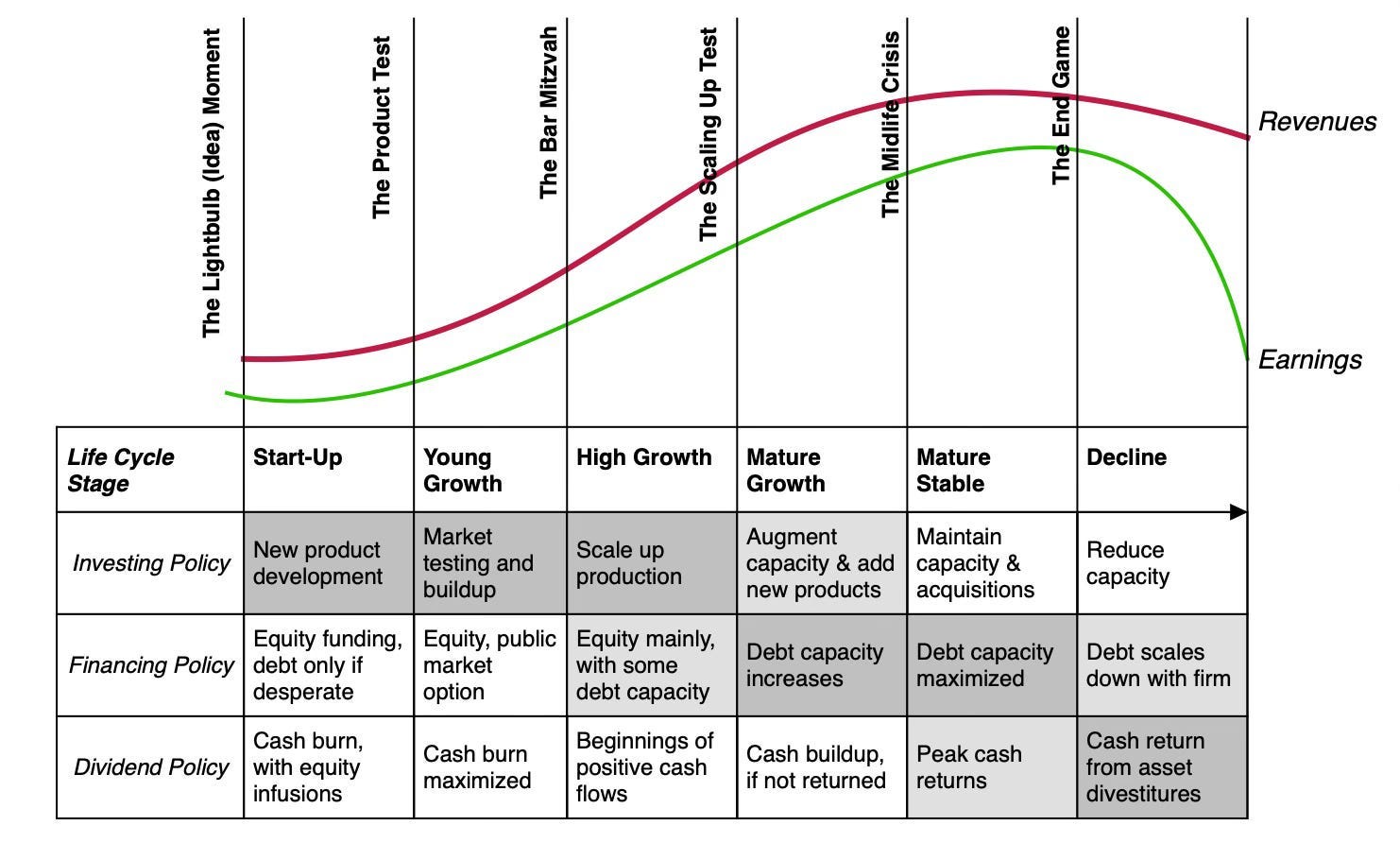

Damodaran’s corporate life‑cycle framework is useful for credit because it forces an honest conversation about when debt makes sense at all. The rule of thumb is simple: the balance sheet should act its age.

Start‑ups and young growth companies: value is almost entirely in future growth. They should be financed with equity or, at most, convertible instruments. Straight debt introduces a hard default condition into what should be an option on growth.

Mature companies: stable cash flows and taxable income justify using debt to exploit the tax shield.

Declining companies: the asset base is shrinking; the debt should shrink with it. If dollar debt stays flat, default becomes a timing problem, not a tail risk.

The AI build‑out is violating this in both directions. Cash‑rich, mature hyperscalers are levering up for a young‑growth story, including off‑balance‑sheet JV exposure that is structurally more fragile than their core businesses. At the same time, young AI companies whose value is pure optionality are taking straight debt — venture debt — to avoid dilution. Damodaran’s view on that is clear: venture debt “violates every rule in corporate finance”, because it puts the entire growth option at risk to save a handful of percentage points on the funding line.

From a credit standpoint, the diagnosis is straightforward. Lending into a business whose value sits mostly in the right tail of a wide distribution is a short‑vol trade. If you are not being paid like a volatility seller — via equity participation, tight covenants, security, or control — you are mis‑pricing your own risk. In that environment, a convertible is the honest instrument. It keeps the cash‑flow drag low for the issuer and gives you upside in the same dimension you are short via the debt.

IV. Overcapacity, leverage, and why some sectors never recover

We also need to be honest about what happens when you build too much capacity on too much leverage.

Damodaran’s distinction between “good” and “bad” overcapacity is helpful. In a young market, creating capacity ahead of demand can deter new entrants and improve long‑run economics. In a shrinking or structurally challenged market, it is the opposite: excess capacity becomes a trap, because nobody wants to buy what you need to sell. His tobacco example — a plant built for five percent growth in a market shrinking five percent per year — is the pure case.

The AI data‑centre build‑out sits between these two poles. Today’s narrative treats overcapacity as strategic. Hyperscalers and specialist operators build ahead of workloads and assume utilisation will follow. The problem is that the funding does not look like growth equity; it looks like term loans, ABS and long‑dated leases with hard payment profiles.

My own working thesis — that overcapacity plus leverage is close to unfixable — matters here. If an industry is oversupplied and mostly equity‑funded, it can consolidate. Equity takes the hit, assets are written down or scrapped, and the survivors earn better returns. Once you add heavy leverage, nobody can afford to be the first to shut capacity and crystallise losses while coupons still need to be paid. Covenants and security packages are structured to protect existing debt, not to allow the economically rational outcome.

For credit, the key is to recognise when a sector has moved into this regime. In that state, “mean reversion” is the wrong default; the right assumption is persistent low returns, forced capex just to stay in the game, and a much higher probability that, when something finally gives, it happens through default rather than through an orderly M&A cleanup.

V. Distress, gap risk, and the pricing vacuum in the middle

On distress, Damodaran’s framework has one point credit should steal and one point it should push back on.

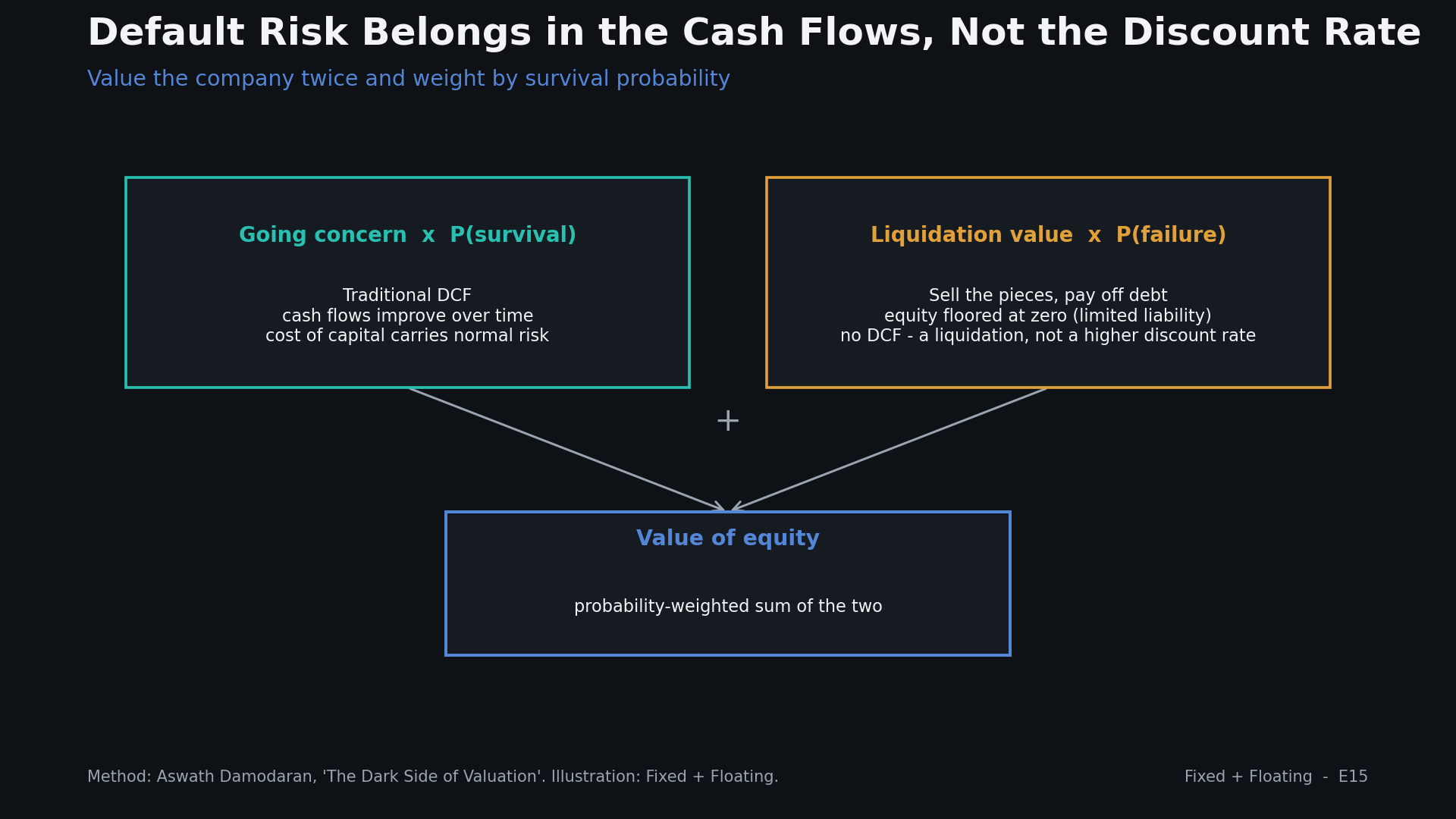

The point to steal is his insistence that default risk belongs in the cash flows, not the discount rate. In his distressed‑valuation work, he values the firm as a going concern with a cost of capital that reflects business risk, not default, and separately estimates a distress or liquidation value and a probability of ending up there. Equity value is survival‑weighted going‑concern value plus distress value times the probability of distress. For equity, the distress leg is usually zero because of limited liability.

Translated into credit language, that is nothing more than PD×LGD done properly: an explicit survival path and an explicit failure path, instead of widening the WACC until the DCF spits out a number you are comfortable with. The discipline is to model what actually happens in default — which assets are saleable, what the forced‑sale haircut looks like, how much value goes to employees, governments and senior secured creditors — rather than hiding those questions inside an arbitrary premium on the discount rate.

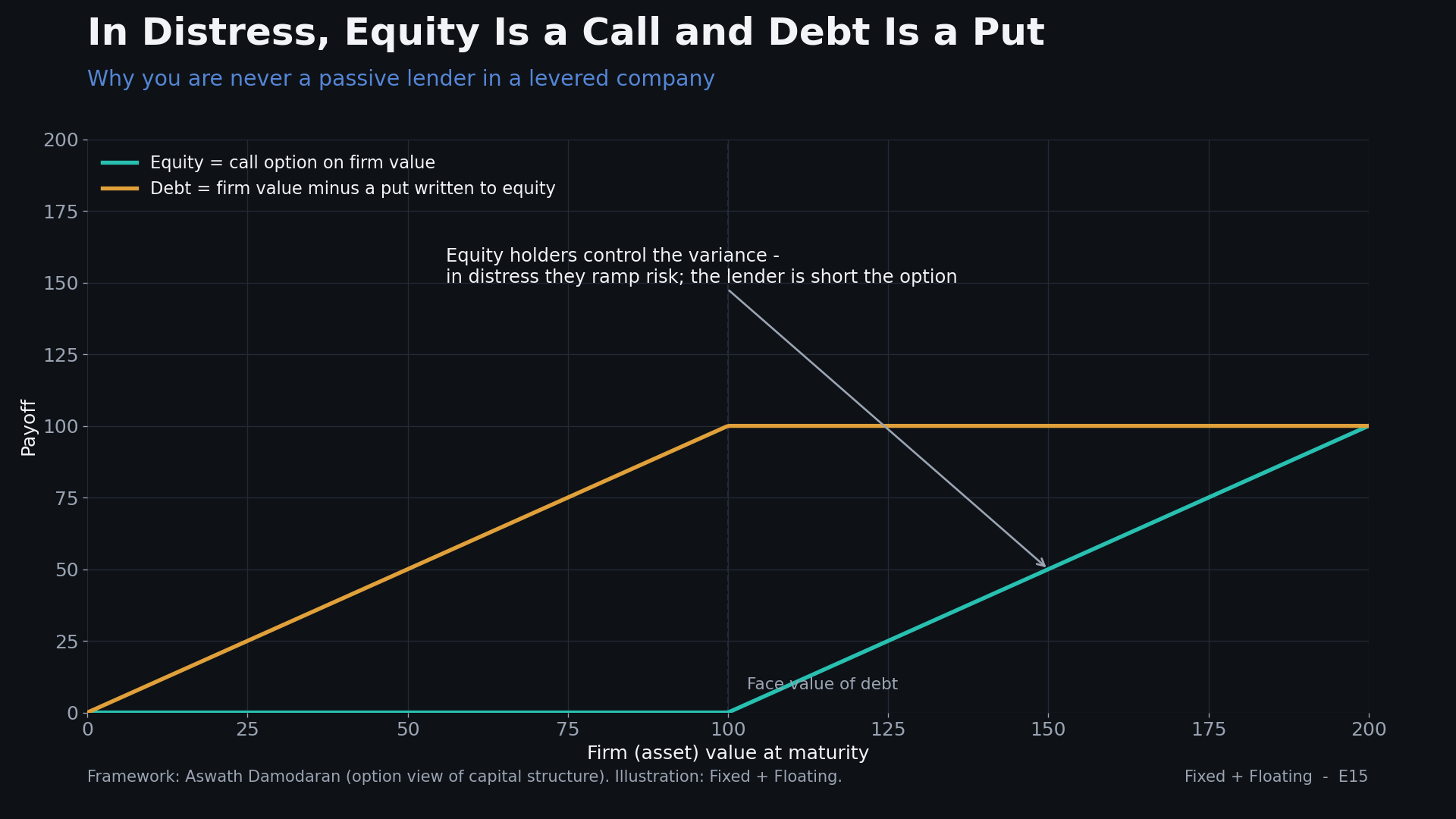

The point to push back on is how far to take the option analogy. In deeply levered firms, equity does behave like a call option on firm value with a strike equal to the face value of debt, and debt behaves like risk‑free debt minus a put on the assets. But the standard implementation of that insight assumes a diffusion: continuous asset‑value paths and well‑behaved volatility. Real defaults do not look like that. They gap. Covenant breaches, ratings actions, liquidity freezes and counterparty reactions create multi‑standard‑deviation moves in a single step.

Credit’s “no man’s land” is exactly where this becomes relevant. Early on, a performing credit prices roughly linearly. Expected loss is PD×LGD, and spread is a reasonable proxy for compensation. As the credit deteriorates, the payoff profile becomes convex and option‑like. Small changes in enterprise value have outsized effects on recoveries, and the instrument’s behaviour depends heavily on path and liquidity. Yet these names still sit in “performing” portfolios, and desks still try to quote them as “+450 over” with a point price.

In that zone, it is more honest to admit that you cannot summarise the risk with a single spread. The right tool is scenario analysis: a distribution of outcomes with explicit recovery and timing assumptions, and an IRR for each. If the range of plausible outcomes spans equity‑like returns on the upside and full capital loss on the downside, you should stop thinking of yourself as a lender and start thinking of yourself as a provider of rescue equity in disguise. If you are not being paid for that, step away.

VI. Pricing vs valuing in AI hardware

The GPU depreciation debate is a good example of where Damodaran’s pricing vs valuing distinction bites credit.

On his numbers, a realistic two‑to‑three‑year useful life for GPUs would increase depreciation charges by roughly 176 billion over 2026–2028 compared with current schedules. That is 176 billion of cost being pushed out of reported earnings, even though the cash has already left. At the equity level, that matters because P/E and EV/EBITDA are still the language most investors use. At the credit level, it matters because leverage, coverage and covenant tests are often expressed off EBITDA, not off cash flow.

If you apply standard leverage metrics (net debt / EBITDA, interest coverage) to a set of issuers whose EBITDA is overstated by aggressive depreciation, you will conclude that balance sheets are stronger than they are. The structure is the same as any late‑cycle capex boom in a commodity: EBITDA looks fine until the cycle turns, because the denominator has not yet recognised the asset decay.

The other issue with AI hardware is cyclicality. In sectors like memory or GPUs, the real drivers are supply, demand and capacity decisions. The P&L confirms the story late. Damodaran’s point is that a numbers‑first investor in cyclicals is structurally lagging the cycle. For credit, the implication is simple: do not wait for the earnings miss. Underwrite against capex plans, utilisation, pricing trends and the technology roadmap. If those are deteriorating while EBITDA is still growing, your metrics are lying.

What i take away from the conversation

For a credit investor, the Damodaran conversation is only useful if it shows up in how you actually run money. For me, the concrete changes are:

Stop letting equity do my PD work. Stock prices, IPO marks and private rounds are telling me almost nothing about default probability or recovery. I will treat them as sentiment indicators, not inputs to the default probability (PB) or the recovery rate.

Be explicit about truncation risk. If I am going to adjust WACC for distress, I will do it as a translation of explicit survival probabilities and failure scenarios, not as a fudge factor. Alternatively, I can keep WACC clean and handle default entirely through PD×LGD and scenario trees. Mixing the two is not acceptable.

Recognise when I’m short volatility. In highly levered, option‑like names — late‑stage venture credits, AI infra SPVs, structurally oversupplied sectors — unsecured and weakly covenanted exposure is economically a short put on the asset base. If I am not receiving equity‑like compensation, I should not pretend it is a carry trade.

Drop “spread talk” in the convex zone. Once a name moves into the performing‑to‑distressed “no man’s land,” I will stop thinking in terms of “+X over” and start thinking in terms of scenario IRRs and recovery distributions. If I cannot produce a credible set of downside scenarios that still justify my entry price, the right position size is zero.

The AI build‑out will not make every credit investor look foolish. But it will be a clean A/B test. Lenders who insisted on acting their age — and made their structures act their age — will lose less. Those who let equity write their underwriting for them will find out what it feels like to be on the wrong side of a big‑market delusion.

Listen to the full episode for Aswaths’s takes on the interconnection of equity and credit markets.

This article is based on Episode 15 of Fixed + Floating, featuring Aswath Damodaran (NYU Stern). The views expressed are those of the speakers and do not constitute investment advice. For more information, please visit https://pages.stern.nyu.edu/~adamodar/.

Fixed + Floating is a credit podcast for institutional investors and finance professionals — exploring the forces shaping global credit markets. Hosted by credit PM Josef Pschorn, the show features conversations with leading voices from investing, research, and academia.

Support Material: