INEOS Quattro: Sector Beta With Shareholder Lifelines

E5: 2027 refinancing without Project One upside (INEOS Deep Dive Pt 2)

In our previous analysis of INEOS Group Holdings, we examined how Project One's €700 million EBITDA catalyst creates a tangible deleveraging path despite permissive documentation and 10x leverage. INEOS Quattro presents the opposite risk profile: equally weak covenants at 8x leverage, but no idiosyncratic catalyst.

Quattro is a pure bet on chemicals sector recovery, with 33% revenue exposure to Asia—the most structurally challenged region. Yesterday’s rally in the 2027s (to 98¢) and 2030s (+5¢) followed news of inventory financing + €200 million equity injection to address the €1 billion Q1 maturity. The refinancing appears resolved—for now—but the question remains whether this preserves bondholder participation in any recovery, or merely delays structural subordination through LME before EBITDA improves. Current pricing (2029s at 80¢, yielding 16%) still reflects binary risk.

Corporate Structure and Formation

INEOS Quattro (ticker: STYRO) was formed in 2020 when INEOS acquired BP’s aromatics and acetyls businesses, combining them with existing Styrolution and INOVYN (PVC) operations. The name “Quattro” reflects four distinct chemical value chains operating within a single restricted credit group:

Restricted Group Assets:

Styrolution: Styrene monomer, polystyrene, ABS (acrylonitrile butadiene styrene)

INOVYN: PVC (polyvinyl chloride), caustic soda, chlorine derivatives, specialty chemicals

Aromatics: Paraxylene, purified terephthalic acid (PTA), benzene, metaxylene

Acetyls: Acetic acid, acetic anhydride, methanol, ethyl acetate, vinyl acetate

Unlike IGH’s vertically integrated olefins/polymers value chain, Quattro’s businesses share limited operational synergies. This structure was driven by opportunistic acquisition rather than strategic integration—a factor that becomes material when considering asset monetization scenarios.

Business Overview

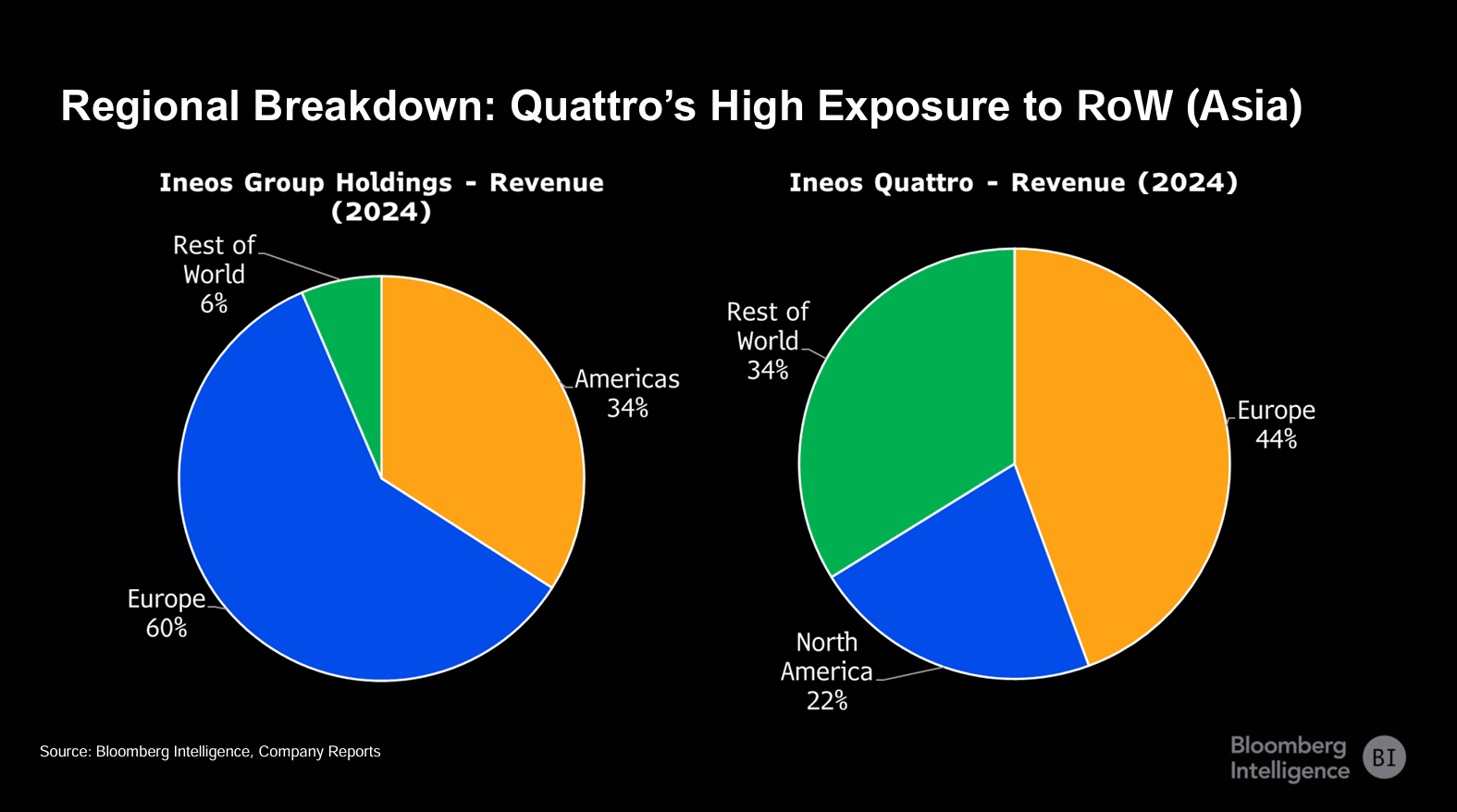

INEOS Quattro operates as one of Europe’s largest specialty and commodity chemicals producers with approximately €8.5 billion in annual revenues (2024). The business mix creates multiple exposure points to construction cycles, automotive demand, and Asian competitive dynamics:

Geographic Split:

Europe: 44%

North America: 22%

Rest of World/Asia: 34%

This Asia exposure is structurally problematic. As Tim Riminton notes: “About a third of Quattro’s revenues come from Asia, where margins are weakest (not just for Quattro—across the sector). Companies with higher Asia exposure have seen more earnings pressure than those focused on Europe or the US.”

End-Market Exposure:

Construction: 60-70% (particularly INOVYN’s PVC business)

Automotive: Significant exposure through ABS and specialty polymers

Packaging and consumer durables: Styrolution products

Industrial chemicals: Aromatics and acetyls feedstocks

The construction weighting creates procyclical earnings volatility. European construction has been in downturn since 2022 due to rate increases and Ukraine war impacts, while China’s property sector—after a decade of double-digit growth—experienced structural collapse.

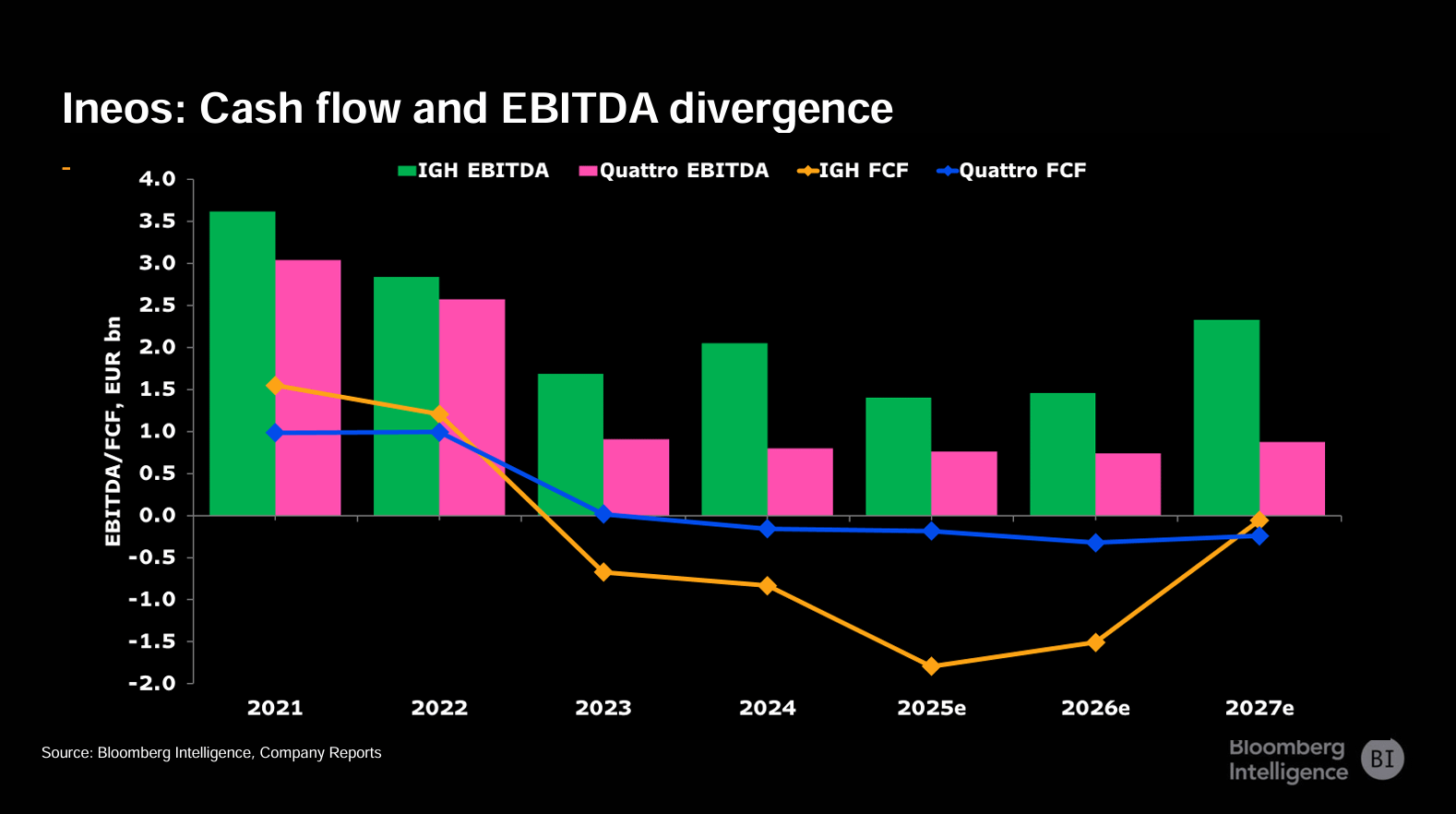

Financial Profile: Distressed Leverage Without a Catalyst

INEOS Quattro has been free cash flow negative for multiple consecutive years and lacks a clear path to FCF generation even in 2027.

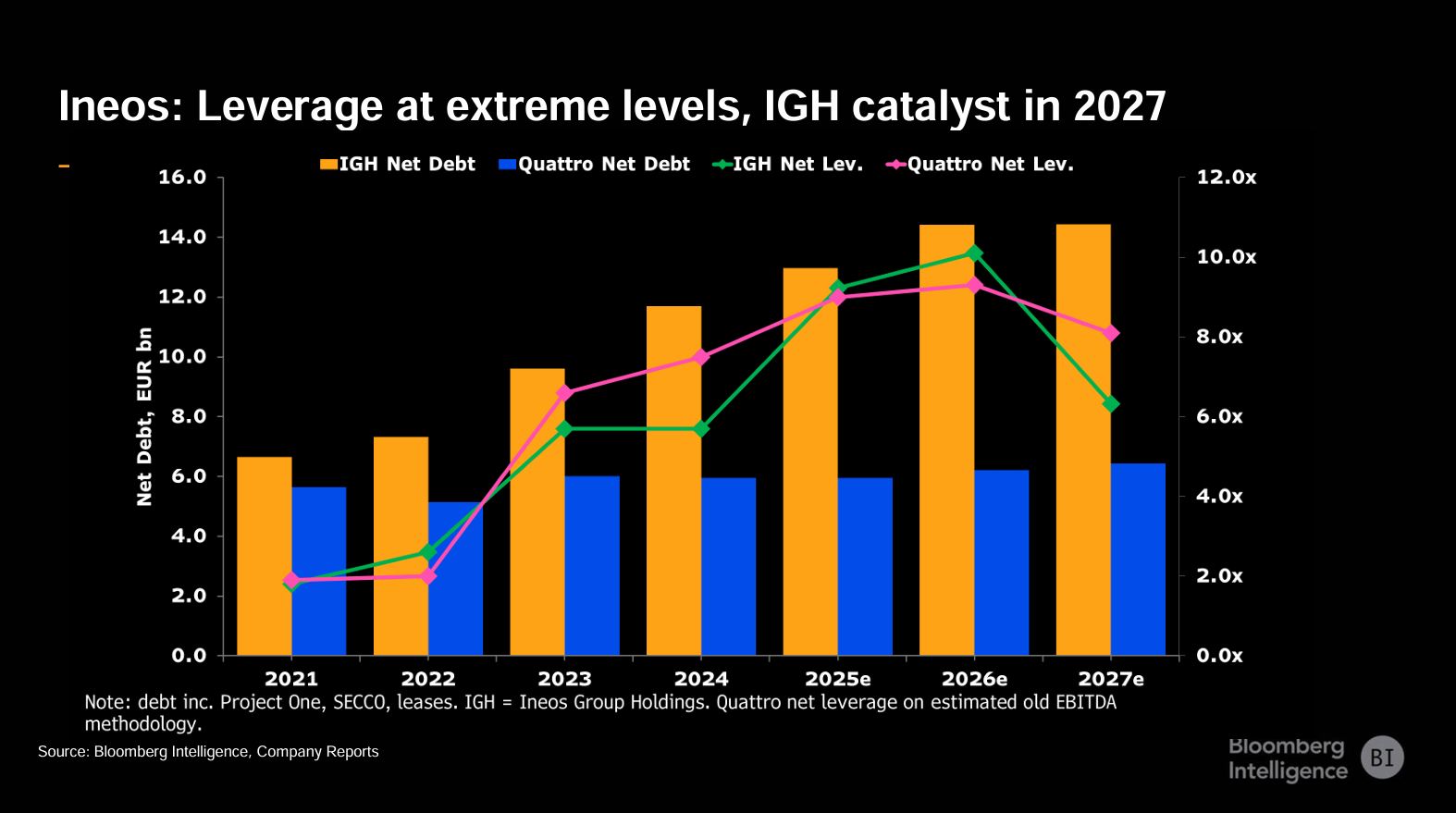

Current Metrics (Q3 2025):

Gross debt: €7.3 billion

Cash: €1.8 billion

Net debt: €5.5 billion (including €313mm leases)

LTM EBITDA: ~€850 million (annualized from 9M25)

Net leverage: 8.0x (Moody’s adjusted: 9.1x)

9M25 operating cash flow less interest: €21 million

Contextualizing the Trough:

2024 EBITDA: ~€900 million

2021-22 peak EBITDA: ~€1.4-1.5 billion

EBITDA decline from peak: 60-70%

The leverage trajectory is unsustainable. Moody’s forecast 16.7x gross leverage for 2025, declining to 8.5x by December 2027—but this assumes material EBITDA recovery that current fundamentals do not support. Bloomberg Intelligence projects Quattro needs approximately €1 billion EBITDA to achieve FCF neutrality, but their 2027 estimate is only €800 million.

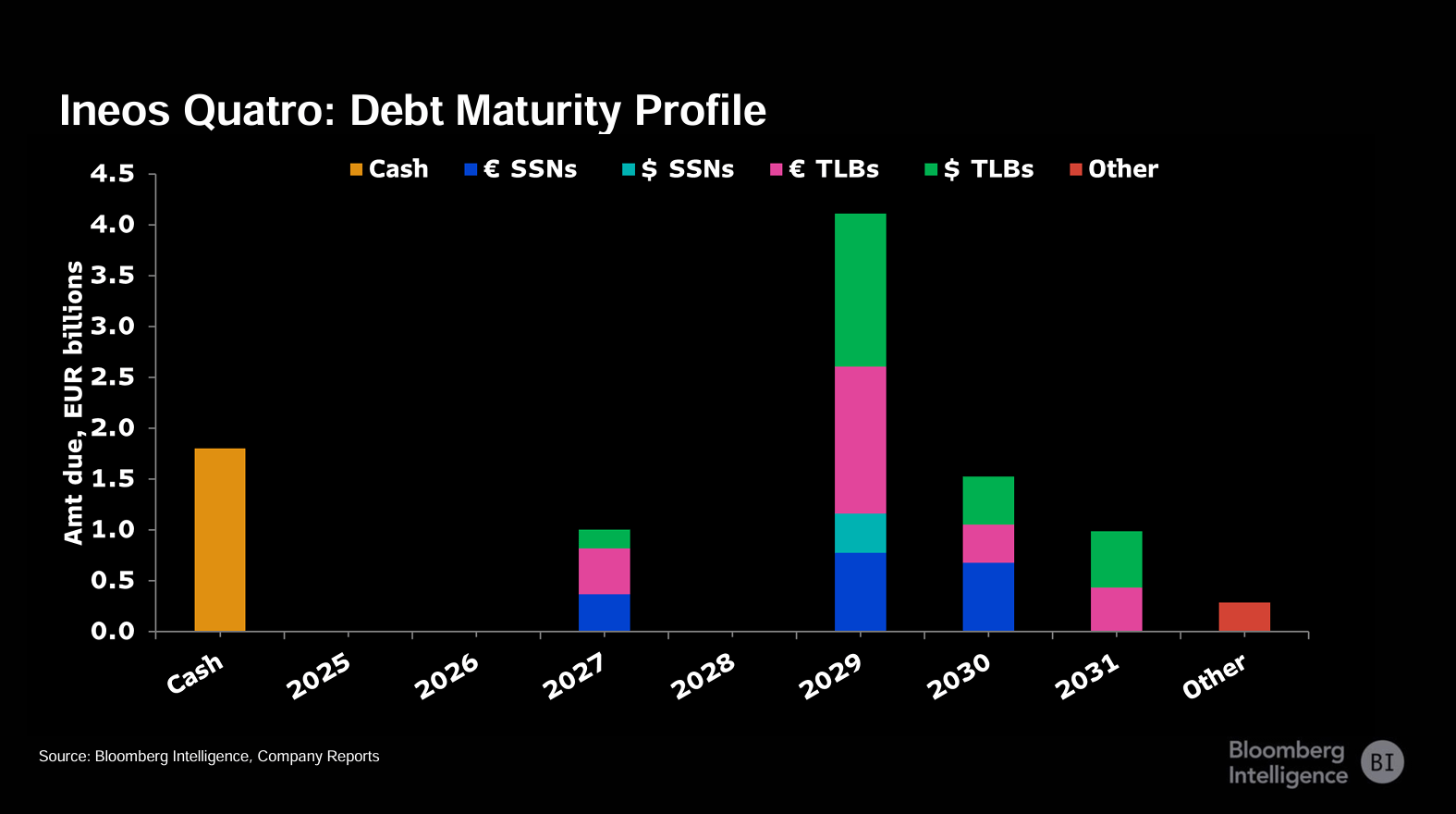

Capital Structure

€7.3 billion total debt (Sep 2025): Senior secured loans €5.1bn (70%, SOFR/EURIBOR+2-4.5%, 2027-31), senior secured bonds €2.2bn (30%, 2.25-9.625%, 2027-30). Net debt €5.5bn vs annualized EBITDA €850mm = 6.5x leverage (company methodology) / 8-9x adjusted. €2.3bn liquidity (€1.8bn cash + €489mm receivables facility undrawn). Weak covenants permit €1.75bn additional debt capacity + €425mm general RP basket + leverage-based UnSub transfers up to €2.5bn+ at 1.75x net leverage threshold.

Upcoming Maturities:

2027: €1.0bn (€365mm SSN 2.25% + €612mm TLB) — due Q1 2027

2029: €3.8bn (€1.3bn SSN 8.5-9.625% + €2.5bn TLBs)

2030-31: €2.5bn (€675mm SSN 6.75% + TLBs)

The 2027 maturity wall is immediate and material. At current market yields of 15-17%, refinancing would consume virtually all EBITDA generation through interest expense alone. Management has indicated plans to use inventory financing and cash, but as Riminton notes: “They probably left it a bit late.”

Current Ratings:

Moody’s: B3, Outlook Negative (downgraded Dec 2025, twice in 3 months)

S&P: BB–, Outlook Negative

Fitch: BB–, Outlook Negative

Moody’s most recent downgrade cited “very high gross leverage of 11.7x” with EBITDA-less-capex-less-interest of just €0.4x—essentially no coverage. They project negative FCF of ~€100 million annually in 2025-26.

Why Quattro’s Earnings Collapsed More Than IGH

The 60-70% EBITDA decline reflects three structural factors:

1. Asia Margin Compression

China capacity additions across Quattro’s product slate created oversupply that disproportionately impacted Asia-Pacific margins. ABS—once a margin contributor for Styrolution—saw prices collapse due to Chinese buildout, forcing closure of Quattro’s North American ABS facility. Aromatics margins compressed 53% in 9M25 due to Chinese PTA oversupply and tariff uncertainty.

Unlike IGH’s ethane-advantaged crackers, Quattro lacks first-quartile cost positioning in Asian markets where it competes directly with subsidized Chinese producers.

2. European Construction Cycle

INOVYN’s PVC business generates 60-70% exposure to construction end markets. European construction entered cyclical downturn in 2022 (rate increases, Ukraine energy shock) and has not recovered. PVC revenues fell 2.5% in 9M25 with EBITDA down 32%. This is cyclical rather than structural—PVC has not faced China oversupply to the same degree as olefins—but timing of recovery remains uncertain.

3. Weaker Product Mix and Cost Curve Position

As Tim explains: “Quattro’s [products] are more commodity-grade with less pricing power...Quattro lacks standout assets like Group Holdings’ Rafnes cracker.” While IGH operates ethane-import crackers that maintained 100% utilization throughout the downturn, Quattro has no comparable cost advantage that insulates margins from commodity cycles.

Documentation: Permissive Structure Enabling Value Leakage

The covenant package mirrors IGH’s weak documentation, creating multiple dilution vectors: incremental debt capacity (€1.75bn), unrestricted subsidiary transfers (€2.5bn+), and permissive asset sale provisions. The INOVYN carveout is particularly concerning. INOVYN represents Quattro’s highest-quality asset with defensible European PVC market position, yet documentation explicitly permits its sale at 2.5x leverage—a threshold Quattro could engineer through strategic debt prepayment immediately before asset transfer.

Asset Value: Is There Enough Left?

Despite four years of FCF negativity, Quattro retains embedded asset value that could attract strategic buyers or support creditor recoveries:

INOVYN (PVC Business): European PVC market leader with ~€2.5 billion revenues. Current downturn is cyclical—driven by construction weakness and energy costs—not structural like the China oversupply affecting olefins. Key recovery catalysts:

New LNG import capacity in 2026 lowering European energy costs

Interest rate cuts supporting construction recovery

EU anti-dumping duties protecting against Chinese imports (already implemented)

Potential Ukraine reconstruction demand

PVC production is energy-intensive (electrolysis of brine), creating operating leverage to energy price declines. With European gas prices normalizing and LNG capacity increasing, INOVYN’s cost base should improve materially. Riminton notes: “PVC’s downturn is not structural—it is a normal cycle...Inovyn and other Quattro assets are well-positioned on the cost curve and could attract strategic buyers.”

Styrolution: Despite margin compression from Asian ABS oversupply, Styrolution maintains scale positions in styrene derivatives serving automotive and consumer durables. Plant rationalization (closures at Sarnia, Thailand, Rheinberg) right-sizes capacity. Recovery depends on automotive cycle improvement and resolution of China tariff uncertainty.

Aromatics: Lowest-margin business (€21mm EBITDA on €2.5bn revenues, 9M25) due to Chinese PTA oversupply. Limited strategic value as standalone; most likely divestiture candidate.

Acetyls: Stable performer (€199mm EBITDA, up 1% in 9M25) with Asian operating rates >70%. Faces Chinese competition but maintains market positions.

A strategic buyer valuing INOVYN at 8-10x normalized EBITDA (€400-500mm mid-cycle) would imply €3.2-5bn enterprise value for that business alone—providing meaningful recovery cushion even after €7.3bn gross debt.

What Needs to Happen: Mid-Cycle EBITDA Scenarios

Bloomberg Intelligence estimates Quattro requires ~€1 billion EBITDA to achieve FCF neutrality (post-interest, post-maintenance capex). Current run-rate of €850mm annualized falls short, and BI’s 2027 projection of €800mm suggests deterioration before improvement.

Mid-Cycle EBITDA Bridge:

Styrolution: €400-500mm (vs €254mm 9M25, ~€340mm annualized)

INOVYN: €400-500mm (vs €166mm 9M25, ~€220mm annualized)

Aromatics: €100-150mm (vs €21mm 9M25, ~€28mm annualized)

Acetyls: €200-250mm (vs €199mm 9M25, ~€265mm annualized)

Total mid-cycle: €1.1-1.4 billion

Current trough: €850 million

Required uplift: 30-65%

This recovery requires simultaneous improvement across multiple independent variables: European construction recovery, normalization of Asian chemical margins, automotive cycle upturn, and energy cost deflation. Unlike IGH’s Project One—which delivers €700mm EBITDA regardless of market conditions—Quattro’s path depends entirely on macro recovery timing.

Policy Support: Speculative Upside

European policymakers face increasing pressure to address competitiveness erosion in the chemicals sector, which employs c.1.2 million workers directly and supports ~30 million downstream jobs. Potential interventions include expanded anti-dumping duties beyond existing PVC measures, targeted energy cost support, carbon border adjustment mechanisms (with mixed near-term effects), and preferential procurement linked to Ukraine reconstruction. To date, policy action has been largely limited to trade defence, with only modest impact on overall sector fundamentals.

That said, recent enforcement activity suggests a more assertive stance by the European Commission. The successful anti-dumping case on 1,4-butanediol—filed by Ineos—resulted in country-wide provisional duties applied at the EU border on imports from China, the US and Saudi Arabia, imposed within a relatively short investigation timeline. While this outcome should not be treated as a direct template for other products, it meaningfully strengthens the credibility of further trade-defence action where material injury can be demonstrated.

INEOS has indicated that additional complaints across other chemical products have been filed or are under preparation, which could lead to further investigations and provisional duties later in 2026, though there is no public confirmation yet and outcomes, scope and timing remain uncertain. Importantly, even if such measures materialise, European producers remain at a structural feedstock and energy cost disadvantage versus the US and Middle East and are increasingly exposed to a shrinking European chemicals market.

For INEOS Quattro, Europe represents approximately 40–45% of revenues, but a materially higher share of earnings volatility, reflecting the region’s higher-cost asset base and its role in setting marginal styrenics pricing. As such, policy support should be viewed as a potential upside catalyst rather than a base-case assumption—capable of improving European profitability at the margin, but insufficient on its own to resolve the sector’s underlying structural challenges.

Thinking About Valuation

This analysis presents factual observations only and constitutes neither investment advice nor a recommendation. Bond prices as of Jan 18, 2026: 2030s ~70¢ (17% YTM), 2027s ~95¢ (8% YTM).

Analog to INEOS Group Holdings, a distressed valuation approach is more sensible than relative value analysis.

INEOS Quattro controls valuable assets—INOVYN’s European PVC leadership, Acetyls’ stable cash generation—but lacks IGH’s catalyst. Mid-cycle recovery requires simultaneous improvement across independent variables: European construction (+€200mm EBITDA), Asian margin normalization (+€150mm), energy cost deflation. The table below illustrates the challenge: €850mm trough EBITDA must reach €1.1-1.4bn for FCF neutrality, requiring 30-65% uplift with no clear timeline.

Unlike IGH—where Project One delivers €700mm EBITDA regardless of market conditions—Quattro requires macro recovery for deleveraging. Chemical peers trading 6.5-9x mid-cycle compress to 4-5x in distressed scenarios, particularly for assets with high Asia exposure and commodity product mix.

The key consideration—similar to Group Holdings—is whether bondholders are kept whole to participate in the upswing or see their claims decimated through liability management exercises. The 2027 refinancing represents the inflection point. A benign outcome (cash plus inventory financing) preserves the existing capital structure, allowing 2029-31 holders to benefit from potential EBITDA recovery to €1.2bn+ and subsequent deleveraging. A coercive outcome destroys this optionality through structural subordination.

Listen to the full episode for Tim’s take on INEOS.

This article is based on Episode 5 of Fixed + Floating, featuring Timothy Riminton of Bloomberg Intelligence. The views expressed are those of the speakers and do not constitute investment advice. For more information on Tim’s research, Bloomberg Intelligence clients can reach him via IB (Timothy Riminton BIO on the Bloomberg Terminal).

Fixed + Floating is the premier podcast for institutional investors and finance professionals exploring the forces shaping global credit markets. Hosted by Portfolio Manager Josef Pschorn, the show features conversations with leading voices from investing, research, and academia. We analyze the technical mechanics of High Yield, Private Debt, and Distressed Situations—from covenant evolution and liability management to macro policy impacts on credit cycles—providing forensic depth for the global fixed-income community.

Support Material:

Fixed Floating Ineos Deck V

915KB ∙ PDF file

05 Ineos Transcript

118KB ∙ PDF file