Significant Risk Transfer Has Quietly Become a $1 Trillion Hedged Market — And It Is Reshaping Bank Capital, Not Bank Origination

E12 – Frank Benhamou (Cheyne Capital) breaks down the SRT market — capital relief mechanics, tranching structures, and and what SRT means for credit origination in the bigger picture.

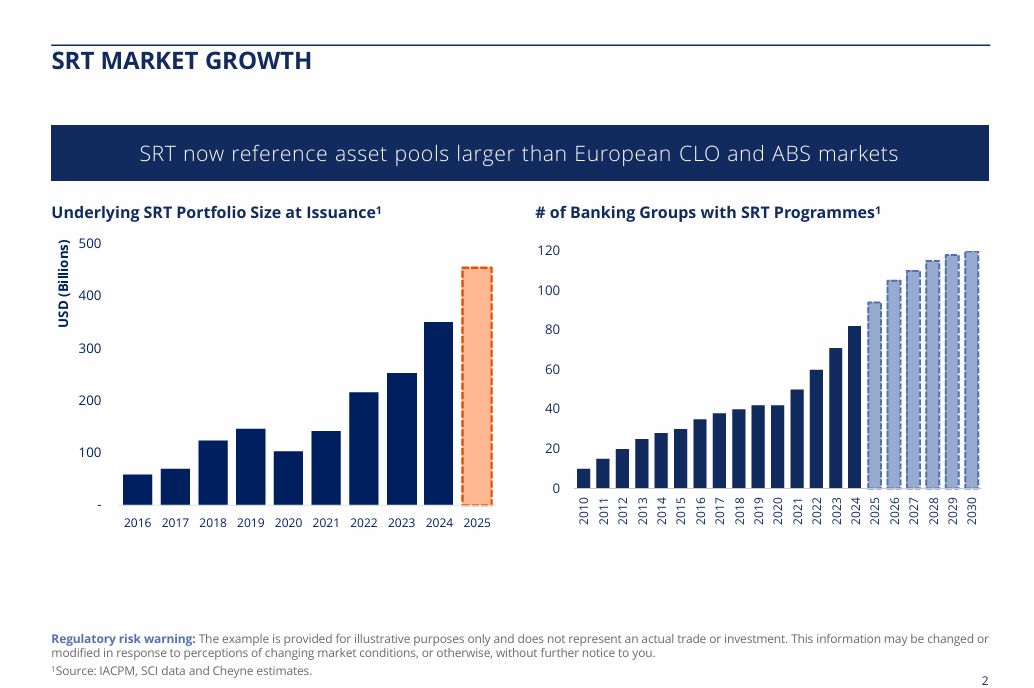

Over the past decade, Significant Risk Transfer (SRT) or credit risk transfer (CRT) trades have moved from niche balance‑sheet tools to a core part of how banks manage capital and credit risk. Estimates from managers, consultants, and regulators suggest that roughly 30 to 35 billion dollars of SRT tranches are placed each year, referencing 350 to 400 billion dollars of underlying bank loans, with outstanding hedged exposure now well above 1 trillion dollars. In Europe, the protected SRT portfolio is already comparable in size to, or larger than, the European CLO and ABS markets; in the US, recent regulatory clarification has opened the door for rapid growth from a smaller base.

This growth has attracted not just asset managers and pensions, but also the attention of supervisors and the Basel Committee, which now treat synthetic risk transfers as a systemically relevant market that needs close monitoring for rollover risk, bank–NBFI interconnectedness, and the quality of “significant risk transfer” itself.

The rest of this piece is a structured walk‑through of the asset class, anchored on the questions an institutional analyst would actually ask: what SRT is and is not, how the structures work, why the market has grown, where the real risks and incentives sit, and what supervisors are worried about as the market scales.

What an SRT Actually Is — And What It Is Not

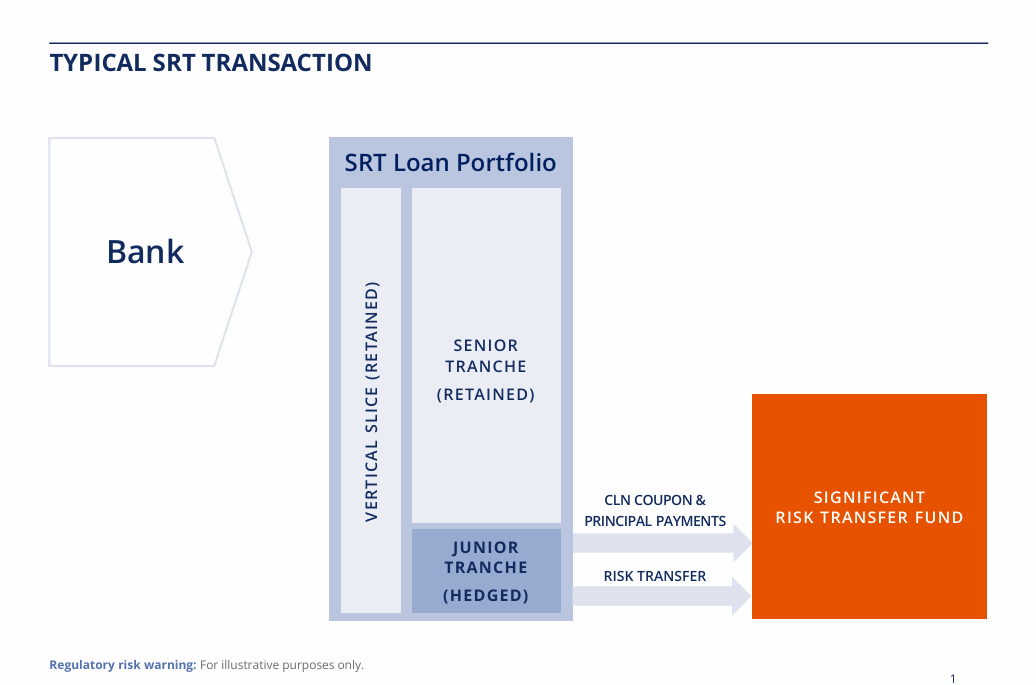

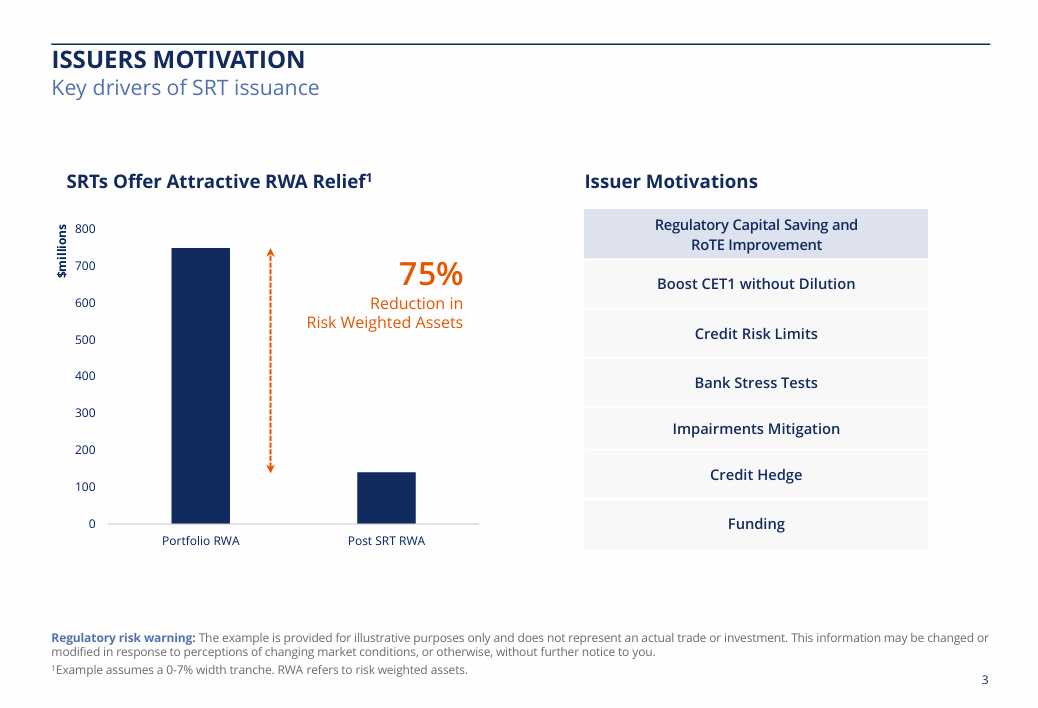

At its core, an SRT or CRT trade is a way for a bank to hedge credit risk on a portfolio of on‑balance‑sheet loans and reduce the risk‑weighted assets (RWAs) the regulator charges against that portfolio. The bank selects a pool of loans — typically corporate, SME, mortgage, infrastructure, project finance, subscription line, or trade‑finance exposures — and transfers the first‑loss or mezzanine slice of portfolio credit risk to an external investor, while retaining the assets, client relationships, and senior risk.

In the canonical example, the bank holds a 1 billion dollar corporate loan portfolio and buys protection on, say, the first 80 million dollars of losses, often corresponding to the 0–7% or 0–12.5% tranche. If the transaction meets the definitional and operational criteria for a synthetic securitisation under Basel and local rules (segmentation into tranches, performance linked to underlying exposures, eligible credit protection, etc.), the bank can recognise a substantial RWA reduction on the protected portfolio.

The economic question for the bank is straightforward: is the coupon paid on the protected tranche lower than the cost of the capital that is freed up? If yes, the trade improves return on tangible equity without issuing new equity or shrinking the loan book; if not, the bank either keeps the loans unhedged or does not originate them in the first place.

It is worth being precise about what SRT is not. It is not a vanilla CDS: there is no requirement for daily margining in fully funded structures, the bank must own the underlying exposures, credit events are narrowly defined (typically failure to pay, bankruptcy, and tightly drafted restructuring), and there is usually no scope to buy “naked” protection on assets the bank does not hold. It is also not a traditional CLO: SRT deals reference assets already originated and held by the bank, with the loans staying on the bank’s balance sheet and the purpose being capital relief and risk management rather than funding or broad loan distribution.

Market Size, Growth, and Who Is Involved

Because SRT is largely a private market, numbers are approximate, but three data points line up reasonably well: manager surveys, law‑firm primers, and the Basel Committee’s recent analysis all suggest annual issuance of roughly 30–35 billion dollars of tranches, 350–400 billion dollars of underlying loans hedged each year, and a cumulative stock of hedged assets above 1 trillion dollars. SRT volumes have more than tripled since the mid‑2010s, and the number of issuing banks has risen into the dozens in Europe and is climbing in North America.

Geographically, the market began as a European phenomenon but is now broadening. European banks — particularly those with relatively tight capital positions — remain the most active, joined by Canadian, US, and a growing group of Central and Eastern European institutions as local rules clarify the treatment of synthetic securitisations. Recent US Federal Reserve guidance and reservation‑of‑authority letters have explicitly acknowledged that well‑structured bank‑issued CLNs can qualify for capital relief, subject to structural caps and strict operational criteria, which is accelerating US issuance from a low base.

On the investor side, the dominant players are specialist credit funds, hedge funds, insurers, and, increasingly, pension plans and sovereign wealth entities, all attracted by double‑digit gross spreads, relatively low expected loss, and low mark‑to‑market volatility. Regulators, including the Basel Committee, have noted that this shift moves risk from regulated banks to non‑bank financial intermediaries (NBFIs), and have flagged the need to monitor bank–NBFI interconnections and leverage in the investor base.

A Sample Trade — What the Capital Relief Actually Looks Like

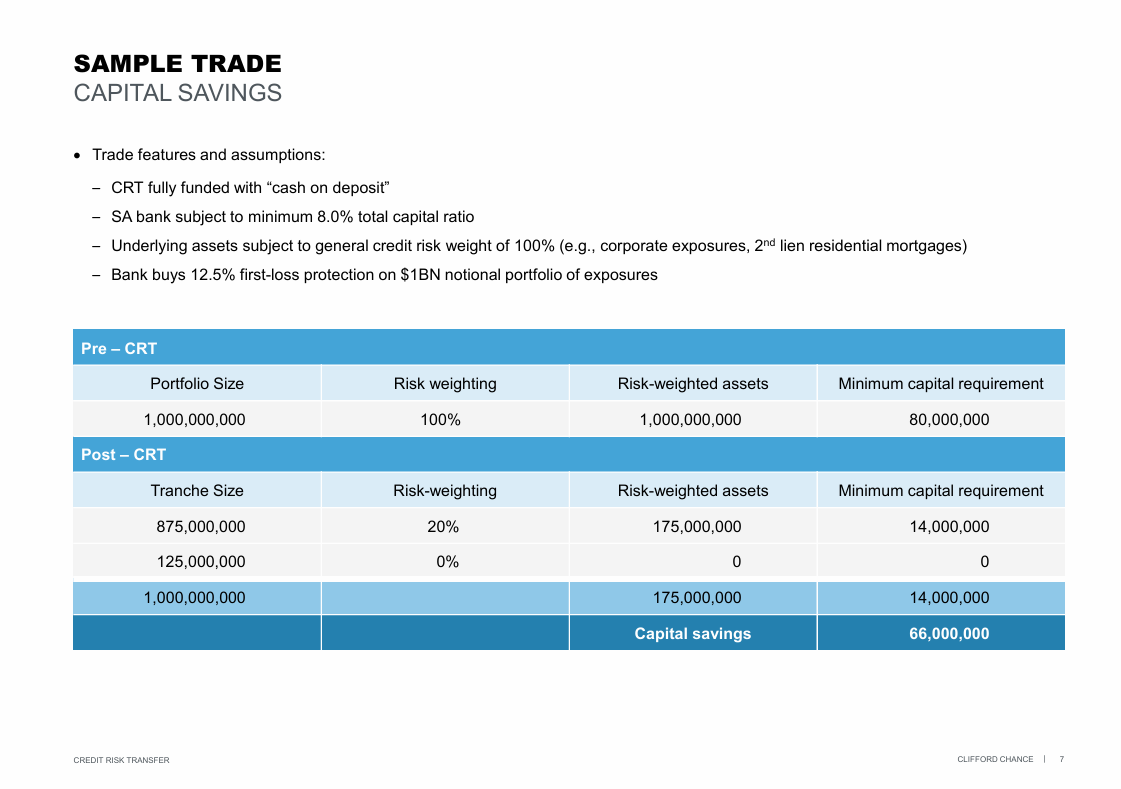

A concrete example from Clifford Chance illustrates how SRT economics work for a bank under a standardised capital regime.

The bank holds a 1 billion dollar portfolio of corporate or second‑lien mortgage exposures, risk‑weighted at 100% under general credit rules, so RWAs are 1 billion and minimum total capital requirement at an 8% ratio is 80 million.

The bank executes a fully funded synthetic securitisation, buying protection on a 12.5% first‑loss tranche (125 million notional) from investors, collateralised with cash on deposit.

Post‑trade, the bank’s exposure is split into:

a senior 875 million retained tranche risk‑weighted at 20%, producing 175 million of RWAs and 14 million of required capital; and

a protected 125 million first‑loss tranche, which receives a 0% risk weight because it is fully hedged with eligible collateral.

Total RWAs fall from 1 billion to 175 million, and minimum capital requirement falls from 80 million to 14 million, implying 66 million of capital “freed up”, against which the bank now pays an annual premium to investors. The trade makes sense so long as the cost of that premium is below the bank’s internal cost of the 66 million of capital it no longer has to hold.

This simplified example captures the basic mechanics behind the “75% RWA reduction on a typical 0–7% or 0–12.5% tranche” that practitioners quote: the hedged first‑loss piece takes the expected credit hits, and the retained senior piece becomes materially cheaper in capital terms.

The Mechanics: Three Main Structures

Market practice and law‑firm guides converge on three principal SRT structures.

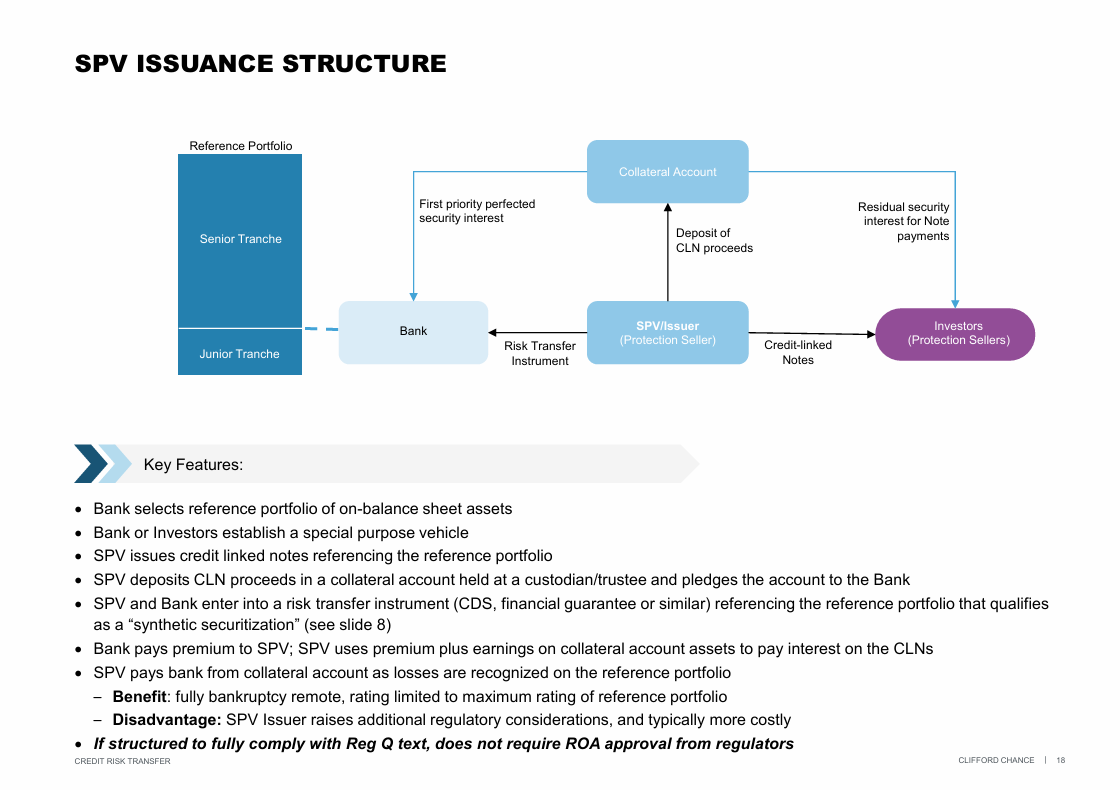

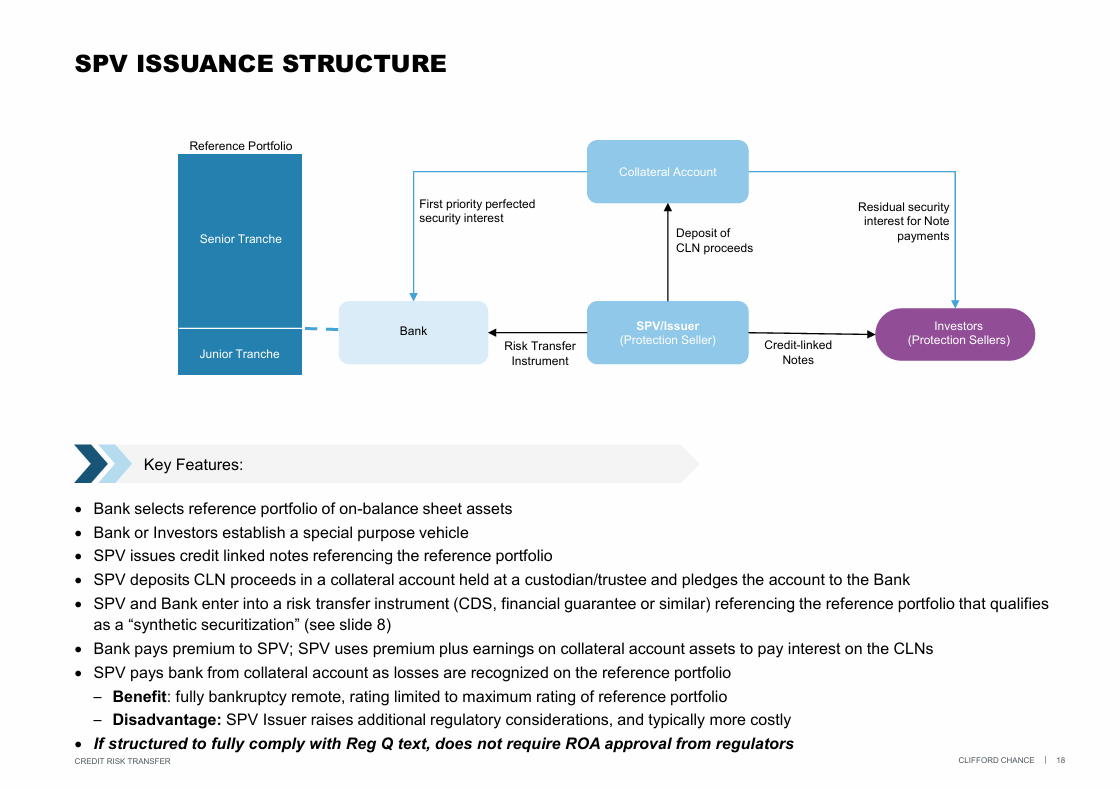

SPV with fully funded guarantee / CDS.

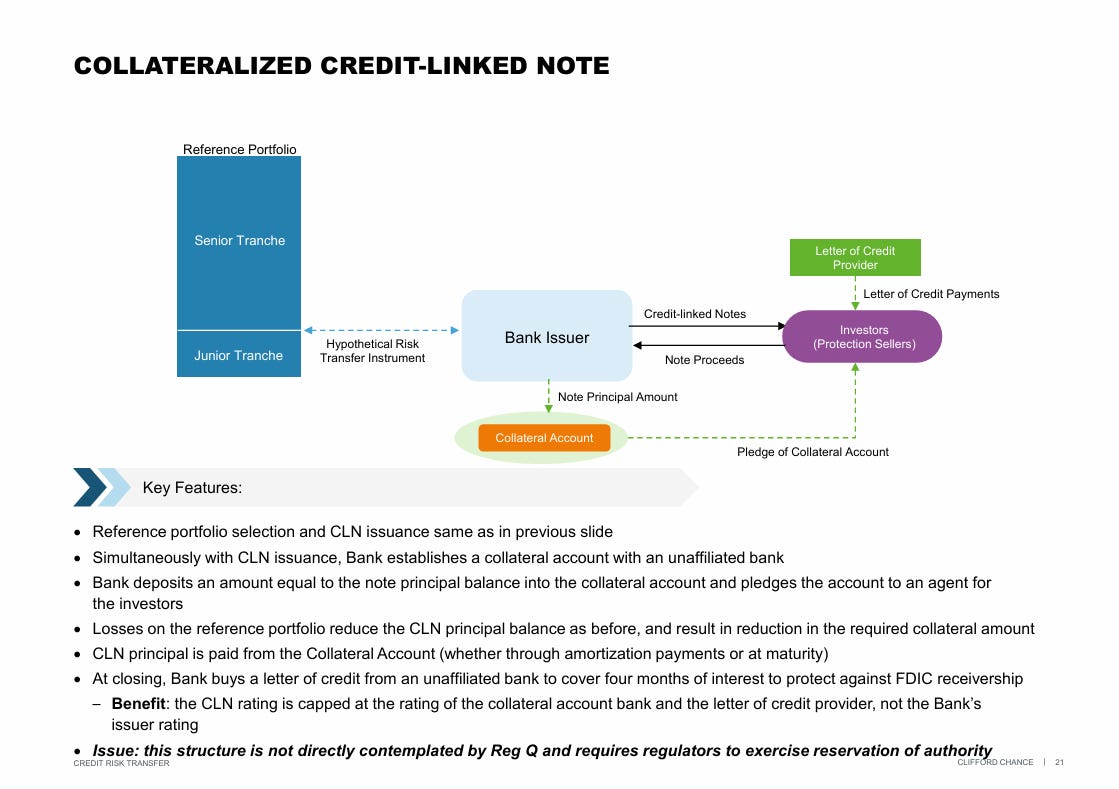

The bank enters into a credit‑protection contract with an orphan SPV, which in turn issues credit‑linked notes (CLNs) to investors and places the proceeds in a collateral account pledged to the bank. Losses on the reference portfolio reduce the tranche notional and are paid out of the collateral, while premiums from the bank plus collateral yield fund investor coupons. This is structurally close to a synthetic securitisation and, when drafted to meet all criteria in Regulation Q (US) or the EU CRR, can deliver capital relief without specific ex‑ante supervisory permission.

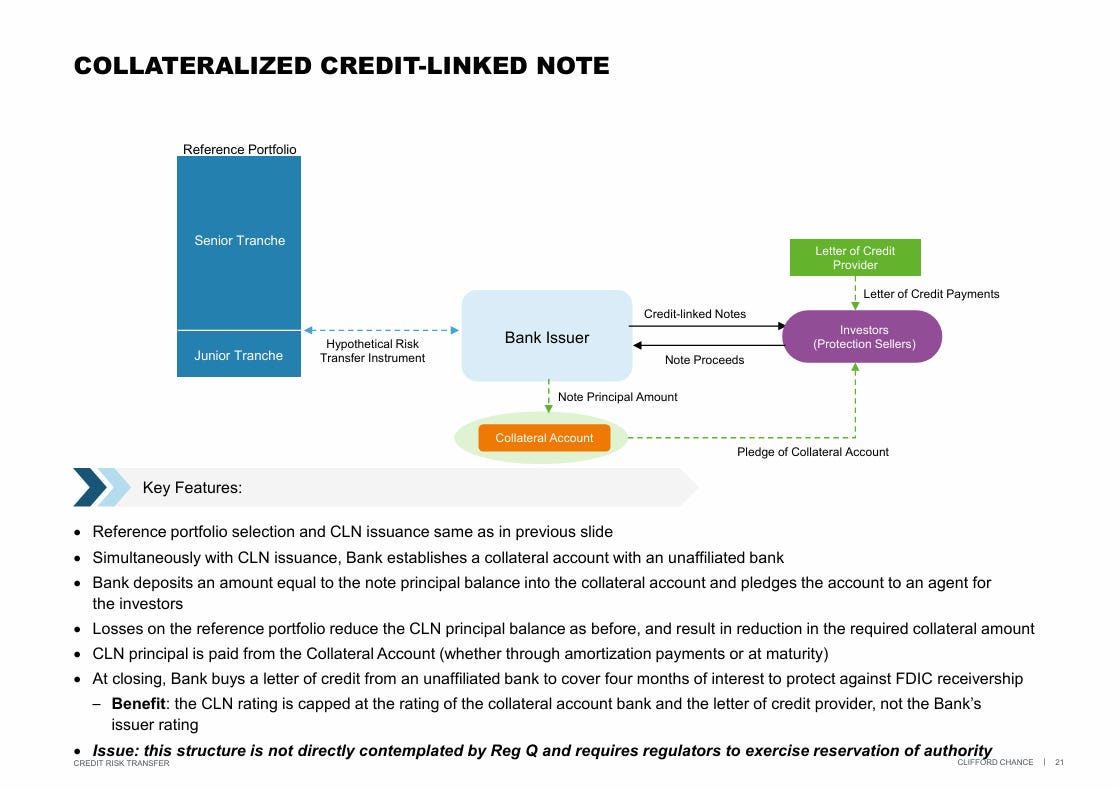

Direct CLN issued by the bank.

Here, the bank itself issues CLNs directly to investors referencing the portfolio, and receives the note proceeds as cash on its balance sheet, with contractual mechanisms to ensure those proceeds function as collateral in an identifiable account. Losses on the reference pool reduce the CLN principal and future coupons proportionally. Because the risk‑transfer instrument can be “hypothetical” and collateralisation is more complex, these deals often require explicit reservation‑of‑authority relief or detailed dialogue with supervisors to confirm capital treatment, and the Fed has imposed caps on the total reference portfolio size for some bank CLN programmes.

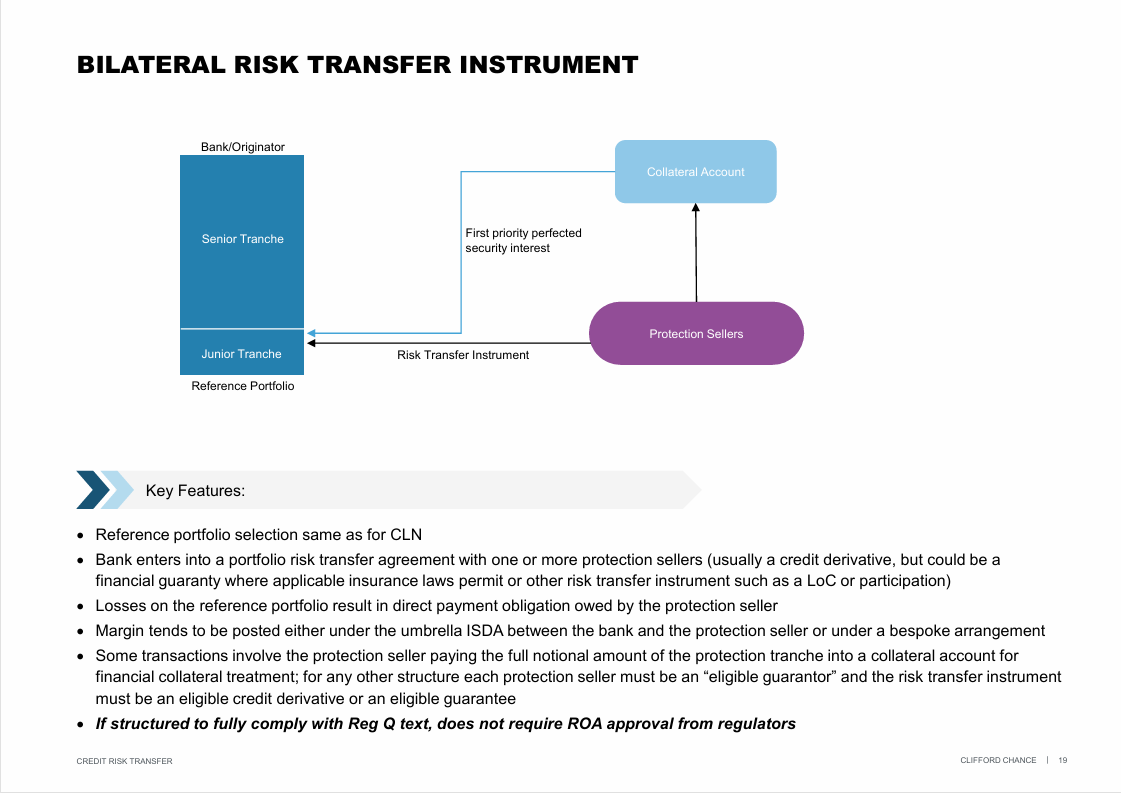

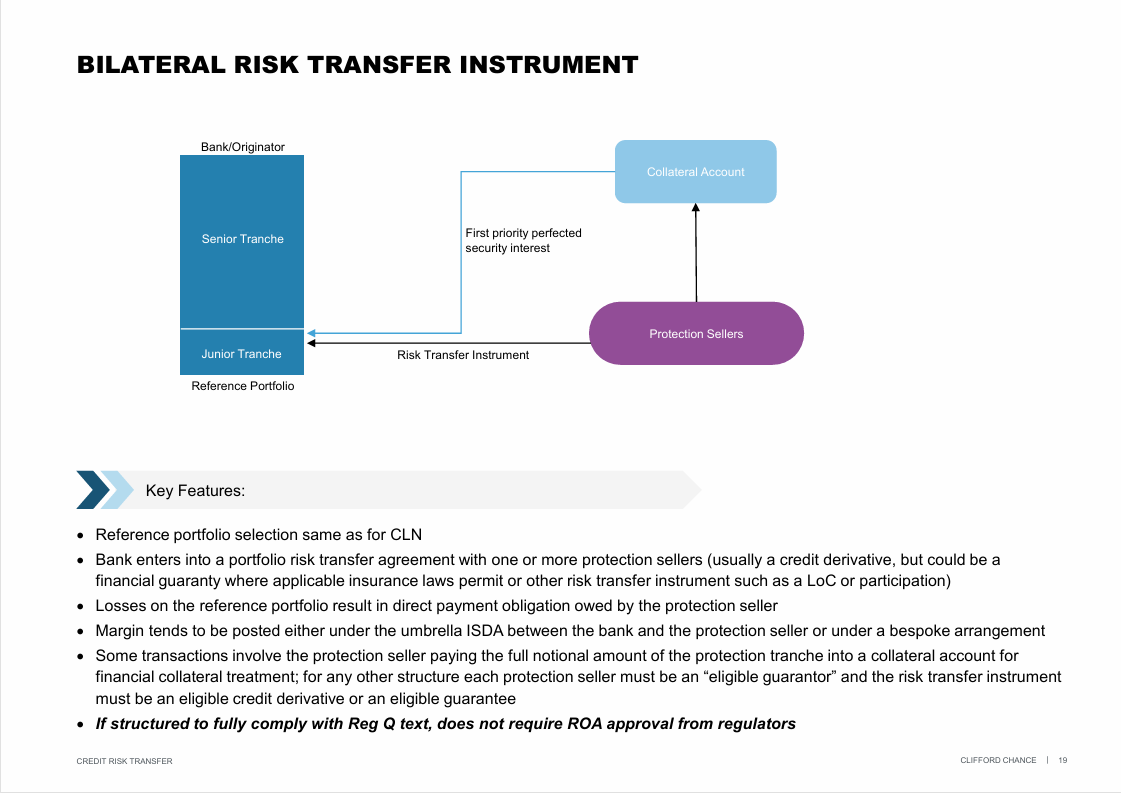

Bilateral funded or unfunded protection.

In bilateral trades, the bank signs a credit derivative or financial guarantee directly with an investor or insurer, which may post full collateral into a pledged account (funded) or rely on its own balance sheet as an eligible guarantor (unfunded). Fully funded bilateral deals can be capital‑efficient but require careful structuring of collateral arrangements and margining to meet operational criteria; unfunded deals can be simpler from a funding perspective but expose the bank to protection‑seller credit and downgrade risk, which UK and EU supervisors explicitly highlight as a prudential concern.

Across all structures, three hard constraints apply: the bank must own the reference assets; the credit protection must meet detailed eligibility tests (e.g., defined credit events, enforceable protection, permissible call features); and the loss measurement process must be robust enough for supervisors to accept that risk has genuinely been transferred.

True‑Up, True‑Down, and Why Losses Are “Real”

One of the distinct features of SRT relative to index CDS is the true‑up / true‑down mechanism. When a loan in the reference pool experiences a credit event — typically failure to pay, bankruptcy, or contractual restructuring — the bank records an initial expected loss and adjusts the protected tranche notional accordingly.

As workout proceeds and actual recoveries are realised, the bank and investor reconcile to a final loss number: if ultimate recoveries are higher than first assumed, the tranche is “trued up” and past coupon calculations are adjusted so that investors are compensated for having had more notional at risk than initially reflected; if recoveries are lower, the tranche is written down further. Law‑firm primers emphasise that this two‑step approach is now standard in capital‑relief trades, precisely to align the protection with the bank’s realised credit experience rather than modelled or index‑based proxies.

For investors, the implication is that performance is tied to realised default and recovery on the underlying loans, not to mark‑to‑market spread moves. That largely explains the low NAV volatility and focus on realised loss rather than valuation noise that consultants and managers highlight as a key attraction of the strategy. The trade‑off is that investors must rely heavily on the bank’s workout and provisioning processes; disputes over loss calculations are rare but can be complex, and documentation has become increasingly granular to minimise room for disagreement.

Portfolio Construction and What Gets Hedged

The SRT market is heavily skewed toward granular, performing corporate and SME loan portfolios, with law‑firm and consultant surveys pointing to large‑cap corporates as roughly half the market by volume, SMEs as another mid‑teens share, and the remainder spread across commercial real estate, mortgages, infrastructure, project finance, subscription lines, and specialised exposures like data centres or trade finance.

Banks choose portfolios based on three lenses:

Size and scalability: reference portfolios are typically at least 1 billion dollars in notional to justify fixed transaction costs and support a programme of repeat deals.

Capital efficiency: banks favour asset classes where the regulatory risk weight is relatively high compared with the bank’s internal view of credit risk, because hedging those assets delivers the most RWA relief per unit of expected loss.

Data and systems: SRT requires deep historical performance data and robust ongoing reporting; some loan books that look attractive on a risk‑return basis simply lack the data infrastructure to support a capital‑relief trade.

Portfolios are intentionally granular: 200–500 names in corporate pools, and sometimes thousands of obligors in SME or trade‑finance deals, so that investors are not overexposed to idiosyncratic single‑name risk within a thin first‑loss tranche. Eligibility criteria, concentration caps, and replenishment rules (where portfolios are revolving) are central to managing adverse selection and ensuring that reference pools reflect the bank’s core lending rather than a dump of troubled names.

Lifecycle, Amortisation, and What Happens When Loans Repay

Most SRT trades run for three to five years in legal maturity, with a replenishment period in the first two or three years during which the bank can replace repaid loans with new eligible assets, followed by an amortisation phase in which the portfolio and tranche notionals shrink in line with loan repayments. BIS and Basel Committee work suggest that, in European data, original maturities tend to cluster around two to four years, with effective investor exposure roughly three to five years once replenishment and calls are taken into account.

During replenishment, portfolio composition is governed by eligibility criteria and reporting: new loans must meet pre‑agreed rating, sector, geography, and concentration limits, and breaches typically lead to exclusion or substitution. After replenishment ends, amortisation may be pro rata across tranches or sequential (reducing senior tranches first), with many transactions including switch mechanisms tied to performance triggers.

This medium‑term profile is exactly why rollover risk matters. SRTs are not permanent capital solutions: when protection matures, the capital benefit runs off unless the bank executes new trades. If a bank is relying heavily on SRT for CET1 optimisation, and the issuance window is closed or prohibitively expensive when existing deals roll off, RWAs will creep back up while the bank may still be holding or originating similar loan books. In normal markets, this is manageable; in a stress scenario, it can become a non‑trivial constraint.

Defaults, Bank Credit Risk, and the Credit Suisse Example

Default mechanics, as discussed, run through the credit‑event definitions of failure to pay, bankruptcy, and qualifying restructuring (forgiveness of principal or interest). The two‑step true‑up / true‑down process governs how losses are allocated and reconciled, with investors ultimately on the hook for realised losses on the reference portfolio up to the size of their tranche.

It is important to distinguish portfolio credit risk from bank credit risk. The investor is primarily taking credit risk on the reference portfolio, but in some structures it is also exposed to the bank itself. In a direct CLN or certain unfunded formats, the bank’s own credit quality and place in the capital structure matter because coupons and return of principal depend on the bank’s ability to pay; in a fully collateralised SPV structure with segregated collateral, that originator exposure is more limited and investors are largely looking to the collateral account rather than the bank for repayment.

The Credit Suisse failure is a useful stress‑test. When Credit Suisse AT1 instruments were written down to zero in the UBS rescue, SRT positions linked to the bank’s loan portfolio continued to perform in line with documentation. In those trades, SRT investors sat structurally senior to AT1 and, in some cases, close to insured depositor level in the creditor hierarchy, with risk exposure driven mainly by the underlying portfolio and collateral, not by the bank’s subordinated capital stack. That episode illustrates what well‑structured, fully funded SRTs can look like in a genuine bank failure, but it is not a universal rule: the degree to which losses on unsecured debt or deposits spill into an SRT depends on where the SRT sits in the capital structure and how it is collateralised.

Pricing, Returns, and the Comparison That Matters

On pricing, banks and investors approach the same trade from different directions. Banks price off capital relief: for a given portfolio, they compute how much RWA is saved by transferring a tranche and ask whether the premium implies a cost‑of‑capital that is below their internal hurdle. Investors price off expected loss and risk‑adjusted return, using portfolio data and stress scenarios to estimate defaults and recoveries and then comparing net spread to other illiquid credit opportunities such as CLO equity, private credit, or mezzanine lending.

Across sources, a broad range emerges: bank‑issued or SPV CLNs on large‑corporate portfolios often pay cash plus 6–11%, with consultant data suggesting long‑run spreads around the high single to low double digits, and expected losses for investment‑grade corporate pools in the 0.1–0.9% per annum range and often lower for balance‑sheet securitisations relative to true‑sale ABS. EBA analyses and law‑firm summaries emphasise that lifetime default rates on balance‑sheet securitisations have historically been materially lower than on comparable public corporate credit indices, although the observed window has been benign.

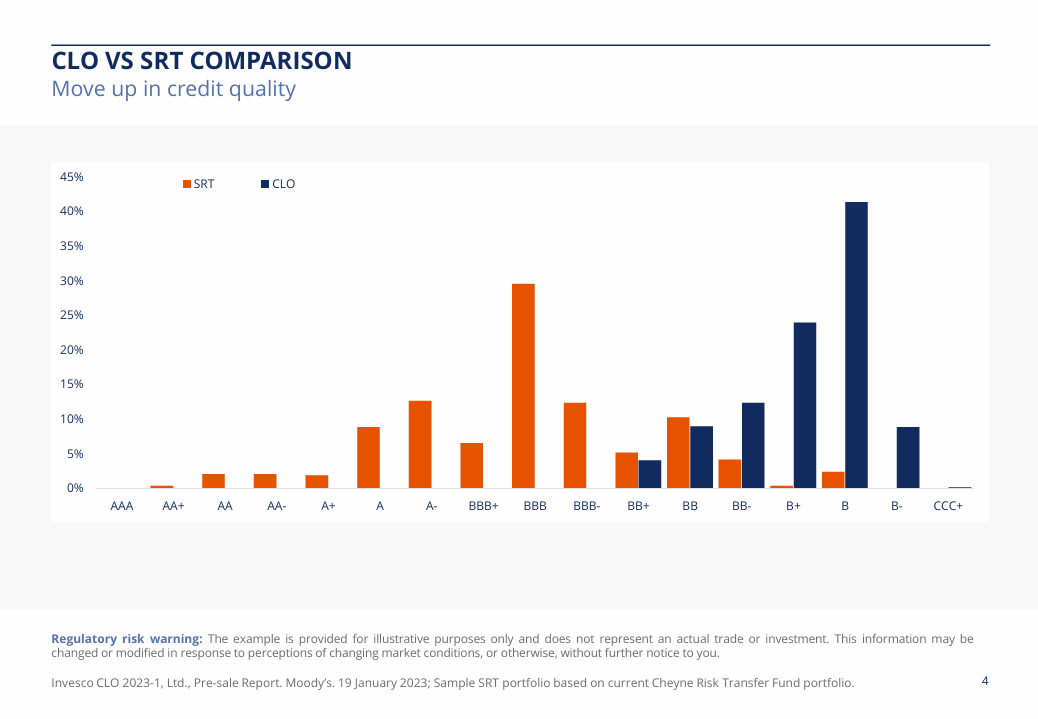

Where SRT is most clearly differentiated is not headline yield but volatility and loss profile. Typical SRT corporate portfolios sit around BBB on average rating, with high granularity and limited exposure to higher‑beta sectors such as leveraged software, whereas CLO equity and some private credit strategies deliberately concentrate in single‑B and BB borrowers with more cyclical cash flows. The result is a return stream that, historically, has exhibited low NAV volatility and limited drawdowns, but also relatively capped upside compared with highly levered or opportunistic credit strategies.

How SRT Behaves Through the Cycle — and What Regulators Worry About

The real question for any capital‑relief product is how it behaves in stress. The COVID episode offered a partial test: spreads on new SRT issuance widened, but banks also reconstituted portfolios, removing the most COVID‑sensitive sectors (retail, hospitality, travel) from new pools and accepting slightly wider coupons on structurally lower‑risk portfolios. That pattern — both pricing and portfolio composition adjusting — is now a standard part of how sponsors describe the product’s cyclicality.

Supervisors, however, are focused on a different risk: rollover risk and procyclicality. If banks come to rely heavily on SRT for capital relief, and the investor bid for new protection evaporates or becomes prohibitively expensive in a downturn, then existing trades will amortise, RWAs will creep back up, and CET1 ratios will fall exactly when credit losses are rising. BIS work and recent Basel Committee commentary suggest that, while average capital relief across issuing banks is currently modest (on the order of tens of basis points of CET1, with only a handful of banks above 1 percentage point), the potential for more material dependence exists as issuance grows.

So far, three factors have prevented rollover risk from becoming acute: strong credit performance in underlying portfolios, the absence of a “maturity wall” where many SRTs expire at once, and still‑limited aggregate dependence on SRT for capital ratios. But both the Basel Committee and the ECB are explicit that rollover and back‑leverage risks are areas for ongoing supervisory attention, particularly as more banks adopt programme‑style issuance and NBFIs fund SRT investments with bank credit lines or repo.

Adverse Selection, Moral Hazard, and Residual Risks

The textbook critique of SRT is intuitive: if a bank can offload first‑loss risk, it may have weaker incentives to monitor credits, and if it has private information about deteriorating loans, it might place those into SRT pools and let investors take the hit. Law‑firm papers and consultant notes acknowledge this concern but emphasise three structural mitigants:

Regulatory risk retention. Banks must retain a material net economic interest in any securitisation or SRT, and cannot reference 100% of any exposure; they take losses alongside investors whenever the portfolio underperforms.

Programme economics and reputation. Most issuers are repeat users who rely on the SRT market multiple times per year. Any evidence of cherry‑picking or under‑disclosure would damage pricing, investor appetite, and, potentially, capital relief; issuance costs and reputational risk make “one and done” behaviour uneconomic.

Documentation and eligibility criteria. Detailed eligibility tests, replenishment rules, and ongoing reporting, combined with due diligence on underwriting standards and historical loss data, give investors tools to push back on portfolio construction and monitor alignment.

That said, none of these mitigants eliminate adverse‑selection risk entirely. Data for SRT portfolios are often less transparent and more heterogeneous than for public securitisations, and regulators point out that imperfect information and complex structures can make it harder for investors and supervisors to detect weak alignment ex ante. The more concentrated the investor base and the more programmatic the issuance, the more important governance, internal controls, and supervisory review become.

Regulatory Scrutiny — What Law Firms and Supervisors Actually Focus On

Regulatory frameworks in Europe, the UK, and the US all revolve around two core tests: definitional requirements (does the trade qualify as a synthetic securitisation or SRT under the rules?) and operational requirements (are there any features that undermine genuine risk transfer?). Law‑firm primers distil the supervisory focus into several recurring themes:

Genuine risk transfer and “no implicit support”. Supervisors want comfort that risk has truly moved from bank to investor for the life of the trade. Features that could re‑route losses back to the bank — implicit guarantees, over‑generous calls, side‑letters, or high‑cost protection that effectively pre‑pays losses — are viewed sceptically and can lead to capital relief being denied or later withdrawn.

Pricing and “high‑cost” protection. Rules and guidance constrain structures where the total premium over the life of the trade can exceed the maximum protection amount, or where coupons are clearly misaligned with expected loss; such trades may be treated as funding or profit‑smoothing mechanisms rather than genuine risk transfer.

Portfolio management, calls, and early termination. Clean‑up, time‑call, and regulatory call options are permitted but tightly circumscribed; investor‑friendly termination rights that might allow protection to disappear when risk increases are generally incompatible with capital relief.

Choice of protection instrument and counterparty. In the US, only certain guarantors qualify as “eligible”, and unfunded guarantees by insurers or corporates must meet detailed tests. UK and EU supervisors explicitly flag additional prudential risks from unfunded protection, including late payment, non‑payment, and downgrade risk, relative to fully funded structures.

In practice, this means that SRT transactions are heavily lawyered, require legal opinions on enforceability, and often involve pre‑issuance dialogue with supervisors, especially for novel structures or direct bank‑issued CLNs. The regulatory mood is not hostile — the Basel Committee explicitly notes that SRTs appear more prudently structured than pre‑GFC synthetic deals — but it is watchful, with an emphasis on substance over form.

Where SRT Sits in the Bank–Private Credit Architecture

At the deal level, SRT does not dictate individual loan terms or create an originate‑to‑distribute model in the way leveraged finance syndication or CLO arbitrage can; origination teams generally structure loans based on client and risk considerations, and SRT desks later aggregate portfolios of already‑originated assets. At that micro level, the incentives remain those of a traditional relationship‑lending bank.

At the macro level, however, SRT has become an important capacity tool between bank capital and the broader non‑bank credit system. By reducing RWAs on existing exposures, it frees regulatory capital that can be redeployed into new lending, which means banks can originate more risk‑weighted assets than they otherwise could under the same capital base. In practice, that can mean maintaining or growing balance sheets under tighter capital rules, or continuing to support core clients without issuing new common equity.

From a system‑wide perspective, what matters less is who originates a given loan and more where the risk ends up, how levered that holder is, and how the structure behaves when stress hits both banks and NBFIs at the same time. The Basel Committee’s recent work makes exactly this point, calling for continued monitoring of bank–NBFI channels, incorporation of SRTs into stress tests, and attention to rollover and back‑leverage dynamics.

What I Take Away From This — And What I Will Be Watching

Three conclusions shape how I think about SRT after layering the practitioner view with law‑firm and regulatory material.

First, SRT is now an institutional asset class. A market that references over 1 trillion dollars of bank assets, has overtaken European CLO and ABS issuance in some segments, and is explicitly analysed by the Basel Committee and BIS is part of the core capital plumbing of the banking system. Documentation standards, regulatory frameworks, and the investor base have all matured to the point where SRT is likely to remain a permanent tool for bank capital management rather than a transient trade idea.

Second, the cycle test is still in front of the market. Historical performance has been excellent: low realised losses on corporate loan pools, stable spreads, and no documented systemic failures of SRT structures through the post‑GFC period, including COVID. But this period has also been unusually benign for credit, with heavy central‑bank support and no full‑scale banking crisis in the core jurisdictions where SRT is largest. We do not yet have a live data point for how SRT issuance, spreads, bank reliance on capital relief, and realised losses behave when both bank capital and NBFI risk appetite are simultaneously under genuine pressure.

Third, rollover risk and NBFI interconnectedness are the variables to watch. The structural elegance of SRT — converting capital pressure into an annual premium — becomes a vulnerability if a bank’s ability to refinance protection becomes correlated with macro stress. At moderate levels of reliance, the arithmetic of tens of basis points of CET1 relief is benign; at higher levels, and with a concentrated or leveraged investor base, the feedback loop could matter for both bank capital and credit supply.

For credit investors analysing banks, that means SRT pipelines, investor concentration, and the quality of risk‑transfer structures now belong alongside traditional CET1 and RWA disclosures in the analytical toolkit. For investors in SRT itself, it means underwriting not just the reference portfolio but also the legal structure, regulatory context, and the potential for regulatory or market regime shifts over the life of the trade.

Listen to the full episode for Frank’s takes on SRTs.

This article is based on Episode 12 of Fixed + Floating, featuring Frank Benhamou of Cheyne Capital. The views expressed are those of the speakers and do not constitute investment advice. For more information, please visit https://www.cheynecapital.com/.

Fixed + Floating is a credit podcast for institutional investors and finance professionals — exploring the forces shaping global credit markets. Hosted by credit PM Josef Pschorn, the show features conversations with leading voices from investing, research, and academia.

Support Material: