Stretch Is Not Cash: The Lesson From Strategy’s Preferred Crash

E16 — Mark Palmer (StoneX) on $22bn of leverage, retail margin calls, and the Digital Credit Capital Framework of Strategy

Over three weeks, Strategy’s flagship perpetual preferred, Stretch, lost more than a fifth of its value. Bitcoin sold off alongside it. Then, last Monday, an 8-K landed, and both the common stock and Stretch ripped back the same day. Most commentary fixated on a single line in the filing: the company had sold 32 Bitcoin for roughly $2.5m. Against a balance sheet holding 847,363 Bitcoin, that is not a portfolio decision. It is a rounding error — 0.004% of the stack. But that sale was the opening move, not the whole hand. In the weeks since, Strategy has sold more than $250m of Bitcoin — its largest disposal on record — with the proceeds earmarked to fund its preferred dividends and replenish the cash reserve behind them. The “never sell” posture is over, and the more useful question is what that shift reveals about how this roughly $22bn structure is actually run under stress.

This piece looks at what actually drove that selloff, how Strategy’s roughly $22bn capital stack is built today, and what the new Digital Credit Capital Framework in the latest 8-K changed for credit investors. The central argument is mechanical rather than conceptual: Strategy has engineered a structure with no covenants and no classical maturity wall through its perpetual preferreds, but remains exposed to one variable — continuous market willingness to fund its securities at a premium to the Bitcoin they represent. As long as Bitcoin retains a bid and Stretch retains liquidity, the true credit risk sits in the capital-raising engine, not in the static balance sheet. The rest of this piece is a structured walk-through of the value drivers, the stack, the selloff mechanics, the new framework, and what I will be watching next.

Three Value Drivers — And One Hard-to-Model Leg

Mark Palmer, the first sell-side analyst to cover Strategy after it adopted its Bitcoin program in August 2020, models the company on a sum-of-the-parts basis, and value accrues in three places. The first is the legacy enterprise-analytics software business, which generates conventional revenue and EBITDA you can attach a standard multiple to; it is small in the overall story, but not zero. The second is the Bitcoin treasury itself, whose projected value is driven by how much additional Bitcoin the company accumulates over time and by the assumed Bitcoin price at the valuation horizon. The third — and the controversial one — is the value created by the treasury activity itself: repeatedly selling securities at a premium to underlying Bitcoin, reinvesting the proceeds into more Bitcoin, and lifting the Bitcoin-per-share metric.

All three legs are ultimately hostage to market confidence. If Strategy’s securities lose their premium and capital-markets access dries up, the engine stalls even though the collateral pool — 847,363 Bitcoin, unchanged through the episode — is exactly where it was.

The treasury-activity leg is the hardest to model cleanly because it presumes the company can, on repeat, raise equity or equity-linked capital at rich valuations, use the proceeds to retire liabilities or buy Bitcoin at distressed levels, and capture a discount on the liability side without permanently raising its future cost of capital. That last step is where most corporates meet reality. Retire converts at 40 cents on the dollar and you book a one-off deleveraging gain, but the next issue prices wider because investors have just watched you equitize or buy back debt in distress. The discount captured on the old paper has to be weighed against the refinancing penalty on the new; the net effect is usually balance-sheet deleveraging, not a clean arbitrage.

Strategy’s bespoke BTC yield, BTC gain and BTC dollar gain metrics were built to quantify this treasury-activity value, but Palmer expects the company to migrate toward a “net BTC yield” framework that better reflects a capital structure now dominated by perpetual preferred rather than converts. For credit investors, that modeling difficulty is precisely why the focus belongs on the robustness of the capital-raising engine, rather than hard-coding treasury activity into a DCF.

How the Stack Actually Works — Debt, Prefs, and Waterfall

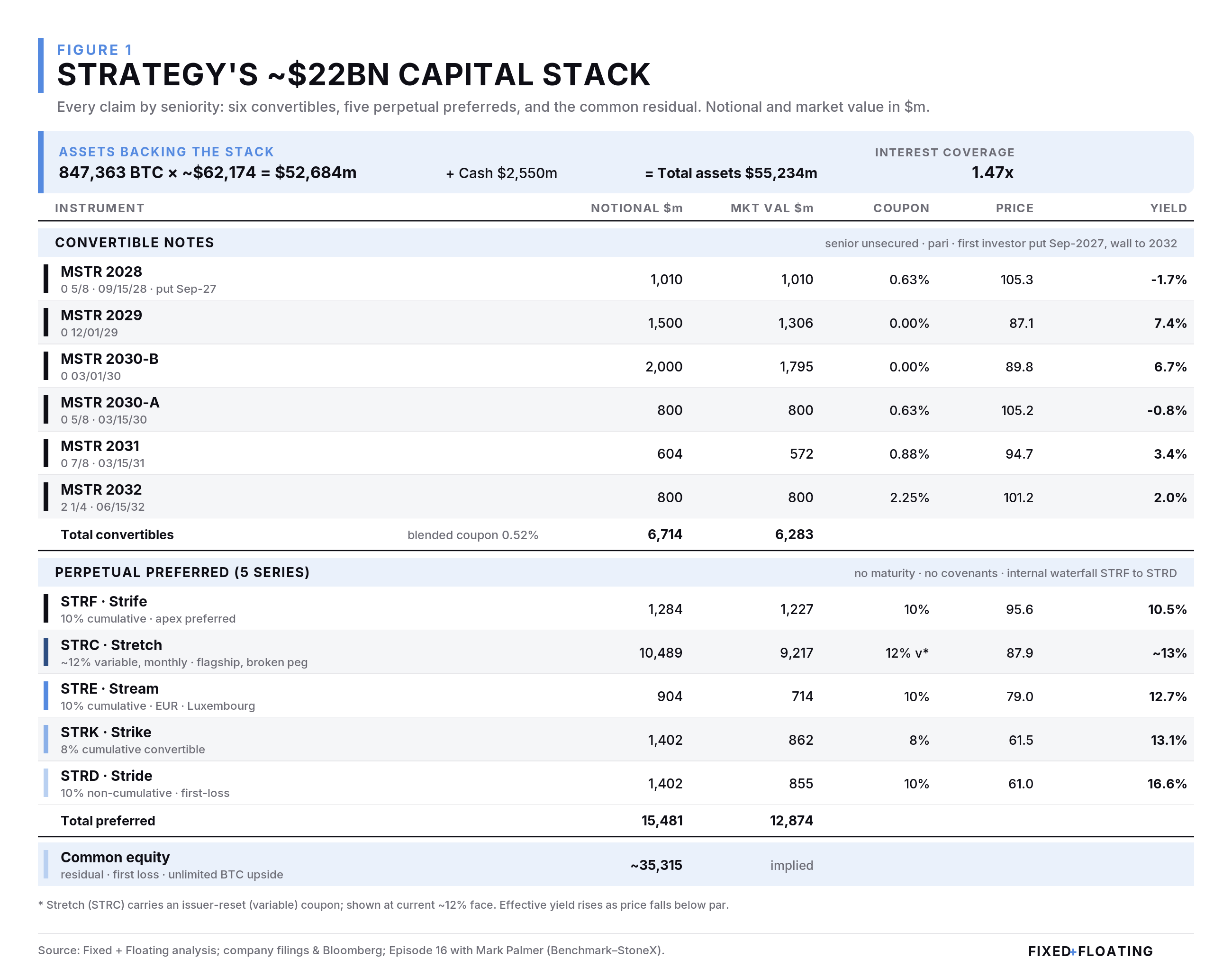

My model and Palmer’s account together map a capital stack that is less “debt above, preferred below” boilerplate and more a deliberately tiered structure aligned to Bitcoin volatility. On the asset side, it anchors on 847,363 Bitcoin — about $52.7bn at spot — plus $2.55bn of cash, against $22.2bn of claims at par. Interest coverage is a thin 1.5x, which tells you the model is not built to service debt out of earnings; it is built to be refinanced and compounded.

The hierarchy runs as follows. At the top sit convertible notes of $6.71bn — senior unsecured, pari among themselves, and ahead of all preferred. Six tranches mature between September 2028 and June 2032, with the first investor put in September 2027. The blended coupon is just 0.52%, and two tranches carry a 0% coupon: interest expense is not the risk. The risk is the wall of principal that must be addressed over a roughly four-year window, and the 2029/2030 tranches trading in the high-80s tell you those are the busted, credit-like lines.

Below the converts sit five series of perpetual preferred totalling $15.48bn, and there is a genuine waterfall inside that layer. STRF (Strife), the apex $1.28bn line, is 10% cumulative with real teeth — unpaid dividends compound and step to 18%. STRC (Stretch) is the $10.49bn giant, a variable-rate (~12%) monthly-pay instrument engineered to peg $100, now trading near 88 as a broken-peg, high-supply line. STRE (Stream) is a €904m euro-denominated 10% cumulative, junior to STRF and STRC. STRK (Strike) is an 8% cumulative convertible, effectively a fixed-income claim plus a deep-out-of-the-money perpetual call. STRD (Stride) is the junior-most: 10% non-cumulative, minimal protections, the structural first-loss piece just above common. Below all of it sits the common equity — the residual, absorbing first loss and capturing unlimited Bitcoin upside.

Two design choices stand out. First, the only fixed maturity in the entire stack is the convert wall; everything else is perpetual, which pushes true refinancing risk into 2027–2032 and hands management discretion over when and how to meet it. Second, the preferred layer behaves like quasi-permanent capital: no covenants, no Bitcoin-linked collateral triggers, no forced refinancing, and non-dilutive to common while outstanding.

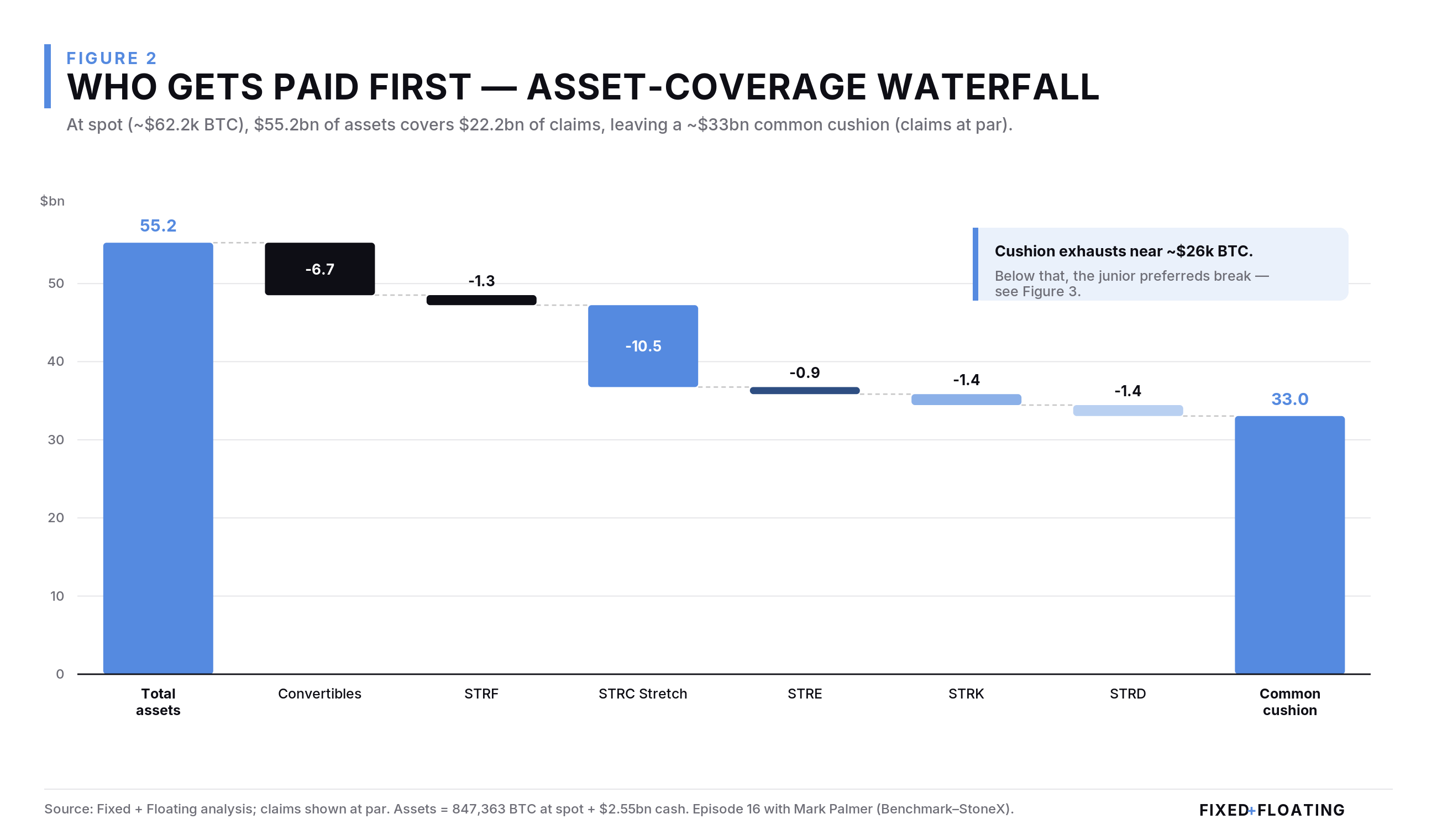

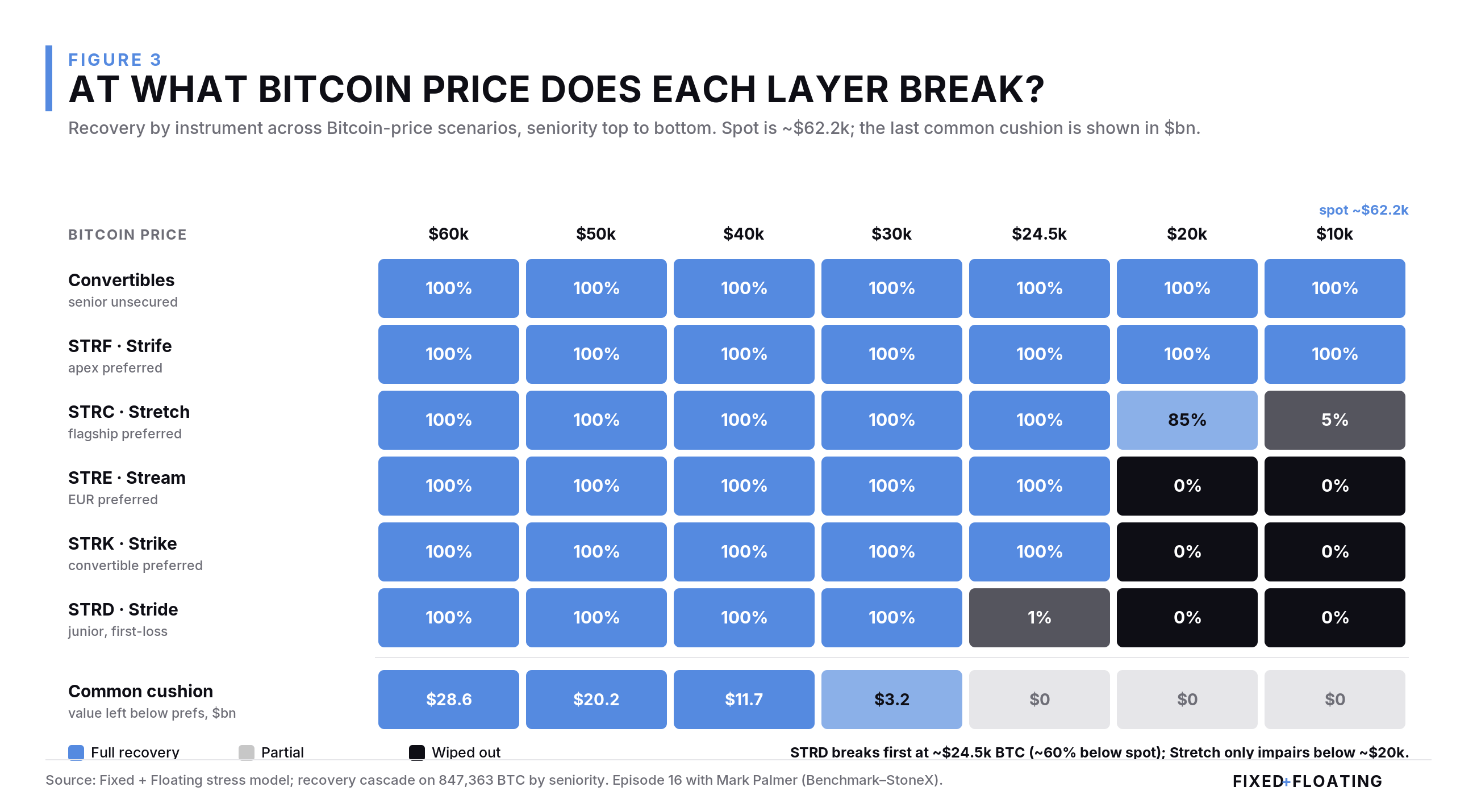

Ordering the stack this way does more than show quantum — it shows exactly where stress lands. Running the collateral through descending Bitcoin prices, the common equity absorbs first loss all the way down to roughly $26k Bitcoin. Below that, the junior preferreds cascade: STRD is wiped near $24.5k (about 60% below spot), STRK and STRE follow, and Stretch itself only begins to impair below ~$20k. The senior converts and STRF stay whole even at $10k. That is a far cry from a structure on the brink.

At spot (~$62.2k BTC), $55.2bn of assets covers $22.2bn of claims, leaving a ~$33bn common cushion (claims at par).

Recovery by instrument across Bitcoin-price scenarios, seniority top to bottom. Common absorbs first loss to ~$26k; the junior preferreds cascade below that.

What Actually Broke: Retail Leverage on a Non-Money-Market Preferred

PPopular narrative put the 32-Bitcoin sale at the centre of this episode. Palmer’s read is that the sale was about S&P’s issuer-rating model, not about liquidity. S&P’s B-minus write-up had effectively assumed Strategy would never sell Bitcoin under any circumstances — a literal reading of years of “never sell” evangelism — despite disclosures stating that Bitcoin could be sold under certain conditions to protect the structure. The 32-Bitcoin sale was deliberately de minimis, executed to prove the optionality exists. Within days the company resumed buying Bitcoin in far larger size and reiterated that its business remains accumulation. It was a message to a rating-agency model, not a pivot in strategy.

The real stress point sat elsewhere. Structurally, Stretch is a perpetual preferred with a ~12% face coupon after the recent 50bp hike, tax-advantaged distributions, and full exposure to market volatility. Yet a large share of holders had begun treating it as a cash-like instrument. Per the company’s own disclosure, roughly 80% of Stretch is held by retail investors — a holder base that almost never appears in that size in quasi-debt instruments, which tend to be institutionally dominated.

Many of those retail holders had layered margin leverage onto Stretch positions on the assumption they were parking cash in something close to a money-market fund. When Stretch slipped from par, those levered positions hit margin triggers, forcing price-insensitive selling into a falling market and compounding fear-driven redemptions from accounts that simply wanted out before it dropped further. Palmer’s assessment is that the bulk of the drawdown was driven by this forced deleveraging and panic selling, not by any deterioration in the instrument’s fundamentals.

A second misunderstanding sat on top. As Stretch’s price fell from 100 toward the high-80s, its effective yield (a ~12% face rate divided by a lower market price) mechanically rose. Some investors misread the higher yield screen as evidence that Strategy’s cash dividend obligations were climbing and the company was under growing strain. In reality, the cash outlay is set by the face rate and the outstanding notional; it does not re-set when Stretch trades at 88 or 68. What falls is the instrument’s usefulness as a funding tool: issuing preferred far below par is uneconomic and signals weakness. Put bluntly, the selloff was a leverage-and-behaviour event — retail margin on a volatile preferred while Bitcoin itself was falling — not a collapse in collateral coverage. That distinction is the whole game for anyone separating solvency risk from market-structure risk.

Why the 32-Bitcoin Sale Still Matters

If the sale did not cause the doom loop, why care about it? Because rating-agency assumptions feed the path of capital costs. S&P’s original B-minus had implicitly hard-coded Strategy as a buyer-only entity, ascribing no value to the disclosed optionality to sell Bitcoin tactically. By executing a de minimis sale and then immediately resuming large-scale purchases, management signalled two things at once: that it is willing to sell Bitcoin in stress to defend the structure, and that it will do so on its own terms and sizing rather than in a forced, liquidity-driven panic. From a credit lens, that proof point lowers the probability that an agency or lender models absolute rigidity and, from there, a forced-insolvency downside path. Optionality has value even when it is never used at scale.

That optionality is no longer theoretical. The 32-Bitcoin signal was quickly followed by the real thing: a sale of more than $250m, Strategy’s largest on record, to fund preferred distributions and top up the reserve. The escalation from signal to scale is the point: management has now demonstrated, not merely disclosed, that it will sell Bitcoin to defend the capital structure. For a rating model, a proven seller is a different credit from an assumed never-seller.

Perpetual Preferred as (Almost) Permanent Capital

Perpetual preferred sits deliberately between senior debt and common equity, and Strategy’s use of it is close to the cleanest expression of why that middle position exists for a volatile-asset balance sheet. Senior debt — bank loans, secured facilities, even convertible notes — carries covenants, collateral triggers and hard maturities. Strategy has already lived one version of that: a $205m Bitcoin-backed loan with a trigger that forced it to post additional Bitcoin when the price fell below a threshold. The loan was tiny against the overall stack, but it dominated the narrative, because markets fixate on the weakest link rather than the average strength of the structure.

Perpetual preferred avoids all three problems. It carries no maturity wall — some of these instruments could, in Saylor’s words, remain outstanding a century from now. It carries no covenants or Bitcoin-linked margin calls, sidestepping the “tiny loan, big headline” problem entirely. And it is non-dilutive to common while outstanding; dilution only appears if the preferreds are eventually equitized or taken out via share issuance.

Layer on the tax treatment and it edges closer still to permanent capital. As long as Strategy reports no positive net income — and management does not expect to for at least ten years — preferred distributions are treated as return of capital rather than ordinary income. For retail, high-net-worth and family-office holders, that is a meaningful after-tax uplift on top of a ~12% face rate. Capital-gains treatment still applies if an investor buys the preferred at a discount and sells higher, but the dividend income — the bulk of the total-return story — escapes ordinary income tax under current conditions. That combination is why Palmer describes Strategy and Strive (via SATA) as the two true pioneers of perpetual-preferred financing in the digital-asset-treasury space, and why treating Stretch as cash was always dangerous: you cannot simultaneously demand a 12% tax-advantaged yield, Bitcoin exposure, and money-market price stability.

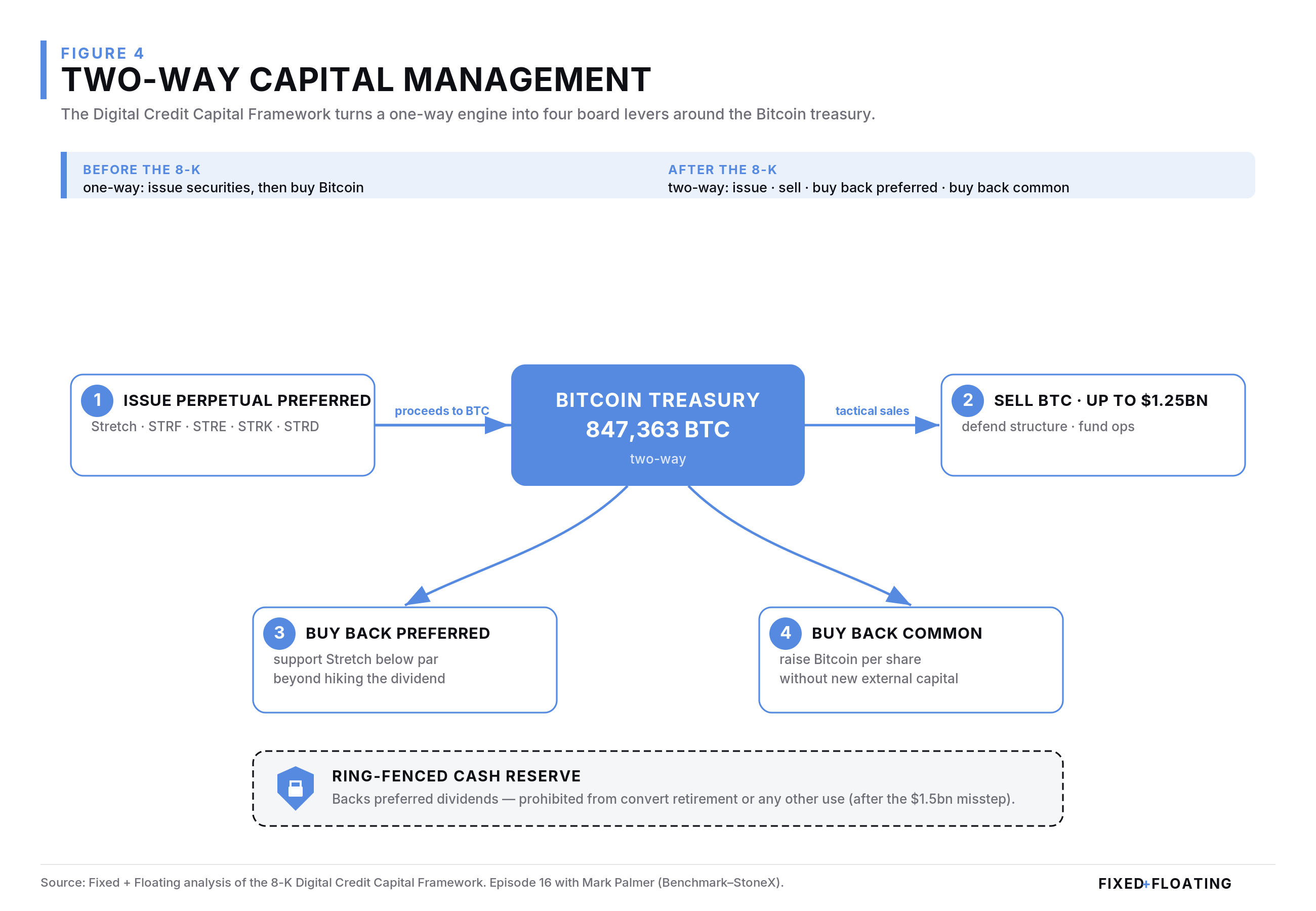

Two-Way Capital Management: Four Levers, One Ring-Fence

Before the latest 8-K, Strategy’s playbook was strictly one-way: issue securities, take the proceeds, buy Bitcoin. That regime works while markets pay a premium for new paper and Bitcoin is rising, but it leaves the company passive when demand dries up and its own securities trade at a discount. The Digital Credit Capital Framework formalizes a shift to two-way capital management, giving the board four explicit levers.

The Digital Credit Capital Framework turns a one-way engine into four board levers around the Bitcoin treasury.

First, it can issue perpetual preferred to buy Bitcoin — the core flywheel, run when pricing is attractive and demand is deep. Second, it can sell Bitcoin tactically, up to roughly $1.25bn, to defend the structure, fund buybacks or manage stress, ending the de facto “never sell” era without turning Strategy into a net seller. Third, and for the first time, it can buy back its own preferred, a direct lever to support Stretch when it trades below par beyond simply hiking the dividend. Fourth, it can buy back common — mechanically raising Bitcoin-per-share just as surely as buying more Bitcoin, but without depending on external capital.

Running across those levers is a new constraint: the cash reserve backing the perpetual preferreds is now ring-fenced. After management used $1.5bn of that reserve to retire converts — shrinking what retail holders had viewed as a multi-year dividend runway down to months — the framework now prohibits using the reserve for debt retirement or any other purpose. Retail holders, who own about 80% of Stretch, forced that correction in real time. This is the real governance upgrade: it codifies that the preferred reserve is not a silent piggy-bank for balance-sheet clean-up, and it leaves the convert wall to be addressed by other means. The framework did not stay on paper for long: within days of the 8-K, Strategy sold more than $250m of Bitcoin specifically to fund preferred distributions and refill this reserve — the two-way playbook used exactly as designed, and a signal that protecting the preferred dividend now sits ahead of dogmatic accumulation.

ATMs: Who Funds the Story, and How Big Is It?

Who stands on the other side of the at-the-market equity offerings that can raise over $1bn in a single week? Palmer’s answer is that the mix has evolved. It used to be a handful of anchor “true believers” plus a long tail of retail; today the ATM program is more institutionalised, run through a syndicate that resembles IPO book-building, with broker-dealers allocated blocks they place across client bases. Retail still dominates the total shareholder base and drives much of the day-to-day volatility, but institutions increasingly take up the offerings.

For credit investors, the critical point is that those ATMs only work while investors — retail and institutional — keep believing the story enough to double down at scale. The moment the narrative shifts from “proven Bitcoin-treasury compounder” to “over-engineered capital-structure trade,” the ability to sell $1bn in a week at attractive levels disappears. Stretch’s trading level and the common’s are therefore not just screen prices; they are continuous referenda on whether the market will keep funding the strategy. That is exactly why Palmer spends so much time on BTC yield: it is an attempt to prove that ATM capital is being converted into Bitcoin-per-share efficiently enough to justify the next round.

Different From 2022 — But Not Risk-Free

It is important not to blur this episode with the 2022 bust. In 2022 the equity traded below convert strike ranges, the converts collapsed into deeply distressed territory in the 30s–40s, and the market explicitly priced a non-trivial probability of coercive equitization and an equity wipe-out. A Bitcoin-backed bank loan with collateral triggers was still in the structure, and the risk conversation centred on senior instruments — covenants, margin calls and lender negotiations. That episode was about potential default on the debt.

This cycle is structurally different. The stack is anchored by perpetual preferreds and deeply in-the-money converts at a 0.52% blended coupon, and the fragility sat in retail margin accounts on Stretch rather than in bank covenants or standstill talks. The convert book still carries a 2027–2028 wall, but trades as short-dated credit, not near-default paper. The preferreds have become the true hinge: Stretch trades at a discount to par, but with large, liquid two-way flows and a ~12% coupon intact.

The existential caveats have not gone away. Everything here hinges on Bitcoin remaining relevant, non-corrupted and technologically robust — surviving quantum, protocol attacks, regulatory overreach, or a structural shift in digital-asset preferences. None of those risks is diversifiable inside Strategy’s model; they hit both the asset side and the narrative that justifies the capital-raising engine. Palmer’s long-term Bitcoin framework rests on fixed supply (21m coins by 2140), ongoing monetary debasement, and incremental institutional adoption via stablecoins, tokenisation and regulatory normalisation such as the CLARITY Act. If those drivers fail, no amount of capital-structure engineering ultimately saves the equity story.

What I Take Away From This — And What I Will Be Watching

The real credit risk is the capital-raising engine, not today’s balance sheet. With $55bn of assets over $22bn of par claims and a first-loss cushion that survives to ~$26k Bitcoin, solvency is not the near-term question. The near-term question is whether Strategy’s securities keep the premium needed to fund further treasury activity.

Perpetual preferred is powerful but fragile. Structurally, Stretch is close to optimal for a volatile-asset balance sheet: no maturities, no covenants, tax-advantaged, non-dilutive. But its “permanence” is a market-price fiction that holds only while it trades near par and can be issued at attractive levels. With ~80% retail ownership meeting margin leverage, that fiction broke in weeks.

The convert wall is a calendar problem, not a coupon problem. A $6.71bn stack at 0.52% blended is not an interest-burden story; it is a 2027–2032 refinancing-and-equitization story. How management meets it — Bitcoin sales, ATMs, preferreds, or a mix, now with the reserve ring-fenced off — defines the next chapter.

The single number worth watching is Stretch’s level relative to par. Bitcoin’s price matters, but the immediate tell for whether the flywheel can restart is whether Stretch normalises back toward 100 and stays there. A stable, liquid preferred market at par makes new perpetual issuance viable; a persistent deep discount turns Stretch from “permanent capital” into stranded capital.

The episode did not reveal a broken balance sheet. It revealed how sensitive Strategy’s model is to retail leverage, instrument misunderstanding, and the continuous vote of confidence expressed through the Stretch and common screens. For a credit investor, that is where the underwriting work now sits.

Listen to the full episode for Mark’s takes on Strategy.

This article is based on Episode 16 of Fixed + Floating, featuring Mark Palmer (StoneX). The views expressed are those of the speakers and do not constitute investment advice. For more information, please visit https://www.benchmarkcompany.com/leaders/1601/.

Fixed + Floating is a credit podcast for institutional investors and finance professionals — exploring the forces shaping global credit markets. Hosted by credit PM Josef Pschorn, the show features conversations with leading voices from investing, research, and academia.

Support Material: