The Invisible Tech Moat

E09 - James Bessen (BU/TPRI) explains why dominant firms get stronger as tech disruption accelerates

Walmart maintains 100,000 SKUs across its supply chain while Dollar General stocks 10,000 to 20,000. That gap doesn’t exist because Dollar General lacks ambition. It exists because once a firm crosses a certain size threshold — roughly a billion dollars in revenue — proprietary software and operational know-how become a form of competitive moat that smaller rivals cannot replicate, no matter how capable they are. This observation comes from James Bessen, an economist at Boston University’s Technology and Policy Research Initiative, a former software CEO, and author of two landmark books on how technology actually functions in markets: Learning by Doing and The New Goliaths. I spoke with him to understand how technology concentrates power, why disruption stories about dominant firms are often overstated, and what credit investors should actually be watching as artificial intelligence reshapes how firms compete.

The premise of much technology writing — that innovation is inherently democratizing, that smaller firms can out-maneuver giants with better products and lower costs — misses something essential about how competitive advantage actually works at scale. Bessen has spent two decades watching this play out across industries. His conclusion is counterintuitive and material for credit investors: technology is making it harder, not easier, for dominant firms to lose their position.

From Software to Economics: How a CEO Learned What Textbooks Got Wrong

When Bessen ran a software company in the 1980s and 1990s, he noticed something odd. Economics textbooks insisted that patents and proprietary technology were essential drivers of innovation. Yet the software industry — which had far fewer enforceable patents than, say, pharmaceuticals or manufacturing -- was innovating rapidly. Competitors were thriving. Knowledge was leaking everywhere. And the industry was not collapsing.

This observation became the foundation for Learning by Doing, published in 2015. Bessen’s core finding was simple but at odds with standard economic theory: the source of competitive advantage in knowledge-intensive industries is not legal protection. It’s accumulated know-how. The firm that learns fastest, and learns from doing, wins. The firm that can absorb lessons from each iteration, build organizational memory, and operationalize that learning into faster product cycles and better decision-making — that firm outpaces competitors. Patents matter far less than economists assumed.

The insight applies directly to how we should think about technology moats today. A moat built on learning — on the organizational ability to extract value from data, experience, and operational depth -- is far stickier than a moat built on a clever algorithm or a proprietary piece of code. This distinction matters enormously for credit investors trying to assess whether a tech company’s competitive position is durable or fragile.

The Walmart Model: Why Technology Alone Doesn’t Explain Market Dominance

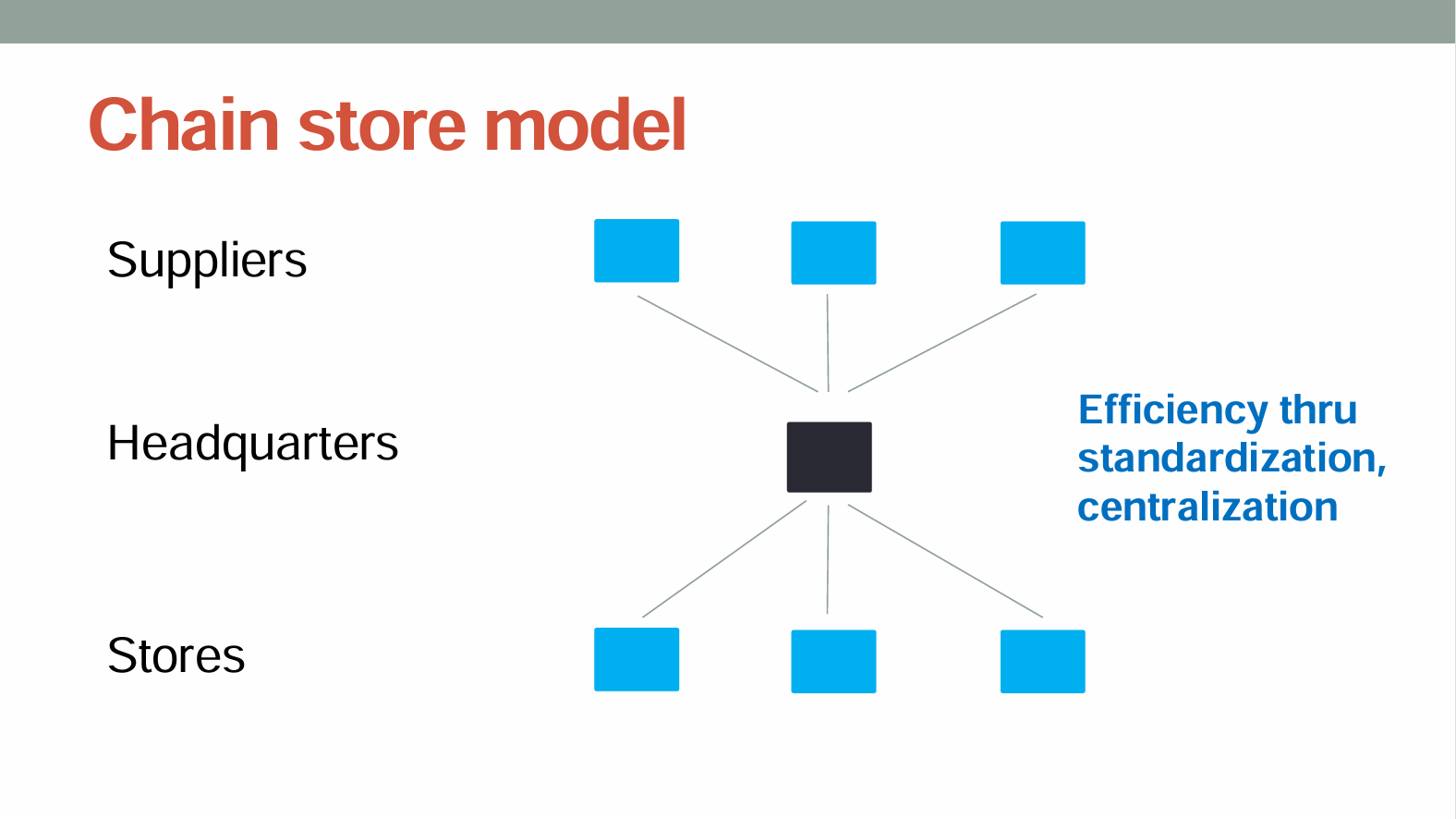

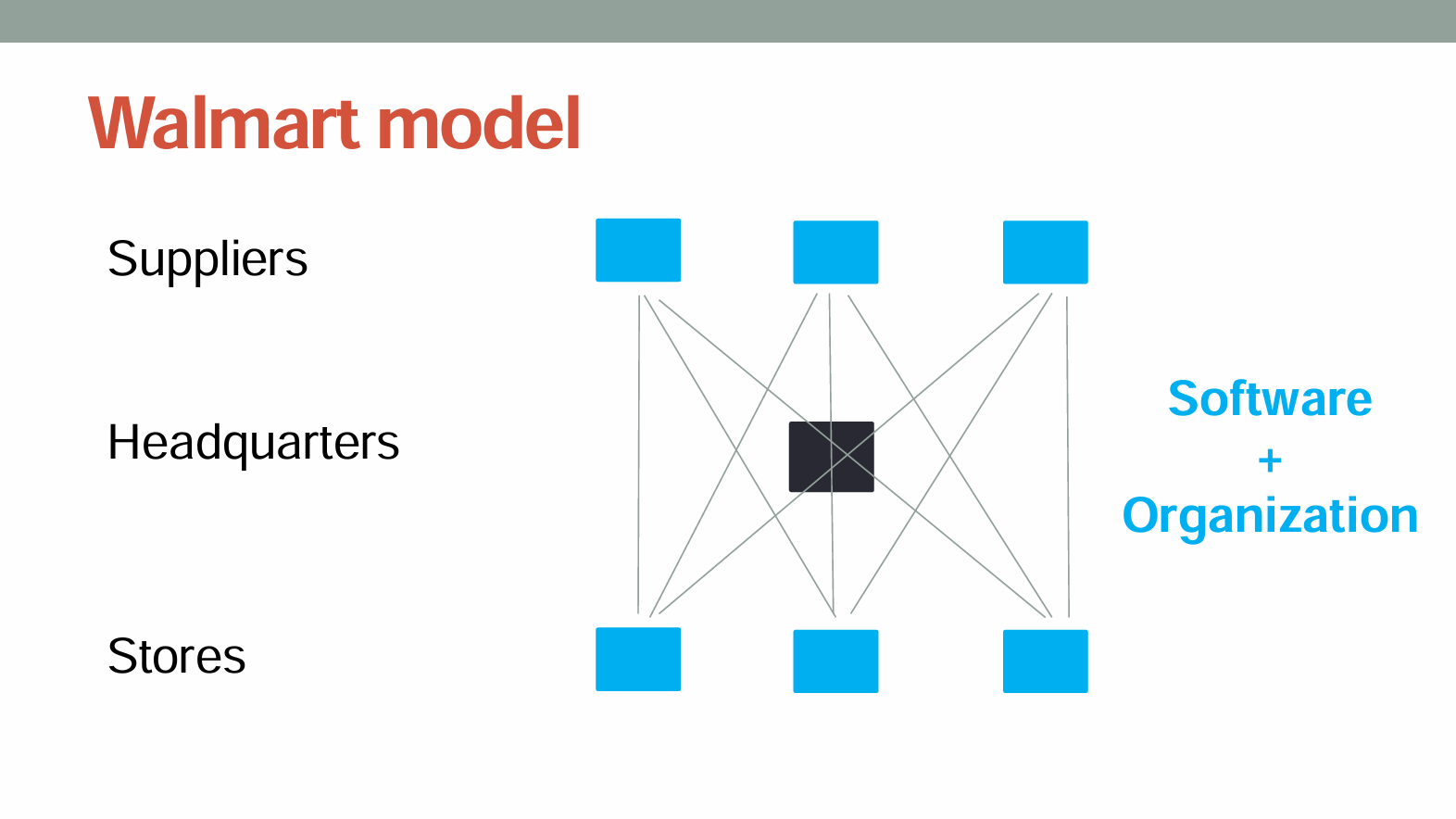

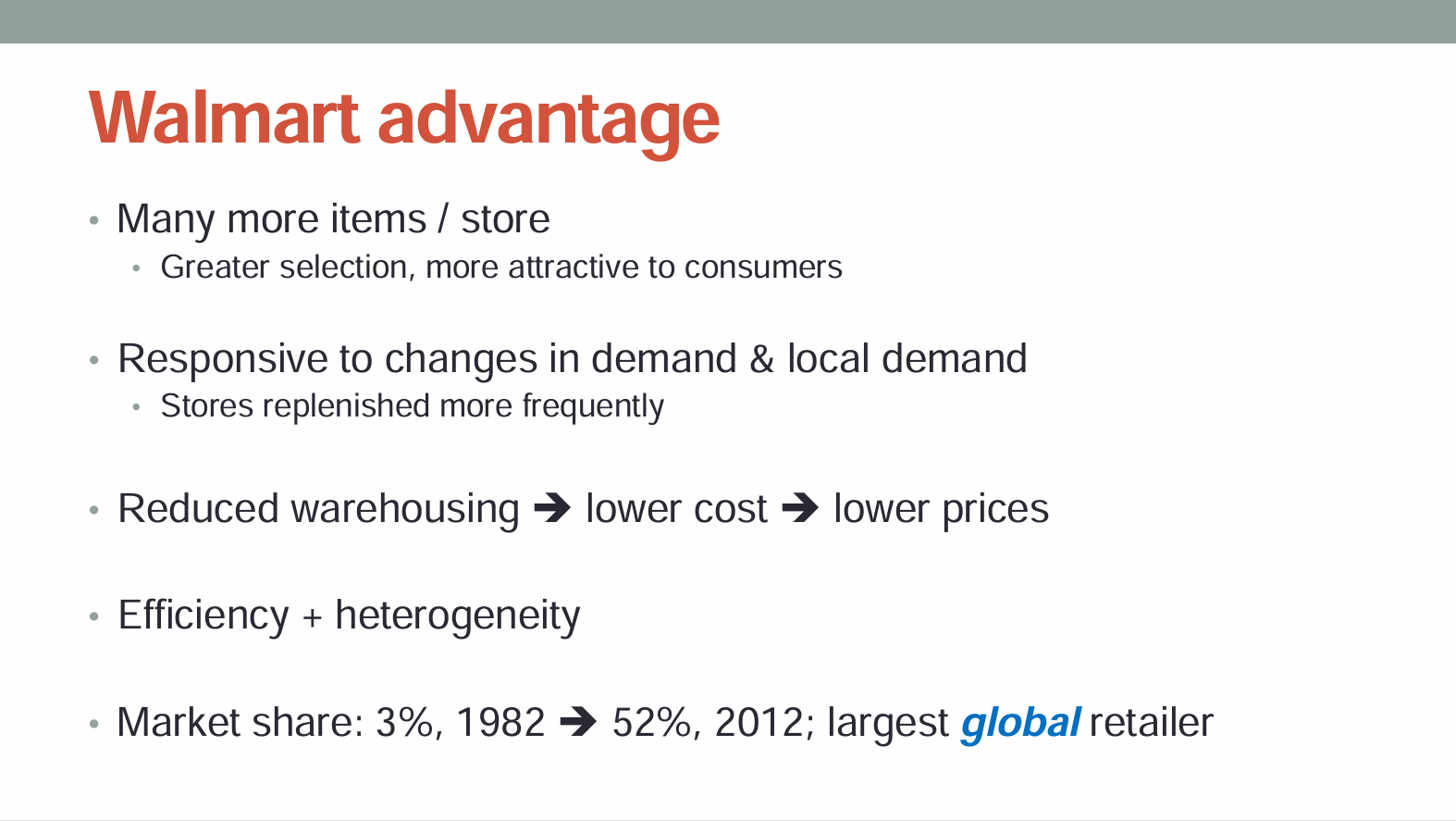

Bessen often uses Walmart to illustrate this principle. In the 1970s and 1980s, Walmart built a proprietary IT system that tracked every cash register, every store, every product, and every inventory movement across its entire supply chain. The system gave Walmart a decisive advantage: it could see demand patterns in real time and respond faster than competitors. If a product was selling well in one region, Walmart could replicate that signal across stores. If demand was dropping, it could adjust orders and floor space allocation faster than Kmart or other regional chains.

But the moat was not simply “Walmart had better software.” The moat was that Walmart’s entire organization had been built from the ground up to use that software effectively. Store managers understood how to interpret the data. Procurement teams had restructured supplier relationships around just-in-time ordering. The logistics network had been designed to support rapid inventory turns.

When Kmart attempted to replicate Walmart’s system in the 1990s, it failed. This wasn't because Kmart lacked the capital or the scale—at the time, Kmart was a retail giant. It failed because it lacked the organizational agility to deploy that software with the same effect. Kmart’s stores, suppliers, and management culture were entrenched in an older operating model. The software, in isolation, was useless without the institutional know-how to extract value from it. This shows why these moats are so durable: even well-funded peer competitors struggle to replicate decades of organizational learning.

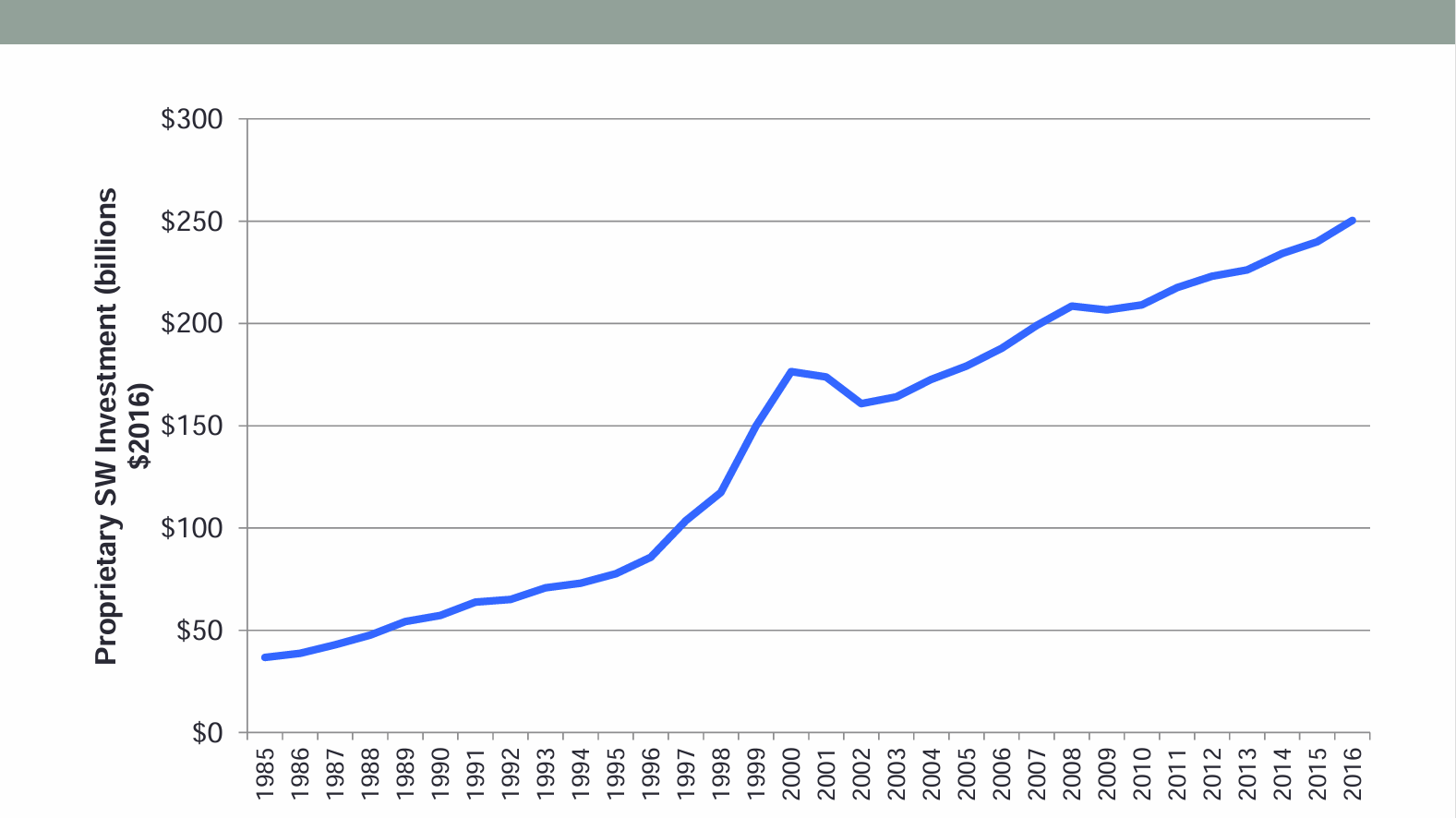

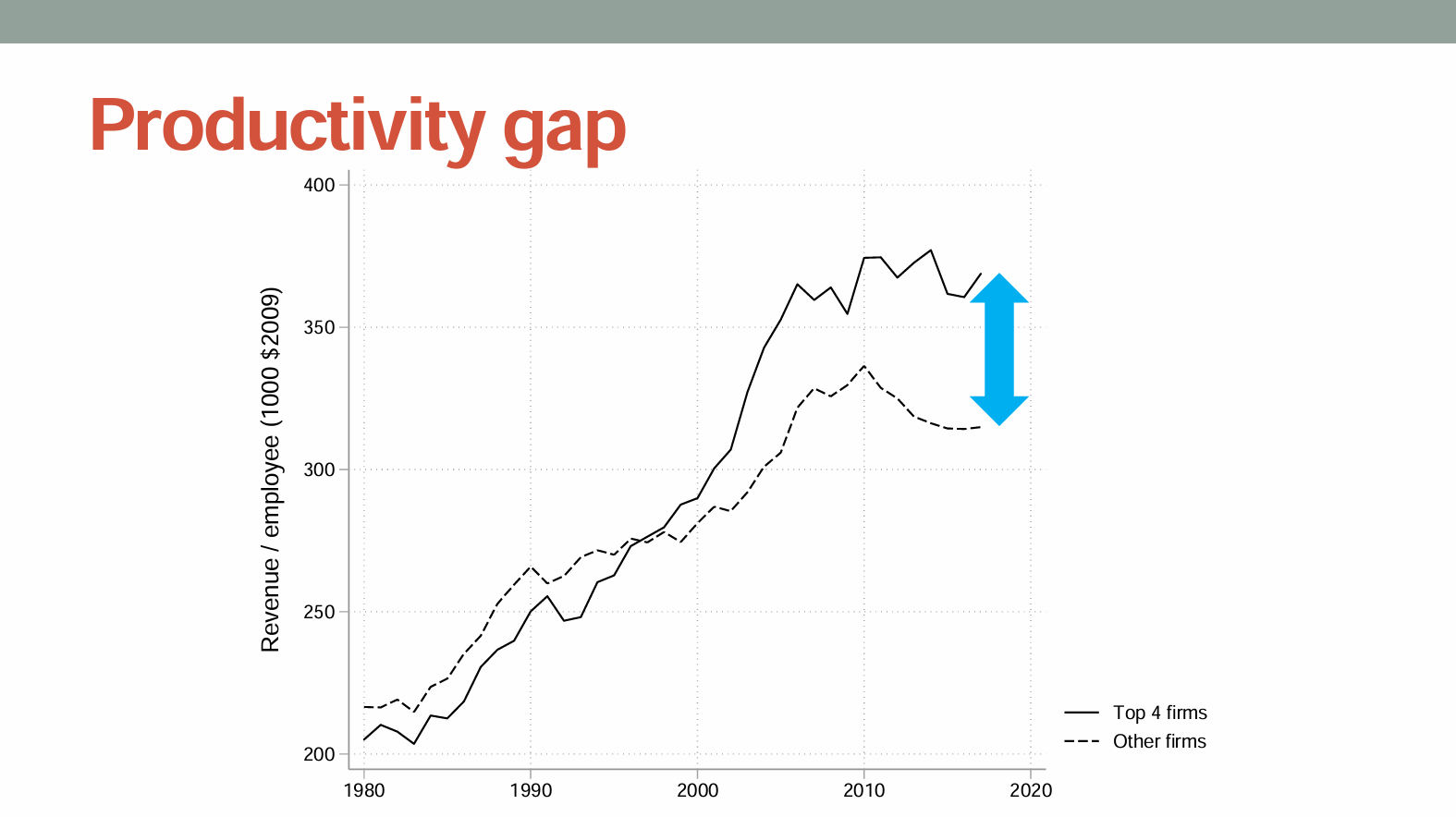

But while organizational complexity protects dominant firms from their giant peers, a different dynamic protects them from smaller upstarts: the brutal economics of proprietary IT. This is a crucial threshold Bessen identifies. A firm needs massive scale to amortize the fixed costs of building and maintaining a custom, proprietary software system.

Below a certain size, it is simply not economically rational for a smaller firm to build a system like Walmart's. Smaller rivals can buy off-the-shelf SaaS or build specialized niche tools. But they cannot match the scope, depth, or integrative power of a multi-billion-dollar proprietary platform. Software's high fixed costs and low marginal costs naturally favor the biggest player, allowing the Goliaths to continuously widen the productivity gap over everyone else.

Banks, Data, and the Fintech Challenge

The same dynamic appears in banking and finance. Large banks like JP Morgan have invested heavily in proprietary credit assessment systems. These systems don’t just automate what an older credit officer would have done manually. They ingest vast amounts of customer transaction data, behavioral data, and historical loan performance data. The bank’s data scientists continuously retrain the models. The models become more precise over time. And because JP Morgan has millions of customers, the data set compounds — each new loan, each default, each repayment adds signal to the next iteration.

Fintech firms have challenged traditional banks in certain segments — payment processing, for instance, or targeted lending to underserved customers. But in the U.S., fintech firms face a structural barrier that Bessen emphasizes: they do not have direct access to the customer transaction and deposit data that large incumbent banks possess. Open banking regulation in Europe has forced banks to share more data; in the U.S., incumbent banks have resisted these requirements. The result is that the largest U.S. banks retain a data advantage that smaller competitors, no matter how clever their algorithms, cannot easily overcome.

For credit investors, this matters. It suggests that disruption risk to incumbent banks — at least from fintech in the U.S. market — is lower than technology commentary often suggests. The moat here is real, and it is being reinforced, not eroded, by technology itself.

Assessing the Durability of Tech Moats: Value, Not Barriers

One common mistake in evaluating technology companies is to assume that a competitive moat must be built on barriers to entry — on something that prevents competitors from even trying. Bessen’s framework is different. The moat comes from delivering real, customer-facing value, and from the difficulty of replicating that value at the same scale.

Walmart’s moat is not that no one is allowed to build a supply chain system. The moat is that customers find what they want more often at Walmart than at competitors. That experience comes from decades of learning. It is not easily replicated. Competitors are not blocked by a legal wall; they face obstacles in building equivalent capability.

This distinction has a practical implication for credit investing. When evaluating a tech company’s competitive position, ask: Does this company deliver something customers value? And is that value difficult to replicate because of accumulated learning, scale economies, or organizational depth? Those are durable moats. The strongest tech moats are often invisible from the outside. They look like operational excellence, not innovation. They look like a company that executes well and learns continuously, not a company with a revolutionary product.

The Counterintuitive Truth: Disruption Risk Has Actually Declined

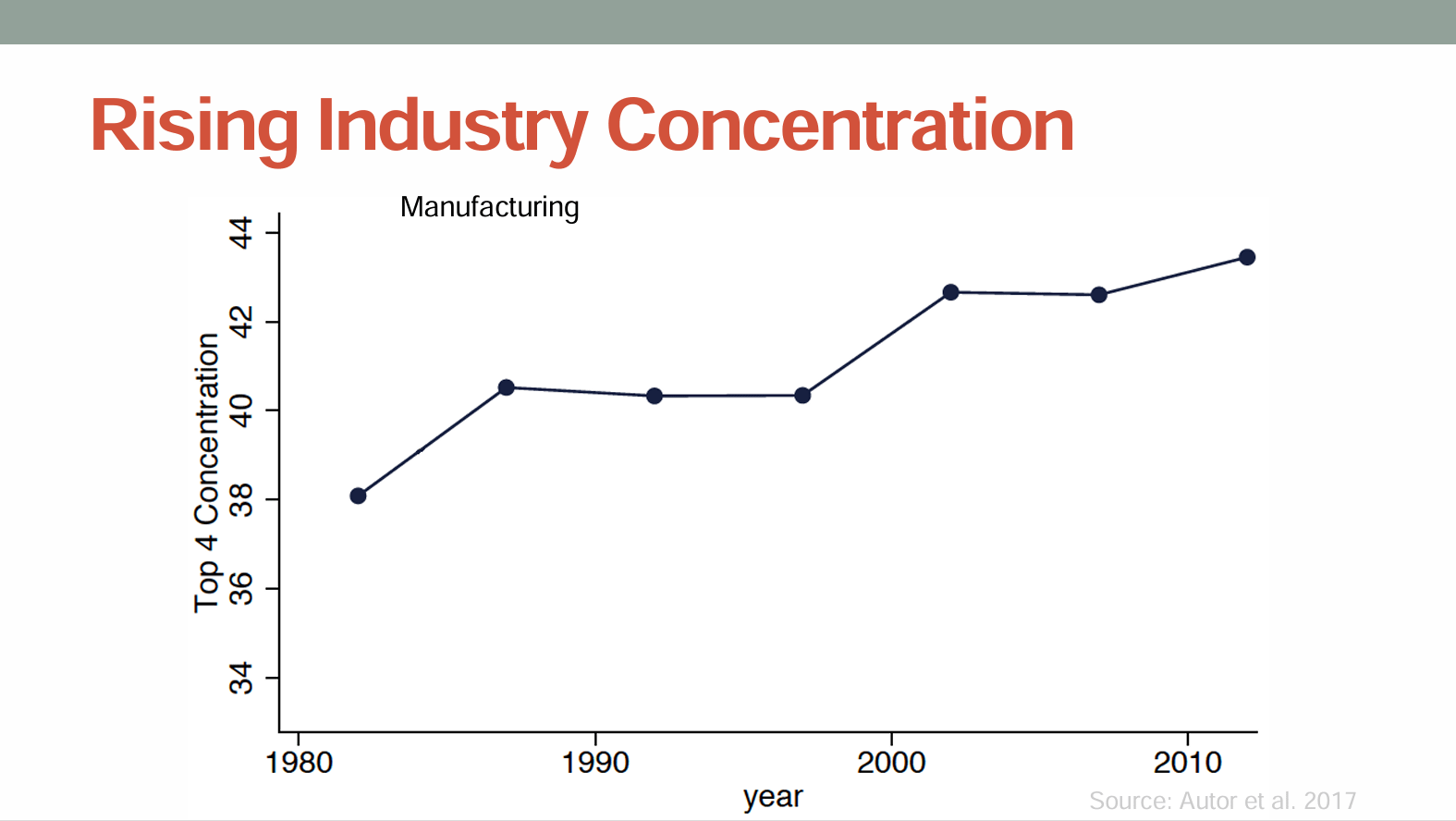

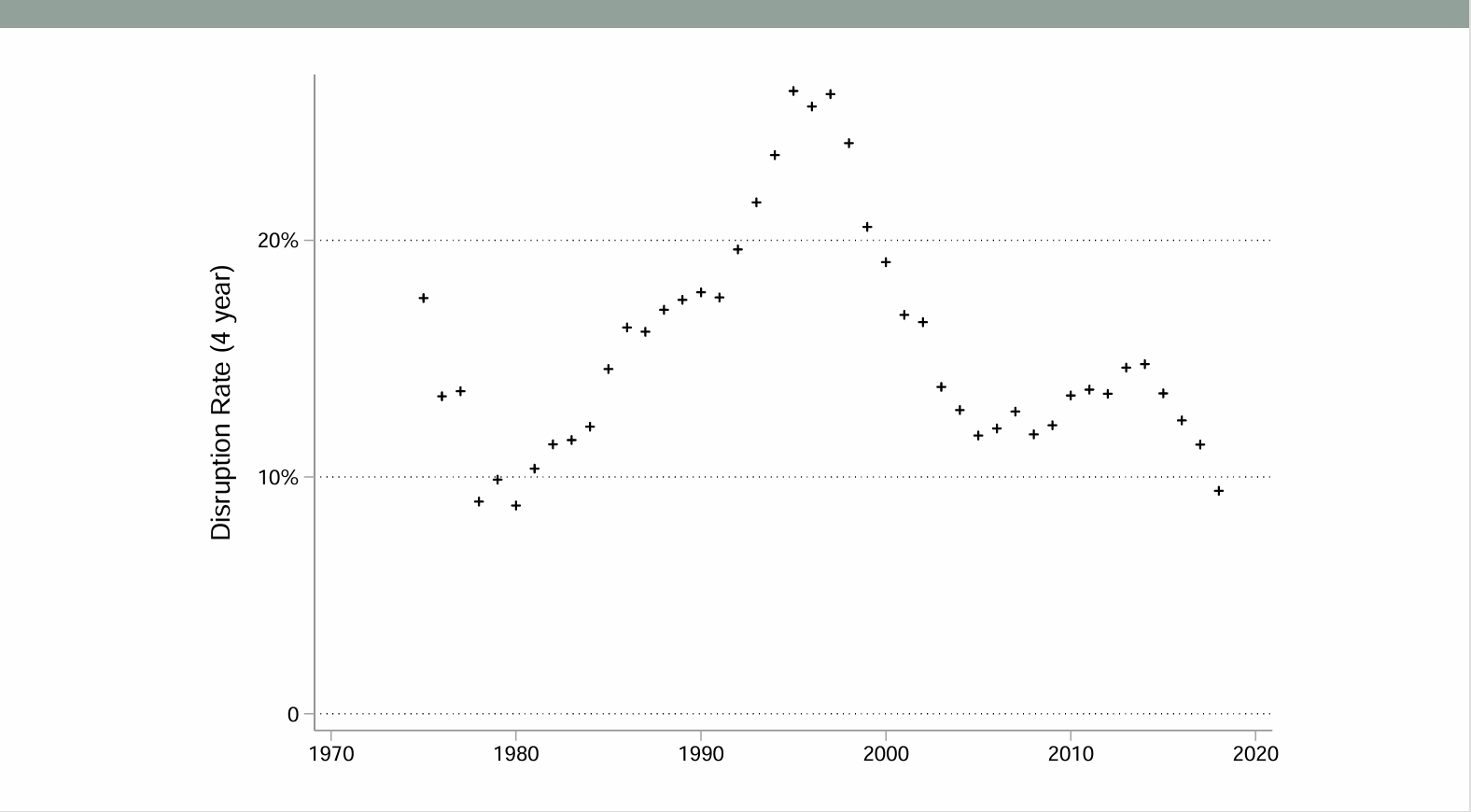

Here is where Bessen’s research departs sharply from conventional technology discourse. Over the past 20 years, the top four firms in most industries have become less likely to drop out of the top four than they were 20 years ago. This is true even as technology is changing rapidly and new entrants are appearing constantly.

The explanation lies in a paradox: technology increases competition in the aggregate. It lowers barriers to entry in many segments. It enables new business models. But at the very top of the market — among the largest, most established firms — technology is actually reinforcing incumbency.

Why? Because dominance at scale now rests on accumulated data, operational complexity, and organizational learning rather than on a single proprietary secret or a technological breakthrough. These advantages are compounding and harder to displace. A dominant platform that has learned how to integrate AI into its operations does not become more vulnerable to disruption because of AI — it becomes more powerful.

Consider IBM. In the popular narrative, IBM is a disruption cautionary tale. The company dominated mainframes in the 1960s, faced pressure from minicomputers in the 1970s, nearly collapsed when personal computers arrived in the 1980s. This story is correct in outline but misleading in implication. IBM did not disappear. It remained profitable and large for decades after its “disruption moment.” Revenue only began to decline around 2010, a full 25 years after the PC supposedly rendered the mainframe obsolete.

Nokia presents a similar case. The company dominated mobile phones. The smartphone was indeed disruptive. Nokia lost the phone business. But Nokia did not vanish. It shifted into telecommunications infrastructure and became, in Bessen’s blunt characterization, “more of a patent troll” — extracting rents from historical patents rather than competing on products.

The broader point is that disruption, when it happens, is slow. The dramatic stories in technology journalism — the moment the giant falls — are the tail end of a long process. For credit investors, this means that disruption risk to truly dominant firms is lower than headline attention suggests. The firm you think is vulnerable today may remain profitable and large for another decade, even as its market position erodes in real time.

Automation, Employment, and the Historical Pattern That Still Holds

One area where technology commentary becomes most overheated is employment. The fear that machines will displace human workers has been constant since the Industrial Revolution. Bessen’s historical analysis suggests we should be skeptical of that fear — not because disruption is impossible, but because the historical pattern has been remarkably consistent, and we have no convincing evidence that the pattern has broken.

In the 19th century, textile machinery dramatically increased output per worker. Looms became faster, spindles multiplied, automation accelerated. Economic theory suggested employment in textiles should have collapsed. Instead, employment in textiles grew for over a century. Why? Because demand was elastic. As cloth became cheaper, people bought more cloth. Families that previously owned two or three garments could now afford six or seven. Industrial demand for textiles expanded. So even as output per worker rose, the industry needed more workers overall.

The employment decline in textiles did not come until the mid-20th century, when demand finally saturated. Closets were full. The savings from automation no longer translated into increased demand; they translated into lower prices and reduced headcount.

The same pattern is visible in software development today. Programmer productivity has increased roughly 5% per year for the past 20 years, compounded. According to standard economic theory, employment in software development should have fallen. Instead, employment has risen by roughly 3% per year, and the total number of software developers employed is at an all-time high. Demand has grown faster than productivity gains.

Microsoft’s internal study of Copilot found a 26% productivity gain for developers using the tool. The study found no employment effect. The developers worked faster. Projects completed ahead of schedule. And the company assigned those developers to new projects, creating new software rather than eliminating the headcount.

For credit investors, this distinction matters. Companies that are planning workforce reductions tied to AI adoption may be facing a different dynamic than they expect. Demand may simply shift. Productivity gains may be captured through new products and services, not through headcount reduction.

AI Investment and the Winner-Take-All Risk: Why This Bubble Is Different

Bessen’s analysis of AI investment risk departs from cheerful startup narratives but also from doomsday scenarios. The comparison he draws is to the dot-com bubble, and the distinction is clarifying.

During the dot-com boom of the late 1990s, massive capital flowed into fiber optic cable and server infrastructure. When the bubble burst and many companies failed, the recession was mild because the infrastructure did not disappear. Fiber optic cables remained in the ground and eventually came back into service as data demand grew. They lasted 20-30 years. Servers lasted about 10 years. The capital was wasted, in a sense, but it was not destroyed — it was eventually put to productive use.

AI investment is fundamentally different. The majority of current AI capex is not going into durable physical infrastructure. It is going into training frontier models and purchasing GPUs to run them. A frontier AI model becomes outdated on an average timeline of two months. A GPU under continuous training stress lasts a couple of years before degradation makes it inefficient. If there is a recession or a correction in AI valuations, these assets will not come back into service. They will be worthless.

This creates a winner-take-all dynamic that is far more brutal than the dot-com scenario. Dario Amodei, CEO of Anthropic, captured the risk: “It’s not going to support all of them.” If only a small number of AI companies end up viable and profitable, the capital invested in the runners-up will simply evaporate. There will be no recovery when demand returns, because the assets are consumed, not mothballed.

For credit investors, this matters in two ways. First, AI companies that are burning capital in pursuit of frontier model development should be viewed with skepticism about profitability timelines. Second, the broader AI capex boom contains embedded tail risk. Not all of this capital will generate returns. The question is how much will be trapped in failed companies and stranded assets.

Who Actually Profits from AI: Adaptation, Not Disruption

The winners in the AI era will not be the companies building the largest language models or the most sophisticated chat agents. Instead, the winners will be companies that figure out how to adapt AI to real problems in their existing business.

Consider call centers. Many companies have implemented AI chatbots to reduce labor costs. By most accounts, customer experience has degraded. Call quality has fallen. Customers are more frustrated. Yet the capital investment has been made, and sunk costs are driving continued deployment.

Contrast this with organizations that use AI as a tool to augment human workers. A customer service representative using an AI system that suggests relevant policies and account history can handle more complex inquiries. In these cases, AI increases human productivity and value creation. The profit opportunity is real.

Industry concentration has been rising for the past 100 years as economies have matured. This trend existed long before AI. But AI, deployed thoughtfully, can accelerate it. If only the largest firms have the scale to deploy AI in a value-creating way, concentration will continue to rise. Smaller firms will deploy AI in cost-cutting ways and will gradually lose margin. Credit quality will follow.

Antitrust, Unbundling, and the Paradox of Forced Competition

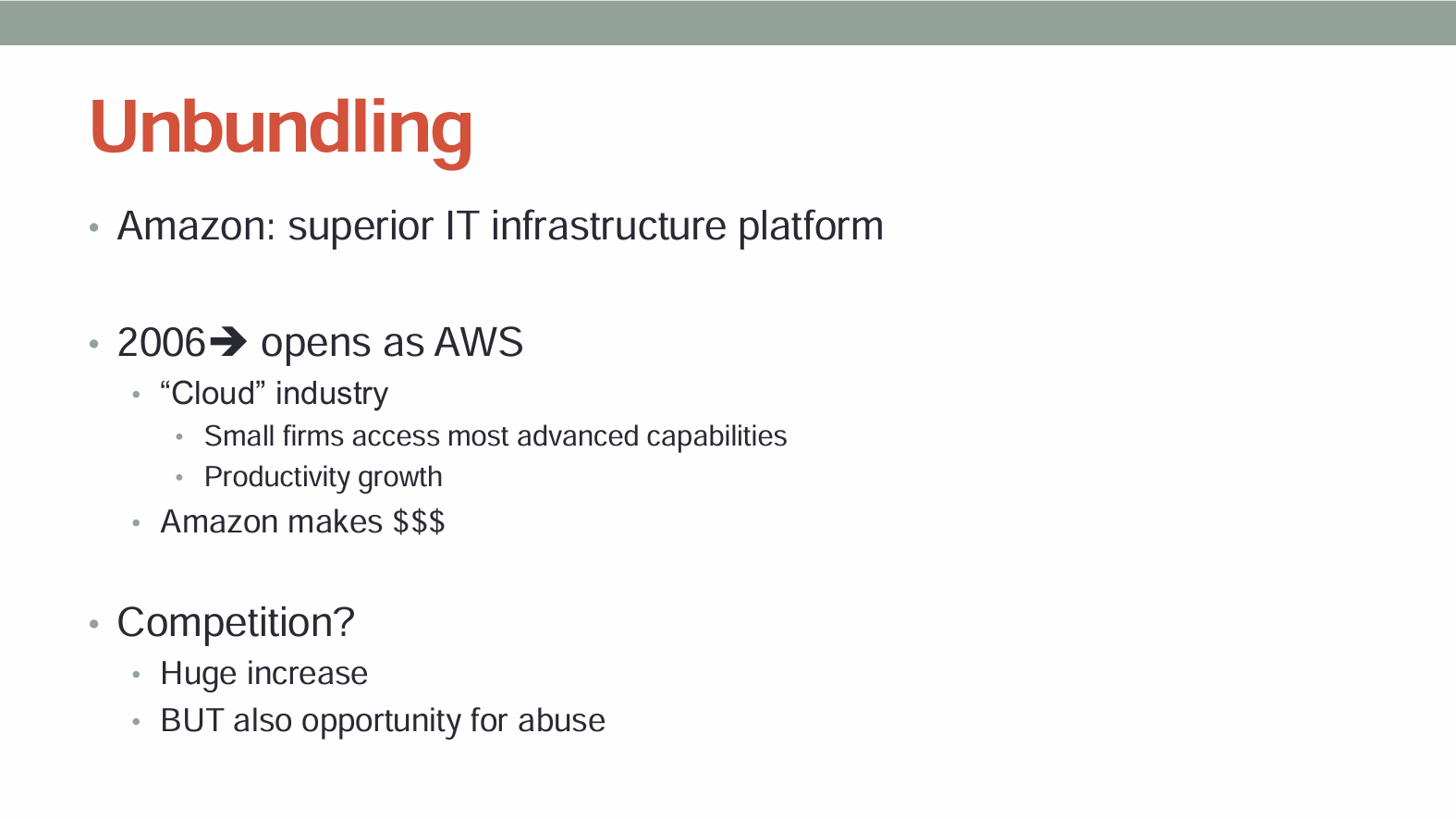

Bessen tells a story about IBM and the U.S. Department of Justice that upends typical antitrust logic. In the 1960s, IBM bundled software with hardware. The DOJ threatened antitrust action. IBM unbundled — it began selling software separately from hardware.

The result surprised everyone. Once the software market was open, third-party developers flooded in. Software development accelerated. New applications emerged. IBM’s software business grew enormously. The unbundling was far more profitable for IBM than the bundled approach had been.

Amazon’s AWS tells a related story. Amazon developed its own internal web services infrastructure to support its e-commerce business. Then it opened this infrastructure to external customers for a fee. AWS became one of the most profitable divisions of Amazon. Again, the demand was hidden until the market was opened.

The implication for antitrust policy is subtle. Regulation intended to increase competition in the product market may, paradoxically, increase technological competition while actually benefiting the dominant firm. Forcing dominant firms to open their systems can benefit the dominant firm more than it benefits rivals, while also creating genuine spillover benefits to the broader economy.

For credit investors, the lesson is that forced unbundling or forced data sharing — potential outcomes of antitrust litigation against large tech firms — may not harm the dominant firm as much as regulation proponents hope. In fact, if recent history is any guide, the dominant firm may eventually profit from the change.

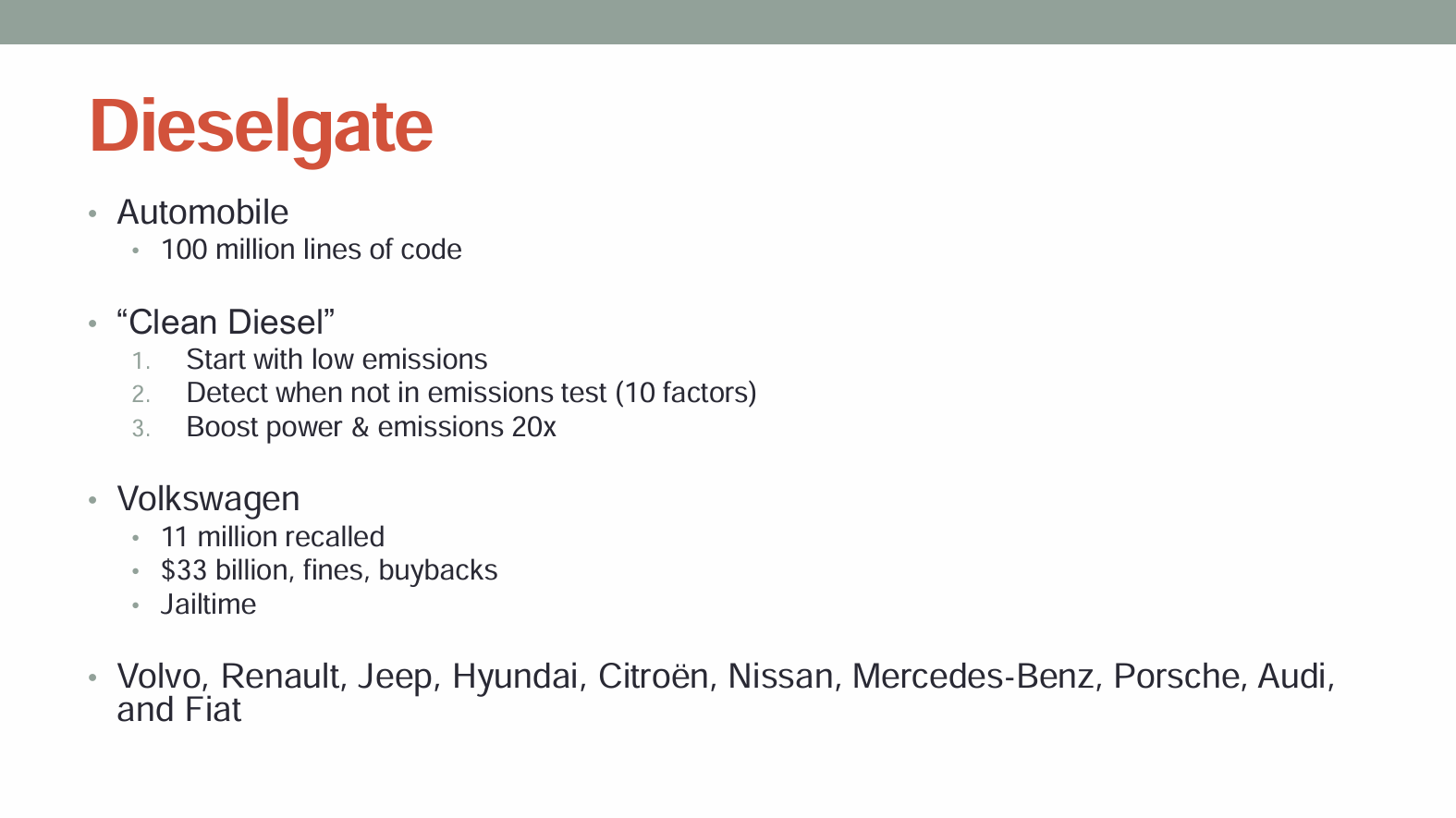

Software Complexity and Regulatory Risk: The Dieselgate Precedent

Dieselgate — Volkswagen’s emissions test cheating software — illustrates how software complexity makes regulation fundamentally harder. A small number of VW programmers wrote code that detected when a car was undergoing an EPA emissions test and reduced emissions during the test, while allowing much higher emissions during normal driving. The software was relatively simple to create. It was extraordinarily difficult to detect. Volkswagen’s cars were emitting pollutants at 10 to 20 times the legal level.

The same dynamic appeared in the 2008 financial crisis. Mortgage instruments became so complex, and their risk characteristics so obscured through layers of software abstraction, that even professional investors could not accurately assess them.

As economies become more software-dependent, regulatory enforcement becomes exponentially harder. This favors incumbent firms with large compliance teams, deep regulatory experience, and the resources to invest in legal infrastructure. For credit investors evaluating firms in highly regulated industries — automotive, banking, pharmaceuticals — the software complexity layer is material.

Evaluating Technology Investment: When Capex Becomes Unpredictable

A traditional capex investment in a steel mill has clear parameters. You invest in the mill, it produces steel at a certain rate, the market for steel determines your profit.

Technology investment is far harder to evaluate. company have profit-making potential? Will its investments deliver capabilities that customers value and will pay for? The answer is almost always opaque. Many AI companies are currently unprofitable. The path to profitability relies on costs coming down — a speculative assumption about a specific path of technological development that may not materialize.

For credit investors, this means traditional capex analysis tools are inadequate when applied to technology companies. The risks are different. The timelines are different. The probability of total capital loss is much higher.

Listen to the full episode for James Bessen’s take on how technology strengthens incumbents, why disruption stories are often overstated, and what credit investors should actually be watching as industries become more software-intensive.

This article is based on Episode 9 of Fixed + Floating, featuring James Bessen of Boston University’s Technology and Policy Research Initiative. The views expressed are those of the speakers and do not constitute investment advice. For more information, please visit https://sites.bu.edu/tpri/.

Fixed + Floating is a credit podcast for institutional investors and finance professionals — exploring the forces shaping global credit markets. Hosted by credit PM Josef Pschorn, the show features conversations with leading voices from investing, research, and academia.

Support Material: