When Annuities Meet Private Credit: The Regulatory Arbitrage Nobody Is Talking About

E10 — Jakub Lichwa (TwentyFour AM) decodes the capital structures and rating games reshaping life insurance's private credit pivot

Private credit now accounts for roughly one-third of the $6 trillion US life insurance asset base. The median age of the US population has shifted from 30 in the 1980s to 39 today, and that single demographic fact has rewritten the business model of American life insurance. As an aging population demands yield, traditional life insurance companies—increasingly owned by private equity—have become the marginal buyers of a broad spectrum of private credit, particularly highly rated, investment-grade assets spanning real estate, infrastructure, and asset-backed securities.

This is not inherently sinister. Insurance balance sheets are a natural home for illiquid assets. But beneath this demographic shift lies a more complex engine: regulatory arbitrage. The true story of the private credit and life insurance boom is how capital efficiency is being optimized to the absolute limit. The way these assets are structured, financed, rated, and aggressively arbitraged across state lines and into offshore captive reinsurers creates a systemic mechanical tension—one that warrants close examination by any credit professional.

(Note: For a foundational primer on the mechanics driving this shift, check out our previous deep dive with Jakub Lichwa on Episode 3)

Private Credit's Insurance Flywheel Exposed

Global life insurers have become the quiet keystone of private credit: they manage $25–30 trillion (around 8% of global financial assets), hold roughly 20–25% of the $1.5–1.8 trillion direct lending market, and yet their exposure looks manageable in aggregate while risk is building in opacity, concentrations, and capital engineering at the margins.

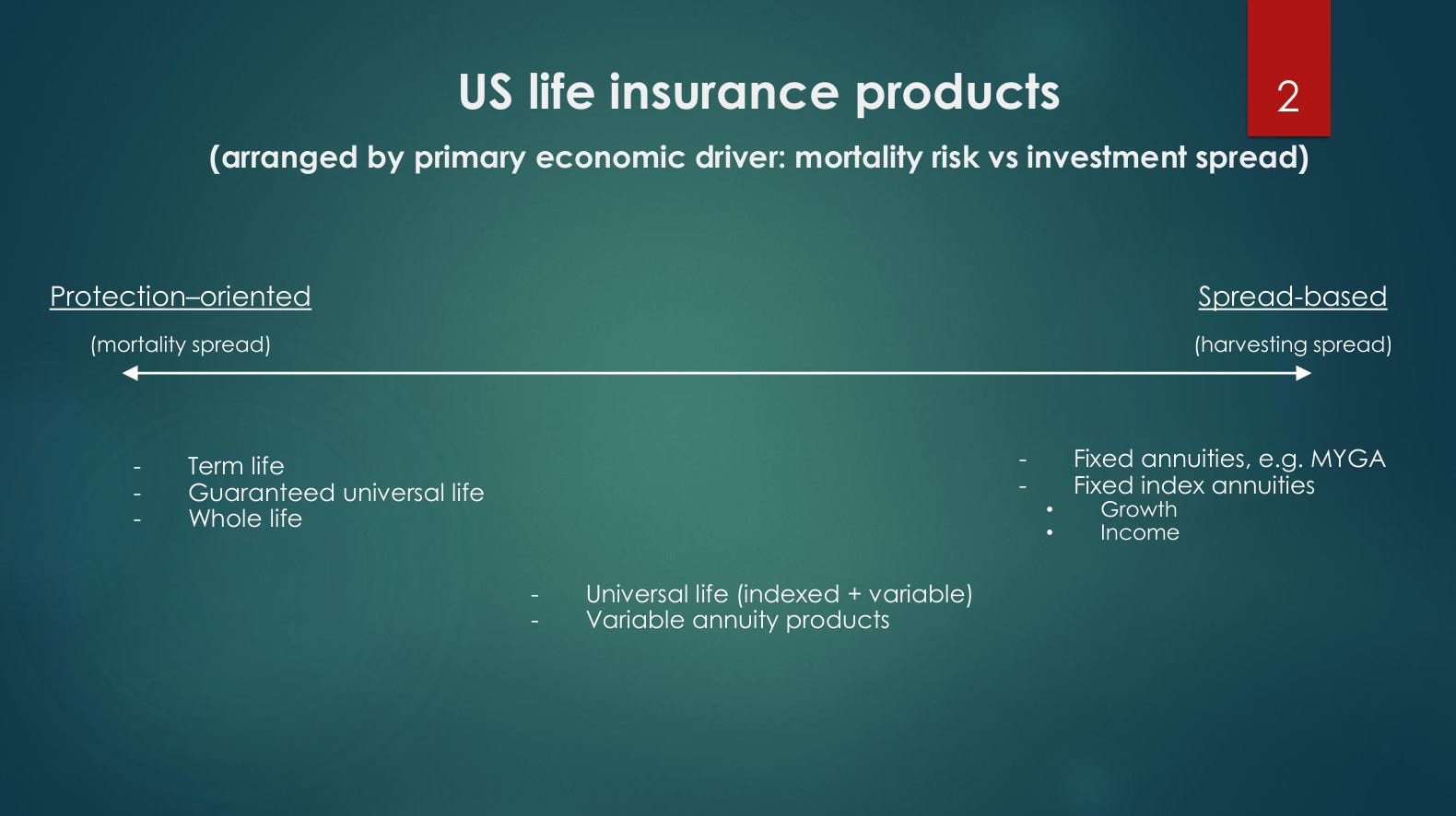

Understanding US Life Insurance Products

To understand why private credit has become central to insurance asset allocation, one must first understand the structure of the liabilities being funded. Most US life insurance products can be classified into two broad categories (variable annuities fall somewhere in between):

Protection-oriented products: Term life, whole life, and guaranteed universal life (GUL) earn revenue primarily from mortality spread—the difference between premiums charged and claims paid. The insurer bets that claims will be lower than expected. These products have no stated maturity, and claims can accelerate in unpredictable fashion (e.g. pandemic, natural disaster), and as a result the business has natural need for more liquid assets that can be sold quickly.

Spread-based products: Fixed annuities, Multi-Year Guaranteed Annuities (MYGAs), and fixed index annuities (FIAs) earn profit from the investment spread—the difference between yield earned on invested assets and the crediting rate paid to the annuitant. An insurer might invest at 5.5% and credit at 4.0%, keeping 150 basis points. These products are acutely interest-rate and duration-sensitive. They also have clear maturity profiles which can be aligned with those of private credit assets.

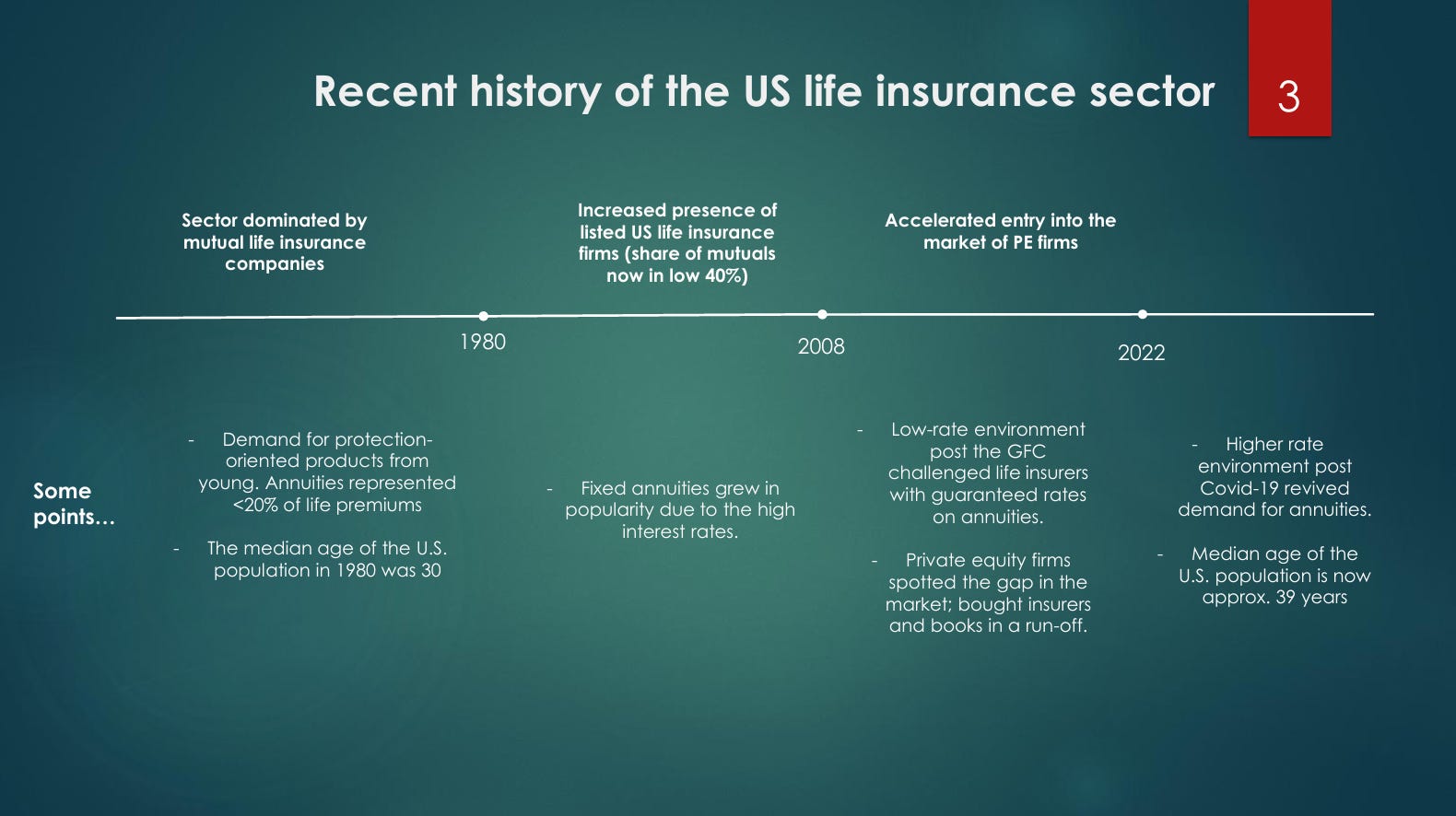

The mix of these categories, and the rate environment in which they are sold, determines the insurer’s duration profile, asset allocation, and leverage. Pre-1980s, the US population was young (median age 30) and demand was for protection products. The 1980s brought rising rates, and annuities exploded as consumers wanted to lock in yields. Then 2008 and the GFC crushed annuity-heavy books through spread compression between 2010 and 2015.

This created conditions for private equity buyouts of insurance firms. Sponsors brought capital, operational expertise, and critically, access to origination channels in private credit markets. Post-2022, rising rates and an aging population have triggered an annuity renaissance.

The Asset-Liability Match: Why This Model Works

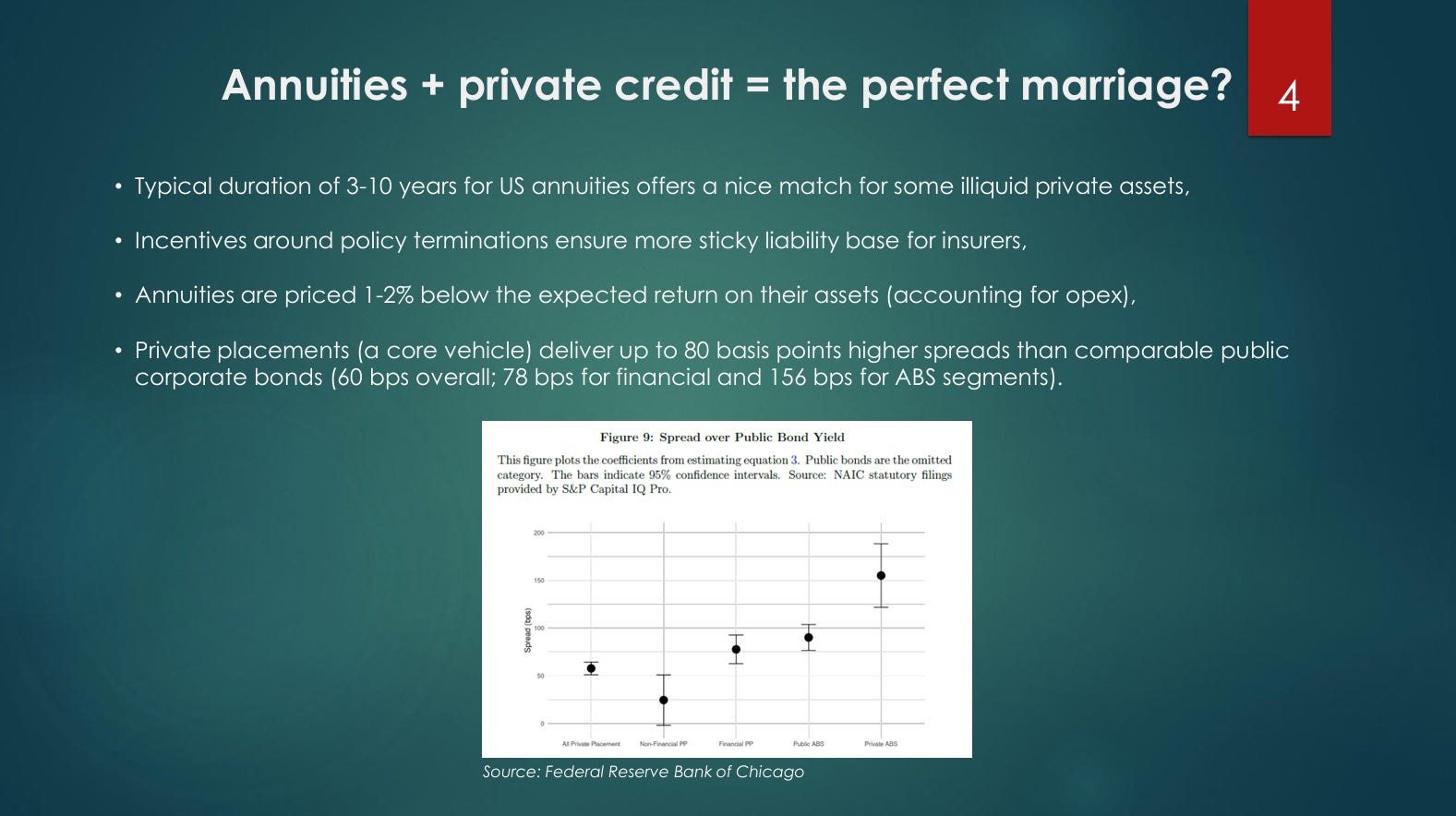

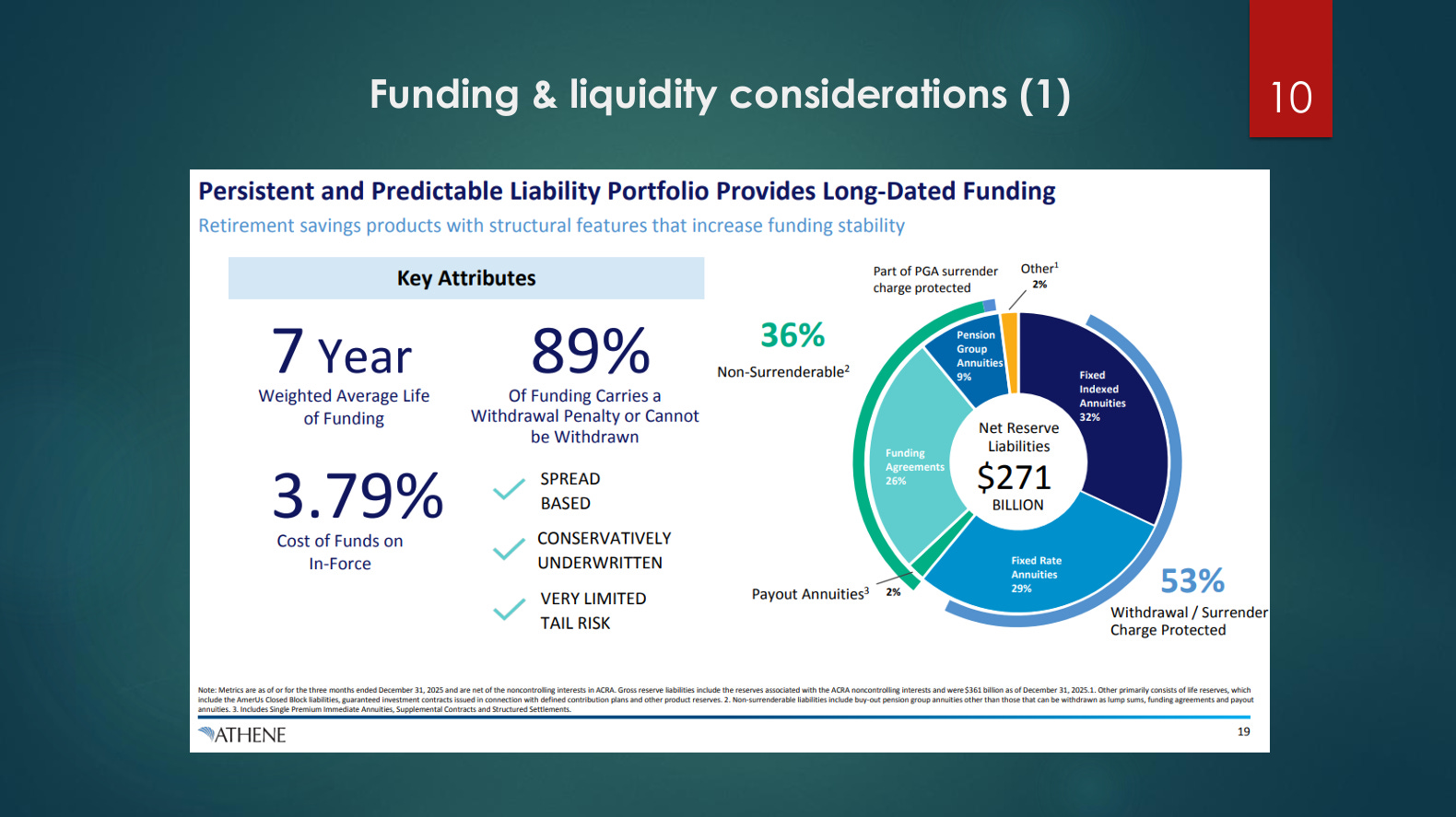

The match between annuity liabilities and private credit assets is structural, not accidental. Annuity liabilities carry durations of 3 to 10 years. Private credit placements across various underlyings—such as real estate lending, infrastructure financing, and asset-based finance—can be structured to match precisely.

Liability stickiness and predictability amplify the value. Annuity policyholders face surrender charges of 6% to 8% in year one, stepping down to zero after 10 years. An insurer placing capital into a 7-year loan knows the annuity funding it will remain in place for at least 5 to 7 years.

Pricing mechanics create a pull toward higher-yielding assets. Annuities are typically priced 1% to 2% below asset yield. Private placements deliver roughly 80 basis points of pickup versus public corporates (approximately 60bps from the general liquidity premium, 78bps from financial placements, and 156bps from ABS segments). Without this pickup, the spread narrows to levels insufficient to cover administrative costs and desired profitability, whilst retaining competitive pricing of annuities.

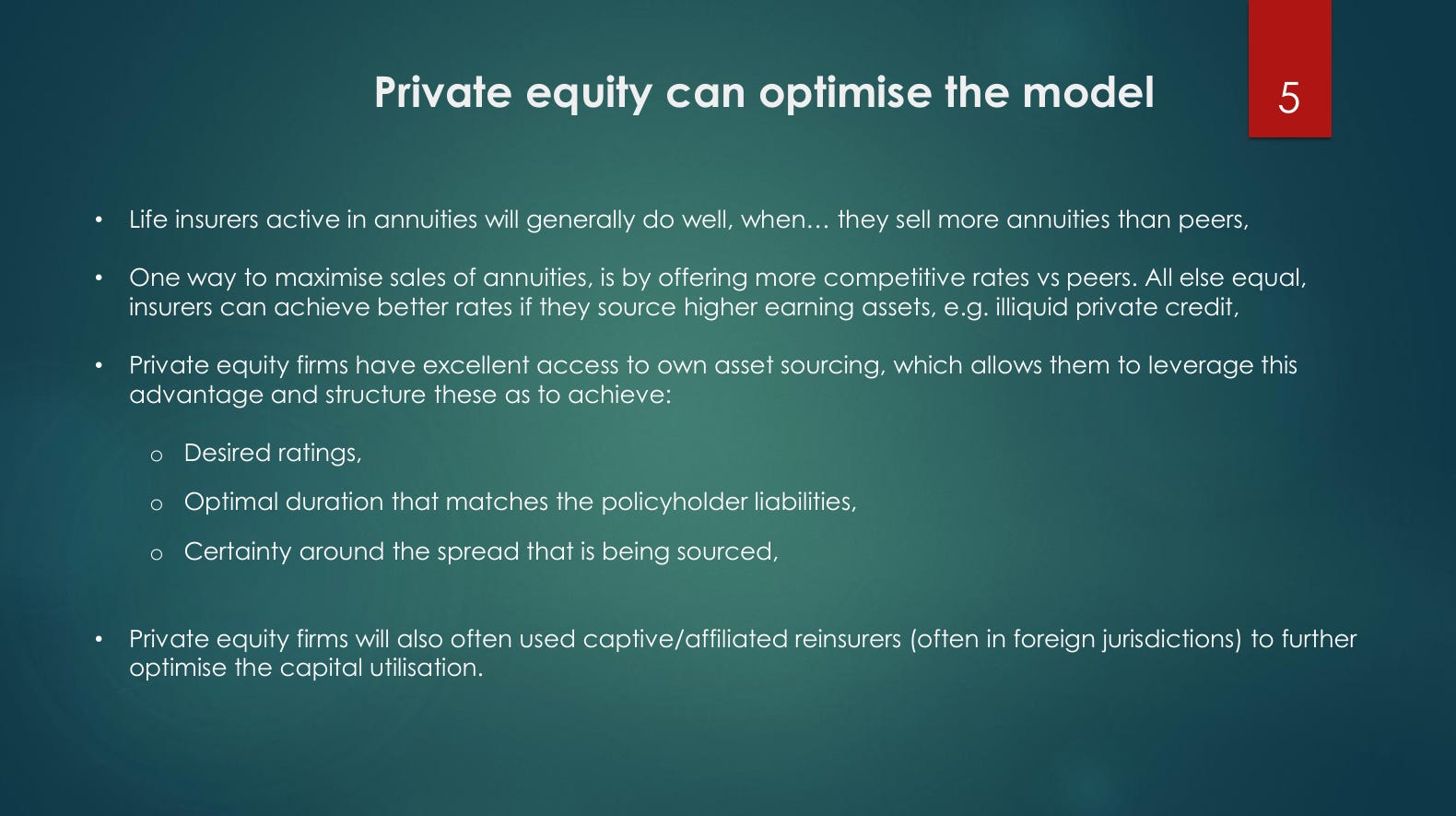

PE-backed insurers solve this through their virtuous flywheel: the sponsor controls origination, structures assets for desired ratings and duration, deploys them into the insurer, then uses captive reinsurance to release capital for the next round. Banks retreating post-GFC left a lending gap that this model efficiently fills.

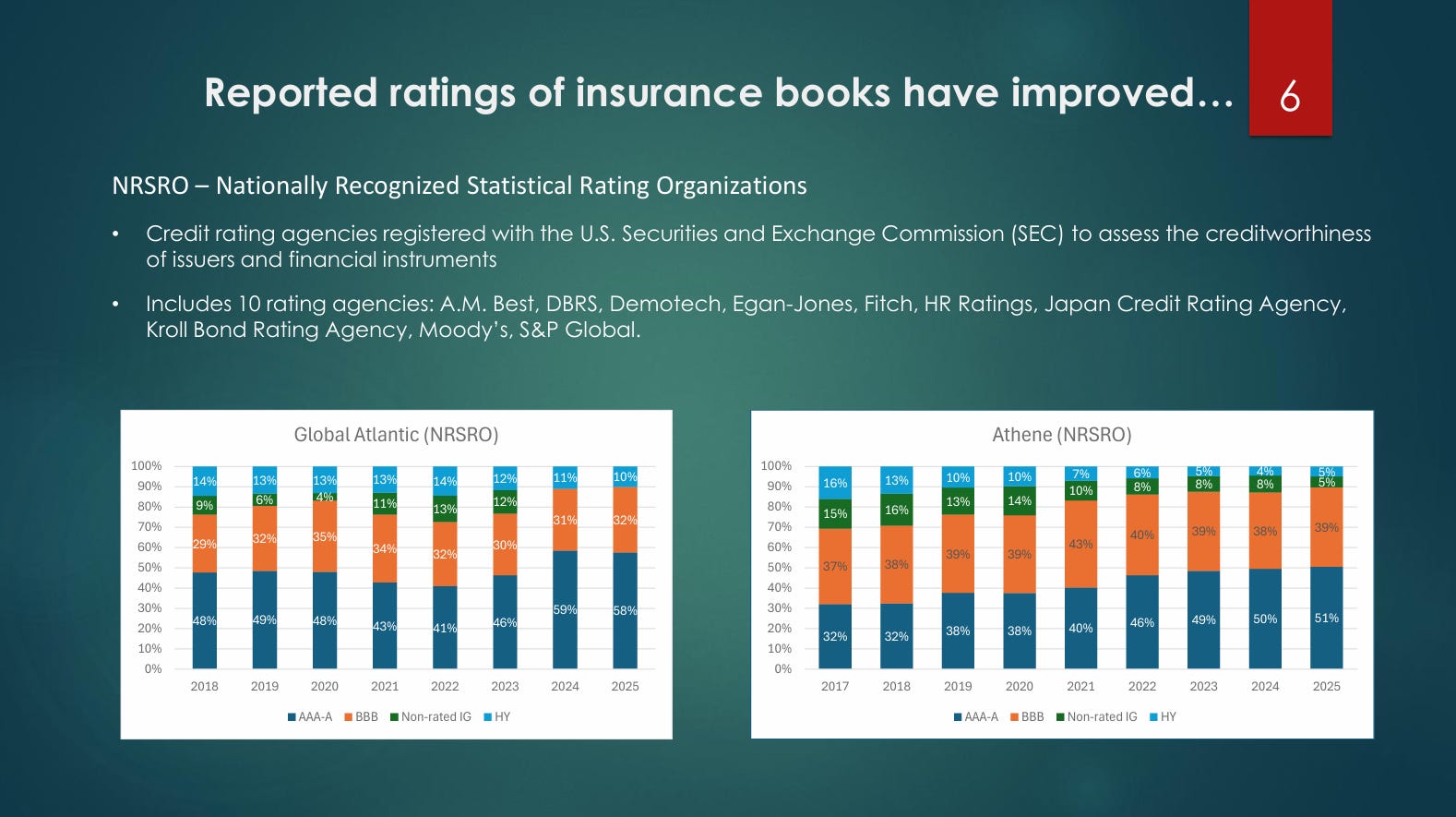

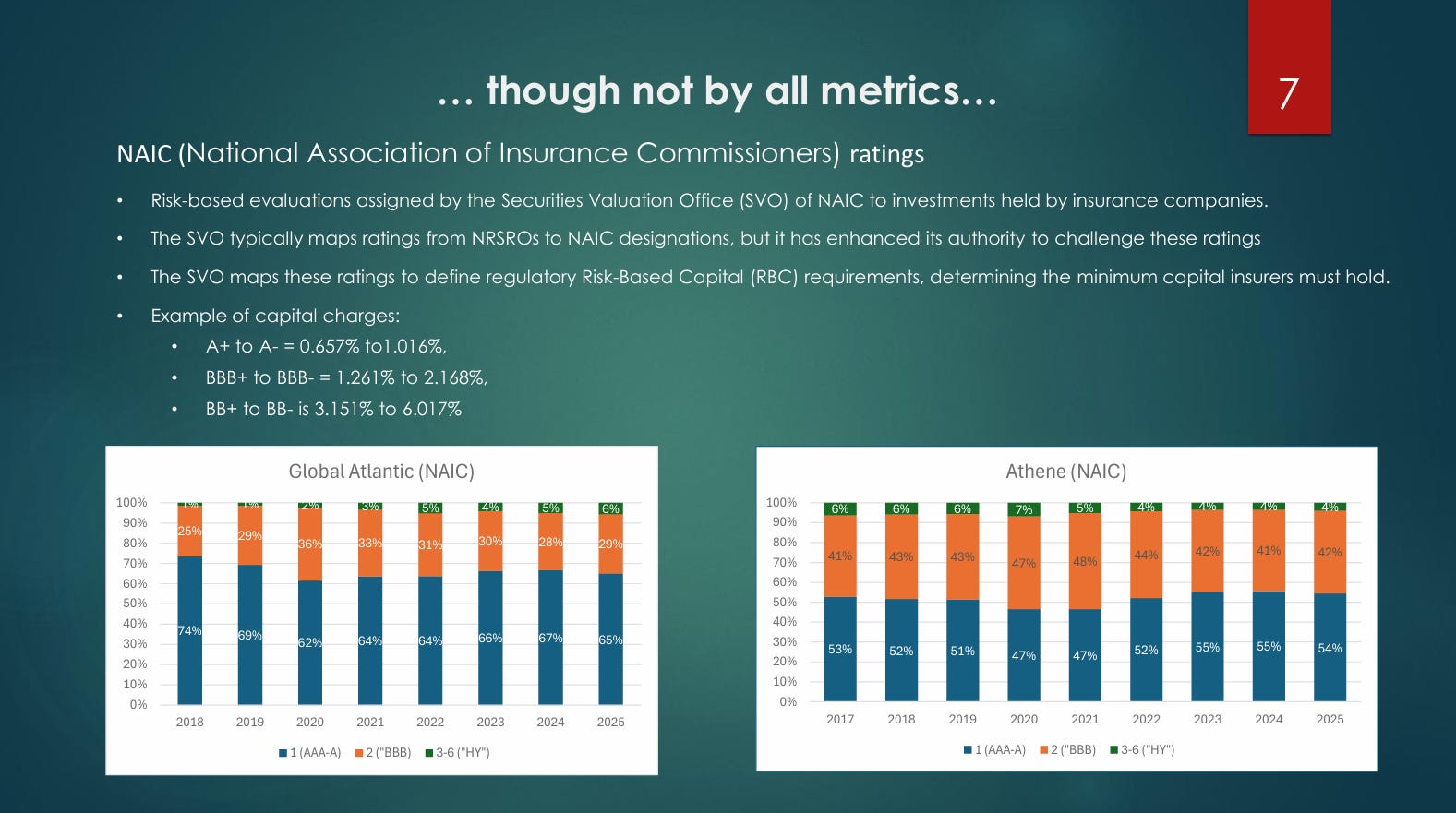

Asset Quality: The Ratings Puzzle

When one examines the credit profile of insurance portfolios, a striking pattern emerges: externally assessed ratings tell a significantly better story than regulatory ratings. NRSRO ratings (assigned by the nationally recognized agencies) show approximately 90% of insurance private credit holdings are investment grade. Analysis of public filings from major players shows the proportion of IG-rated holdings has either held steady or improved over time.

But NAIC ratings—assigned by the Securities Valuation Office (SVO), which has authority to challenge and override external ratings—tell a different story. The divergence is meaningful and growing for some insurers. This matters because capital requirements are tied directly to ratings:

An A- rated asset carries a capital charge of approximately 1%.

A BBB- rated asset carries approximately 2.2% (more than double).

A BB- rated asset carries approximately 6%.

A portfolio does not need to suffer actual defaults to experience stress. A wave of downgrades alone can increase capital requirements six-fold, instantly pressuring the insurer’s balance sheet.

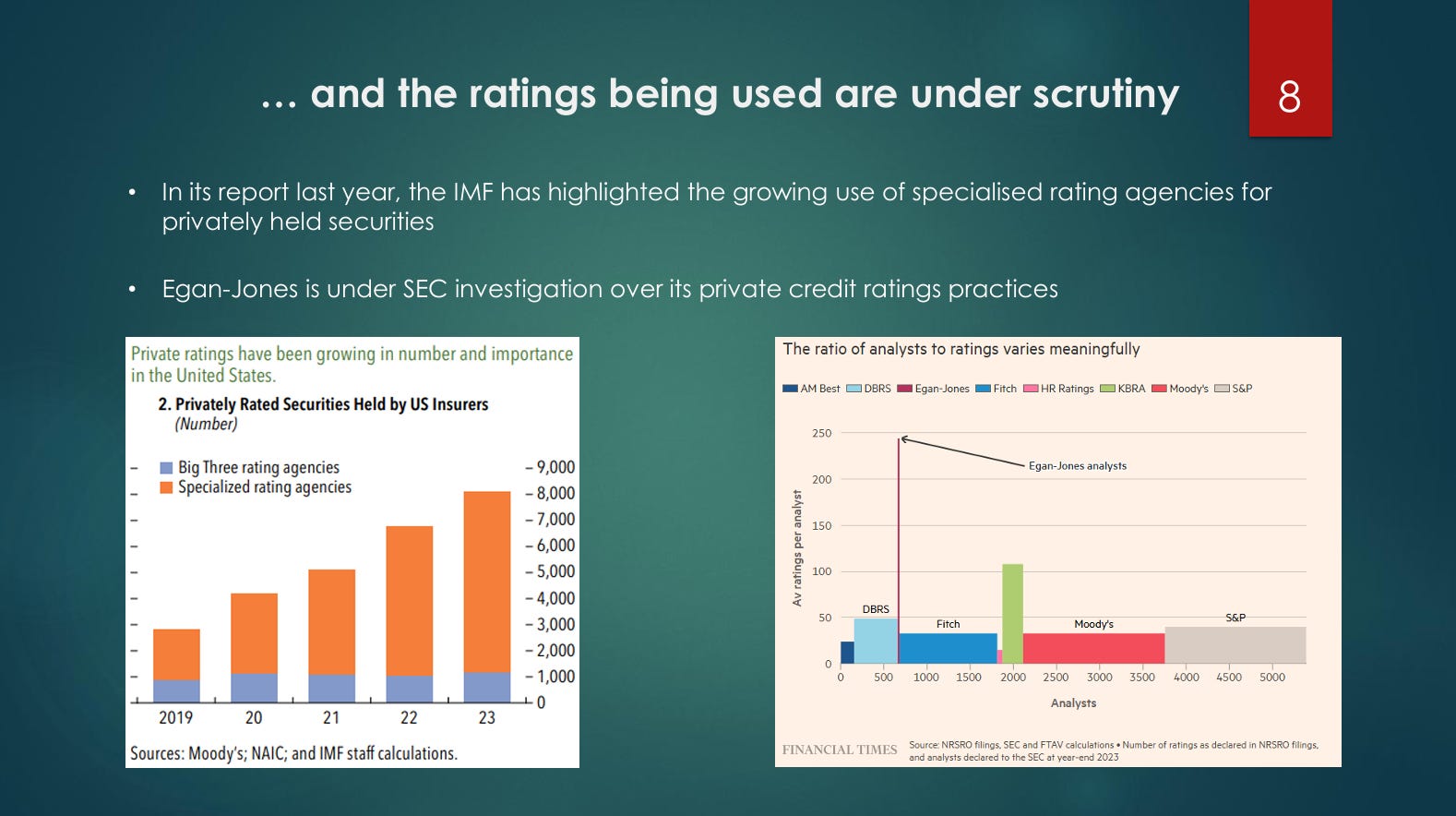

The credibility of these ratings is under active scrutiny. The IMF has flagged the explosive growth in specialized rating agencies since 2019, specifically agencies focused on private credit where large incumbents have stepped back. In November 2025, the SEC launched an investigation into Egan-Jones Ratings Company over its private credit rating practices, noting they assigned significantly more ratings per analyst than peers like Moody’s or S&P. If originators gravitate toward the most generous rating agency, portfolio distributions will skew optimistic.

Opaque Disclosures and Cross-Sector Comparisons

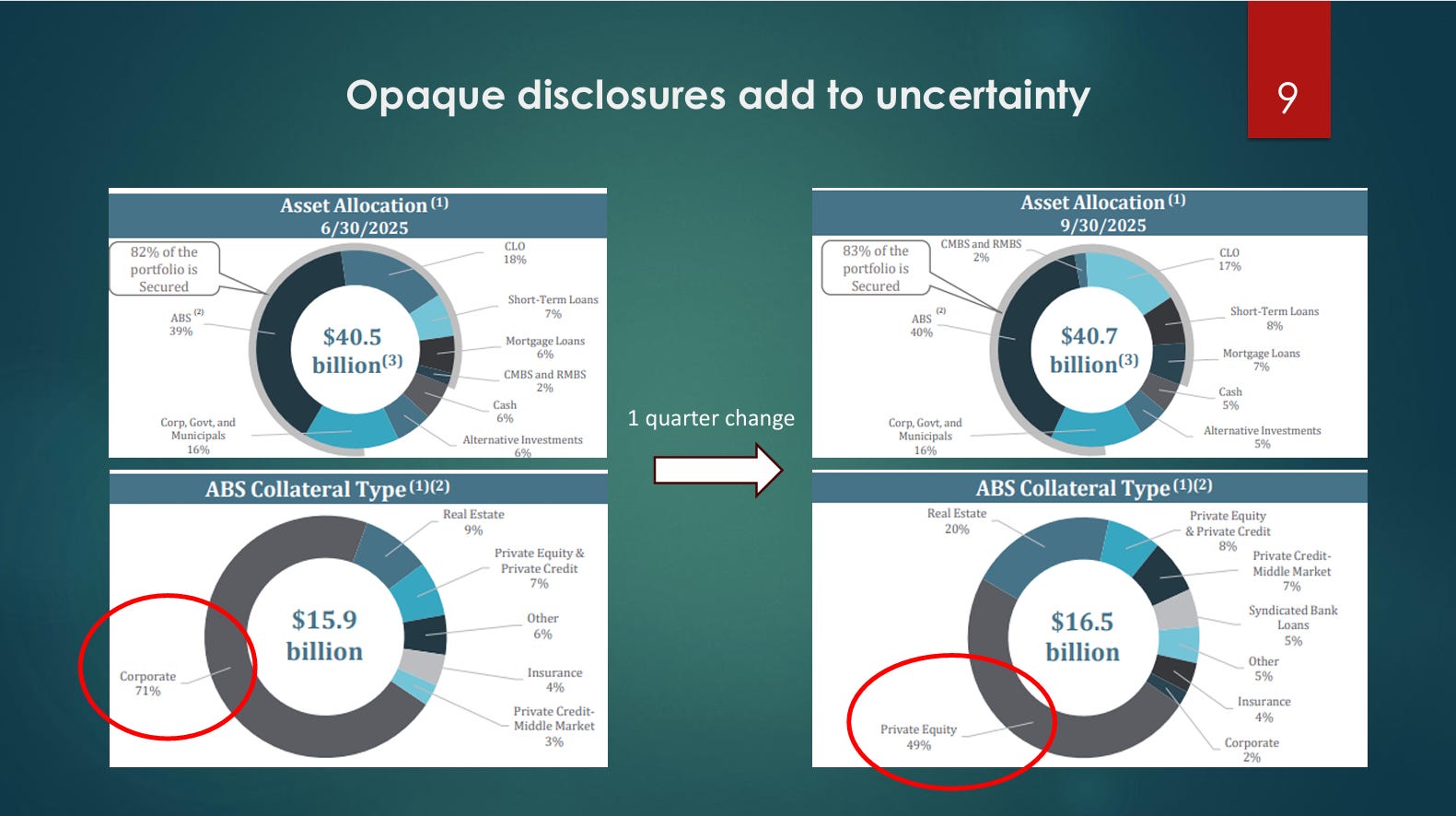

Anecdotal evidence reinforces the opacity concern. Between Q2 and Q3, Security Benefit reclassified its ABS holdings (representing 40% of total assets) from corporate exposure to a more granular breakdown. Nearly half of the ABS portfolio, or 20% of total asset allocation, was disclosed as being private equity. While the reclassification does not prove deterioration, it reveals an opacity that had previously concealed the true composition of the portfolio.

It is critical to distinguish insurance private credit from BDC private credit. BDCs hold largely single-B rated corporate loans with heavy software exposure. Insurers hold primarily IG-rated, diversified portfolios of private credit across various underlyings (real estate, infrastructure, ABS). The key risk for BDCs is actual defaults; the key risk for insurers is downgrades and regulatory recalibration.

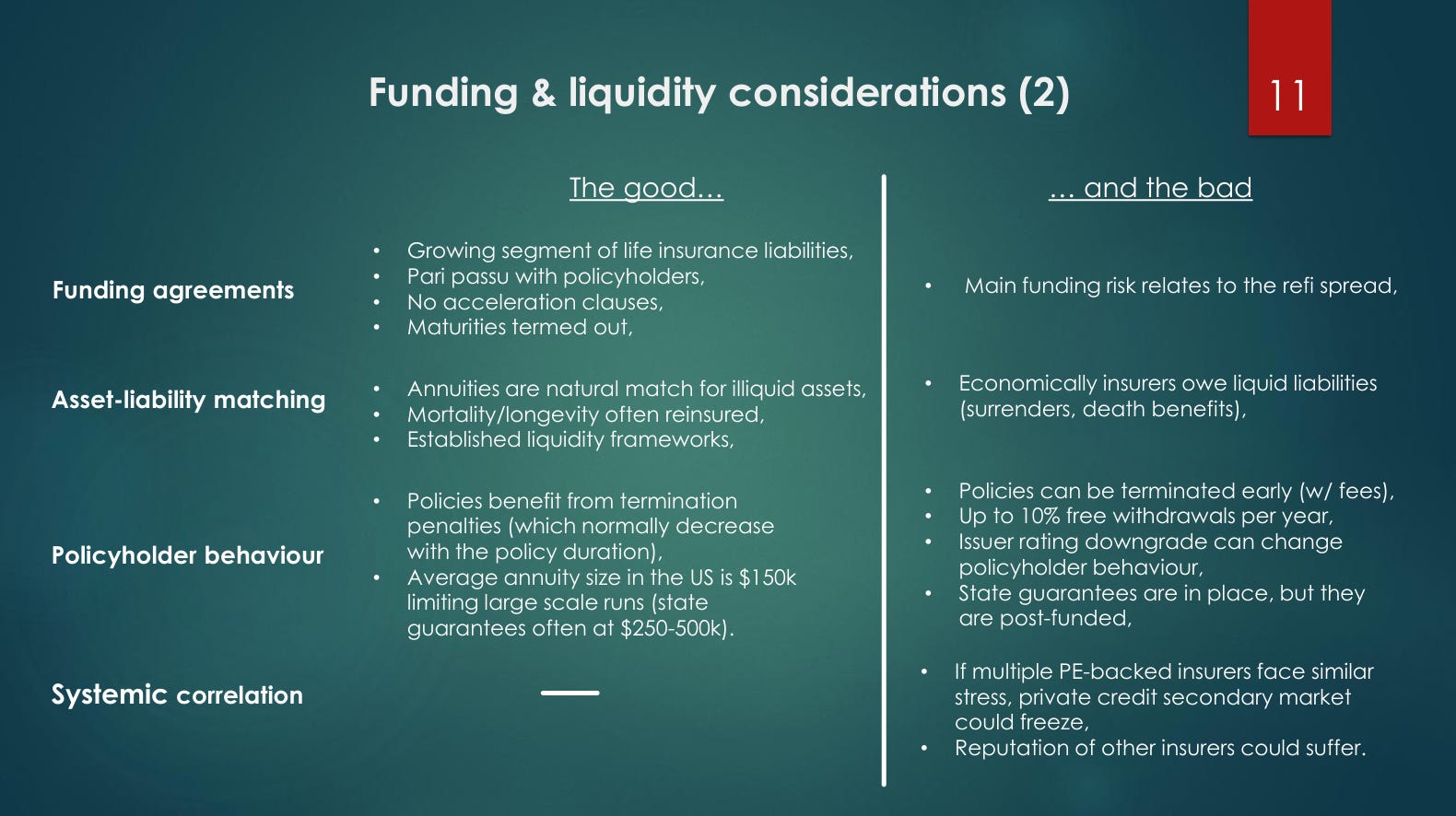

The Funding Side: Stability and the Liquidity Myth

Negative commentary often mischaracterizes the liquidity risk of life insurers. Recently, it was suggested on a major podcast that institutional investors holding funding agreements could theoretically call up Apollo and ask for $3 billion back from Athene Global, triggering a run.

This is structurally false. Funding Agreement-Backed Notes (FABNs) function like bonds, not demand deposits. They are pari passu with general policyholders, have termed-out maturities, and contain zero acceleration clauses triggered by asset deterioration, ratings downgrades, or market dislocation.

The real risk is a spread-widening and refinancing-cost vulnerability. If an insurer is downgraded or credit conditions tighten, the cost of refinancing matures liabilities spikes.

Beyond funding agreements, Apollo’s liability structure provides meaningful stability.

Looking at representative structures, approximately 50% of annuities carry withdrawal fees, and roughly 33% cannot be surrendered at all. Policyholders can withdraw up to 10% of principal penalty-free per year, and state-level guarantees provide coverage of $250,000 to $500,000 against an average annuity size of approximately $150,000. However, unlike FDIC bank deposit insurance, state guaranty funds are post-funded—capitalized through industry assessments only after a failure occurs, which can represent an element of concern for annuity holders (especially in a situation of several insurers failing in close succession).

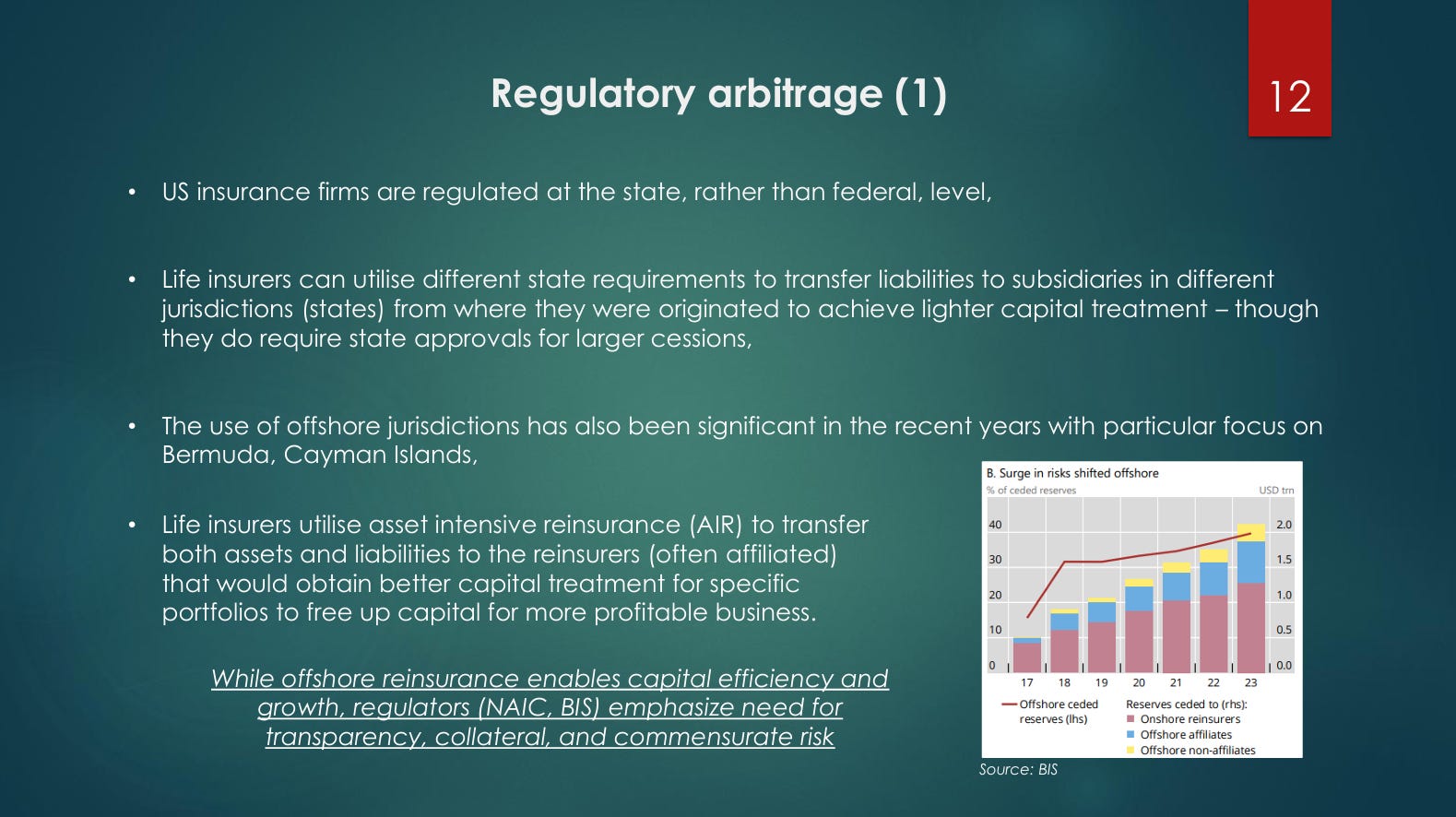

Regulatory Arbitrage: The Structural Risk

Insurance regulation in the US is primarily a state-level function, not federal, enabling arbitrage both across states and offshore. The Bank for International Settlements reported that approximately 40% of reserves have been ceded to offshore reinsurers.

The mechanism that has attracted the most scrutiny is Asset-Intensive Reinsurance (AIR). In AIR, the primary insurer transfers both assets and liabilities to a reinsurer—often an affiliated captive in Bermuda or the Cayman Islands. The return on transferred assets pays for the liability reinsurance, releasing significant capital.

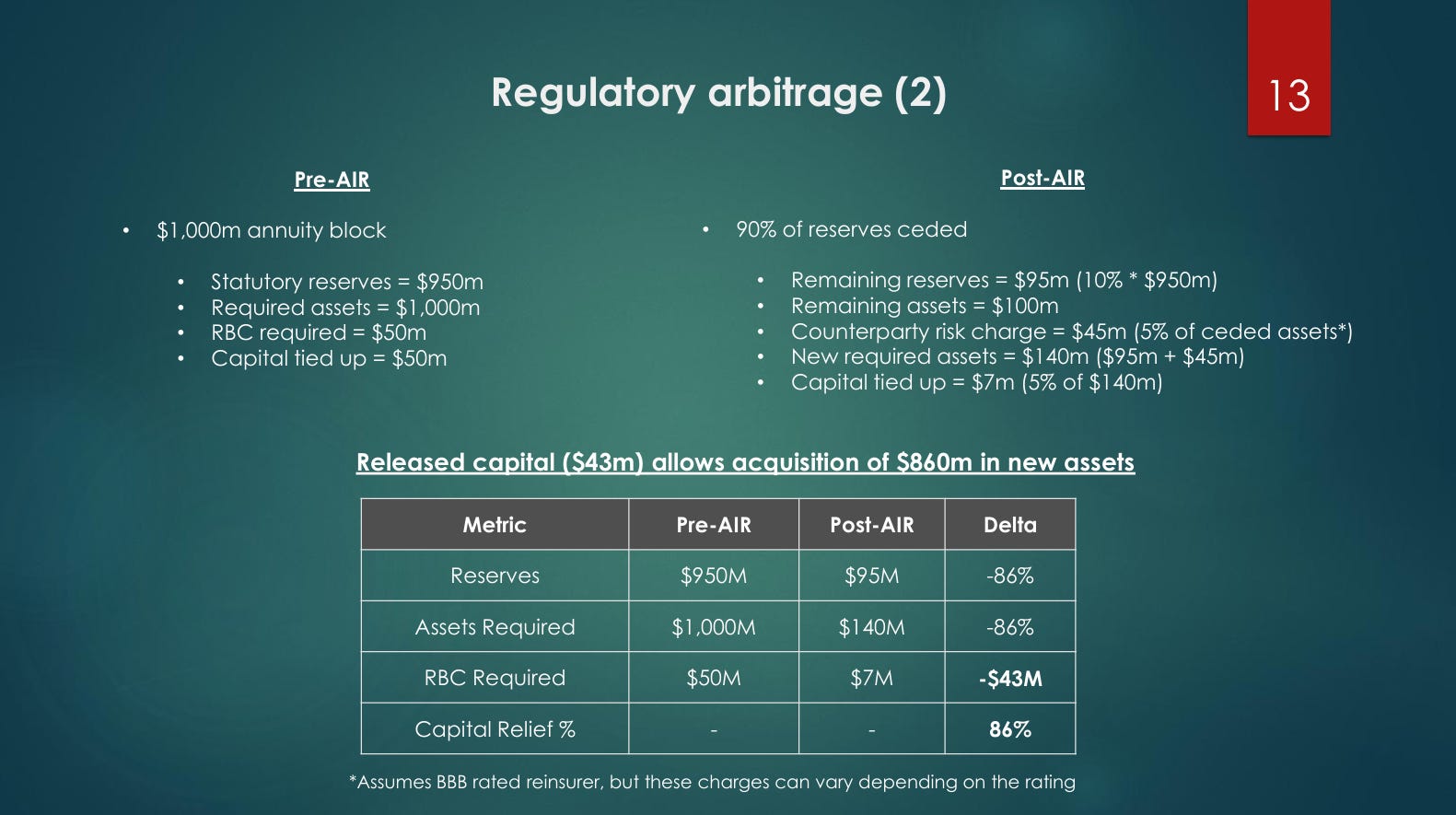

A concrete example highlights the leverage:

Start with a $1 billion annuity block ($950 million in reserves, $50 million in capital).

Cede 90% to the reinsurer. Reserves drop to $95 million.

Add a counterparty risk charge of approximately 5% at a BBB rating ($45 million).

New required assets equal $140 million. Capital tied up is just $7 million.

The transaction releases $43 million in capital, enabling the acquisition of $860 million in new assets.

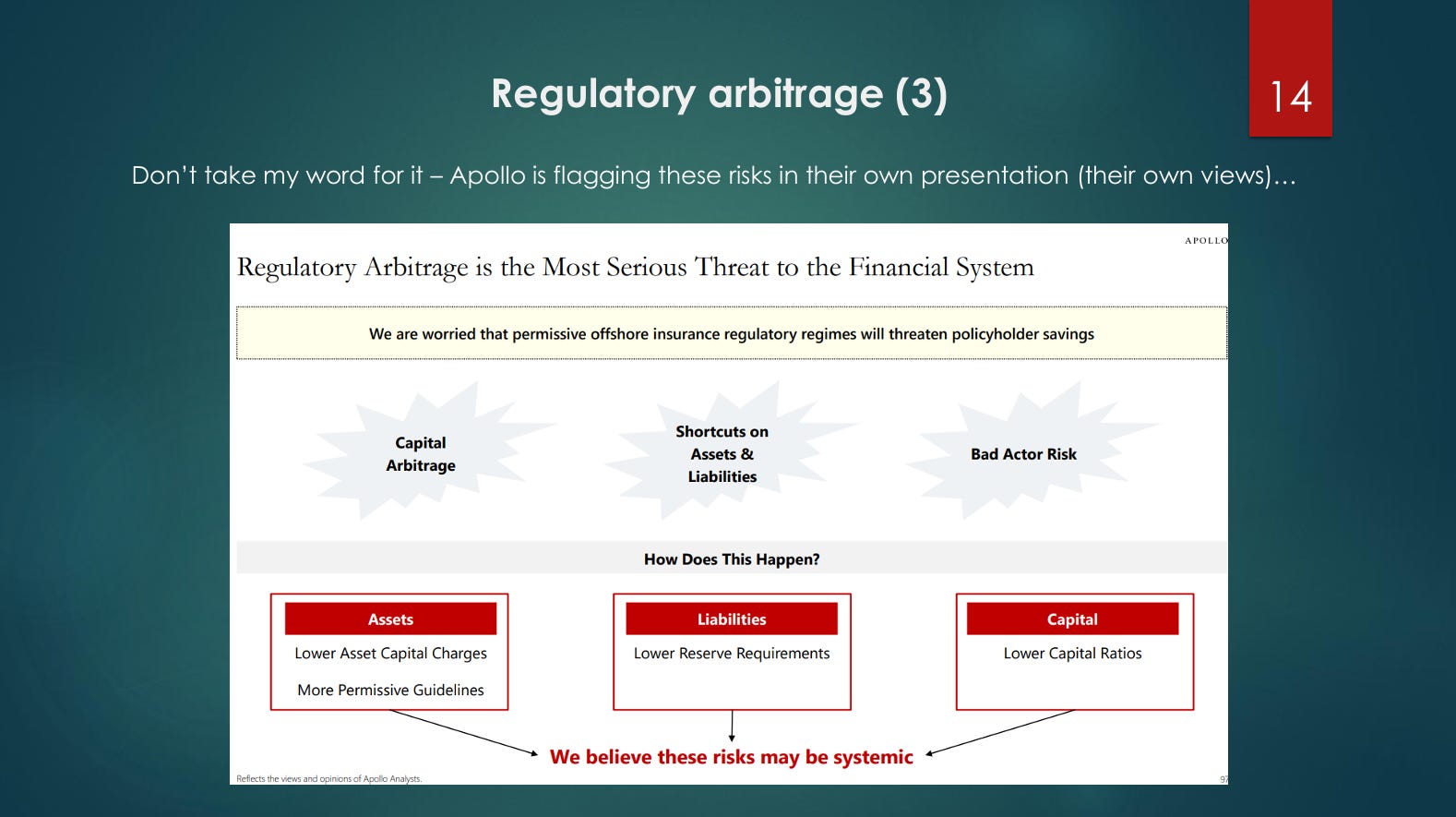

The tail risk is deeply concentrated. If the offshore reinsurer fails, the primary insurer must recapture both assets and liabilities, and that $43 million in capital relief evaporates instantly. In a revealing data point, Apollo flagged regulatory arbitrage in their own investor update as “the most serious threat to the financial system”.

2008 Echoes and Stress Scenarios

If the system faces stress, a clear hierarchy emerges:

Rating downgrades triggering capital calls: A move from A- to BBB- doubles the requirement. Evidence suggests ratings may warrant scrutiny, and the capital arithmetic is unforgiving.

Reinsurance counterparty stress: Concentrated offshore ceding means a single reinsurer failure forces recapture across multiple primary insurers simultaneously.

Default clusters: Widespread defaults would require a severe macro shock given the high IG concentration.

Policy surrender spikes: A tail risk, heavily mitigated by withdrawal penalties and liquidity buffers.

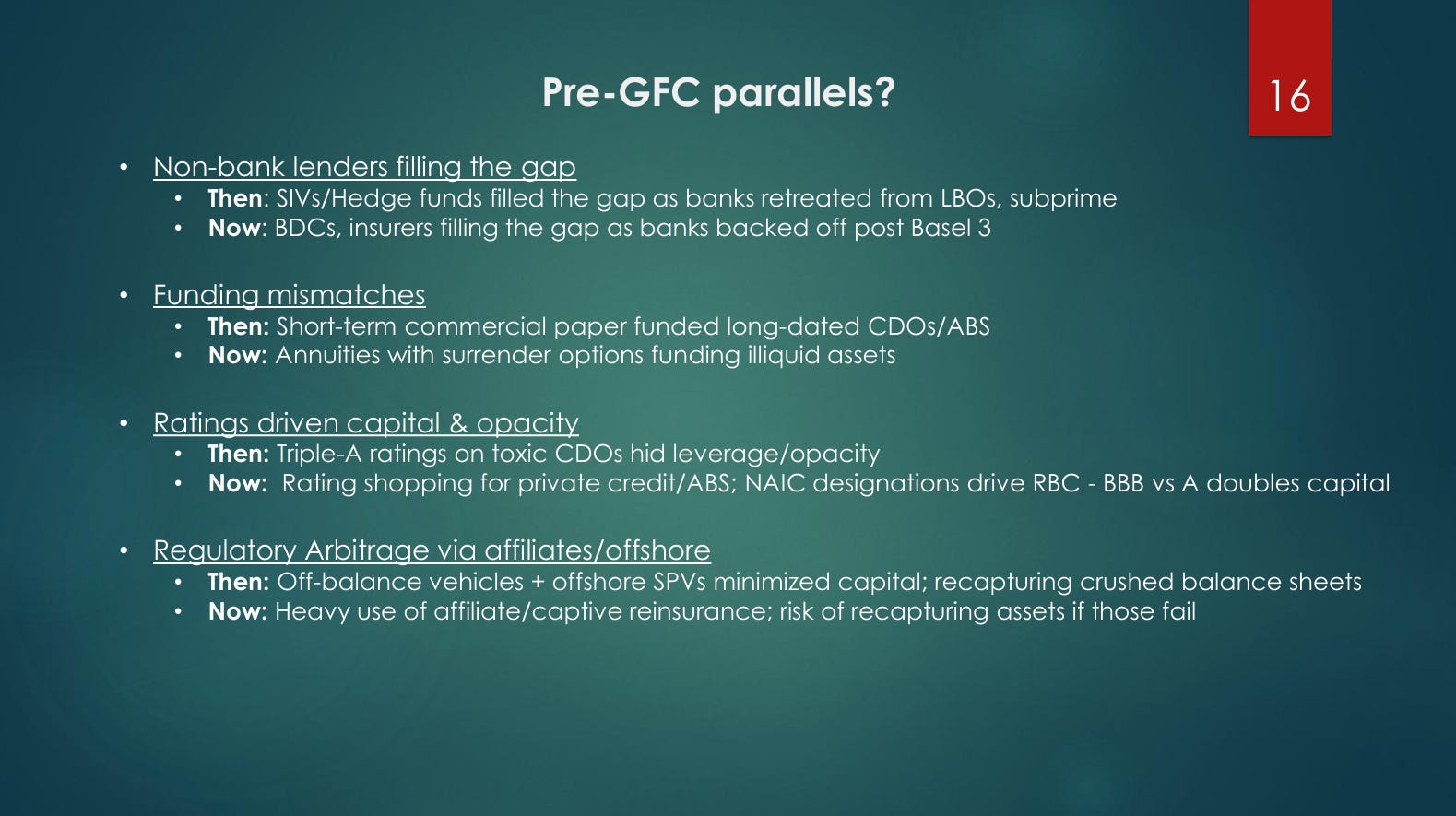

The structural parallels to the pre-GFC system are meaningful. Non-bank lenders are again filling a lending gap vacated by banks. Funding mismatches persist—surrenderable annuities funding illiquid private credit. Ratings-driven capital opacity remains, and regulatory arbitrage through offshore captive reinsurance mimics the off-balance-sheet SPVs of the past. The key difference today is the existence of state guaranty funds and NAIC regulatory oversight.

Conclusion

Insurance is a great home for illiquid assets, but only at the right price and when properly regulated. The key risk is mainly that the asset quality on private credit across various underlyings is lower than expected, which impairs the asset quality of the broader portfolio and drives up the capital requirements, eroding regulatory metrics.

Massive amounts of these risks have been shed to offshore captive reinsurers. If underlying assets underperform, those risks could come crashing back onto the primary balance sheets. Consequently, a vast amount of risk has been transferred into the insurance sector. Because this is a highly regulated sector, it could find itself undercapitalized—not purely from a sudden wave of borrower bankruptcies, but from the acute risk of regulatory recalibration and rating downgrades.

Listen to the full episode for Jakub’s takes on Insurance and private credit.

This article is based on Episode 10 of Fixed + Floating, featuring Jakub Lichwa of TwentyFour Asset Management. The views expressed are those of the speakers and do not constitute investment advice. For more information, please visit https://www.twentyfouram.com/.

Fixed + Floating is a credit podcast for institutional investors and finance professionals — exploring the forces shaping global credit markets. Hosted by credit PM Josef Pschorn, the show features conversations with leading voices from investing, research, and academia.

Support Material:

Great article really don't understand the lack of readers here. That's soon to change I'm sure