Why Software Credits Are LME Catnip

E11 — Sabrina Fox (Fox Legal Training) explains, why industrial‑era covenant packages on IP‑heavy borrowers have turned software into the easiest sector to strip and prime.

Software has quietly become the easiest sector in leveraged credit to strip, prime, and re-cut through liability management exercises. This piece explains why. We start from first principles of what covenants actually protect, show why a single “covenant quality score” cannot capture LME risk, and walk through a practical taxonomy of LMEs — drop-downs, up-tiers, double-dips, and extend-and-exchange — with Xerox and ION Platform as live case studies.

The article closes with a five-line checklist you can run on any software deal in ten minutes to decide whether you’re being paid for the documentation risk.

This is the third part of a software arc on Fixed + Floating. For context on software business models and leverage, see:

Covenant Erosion and the Normalisation of LMEs

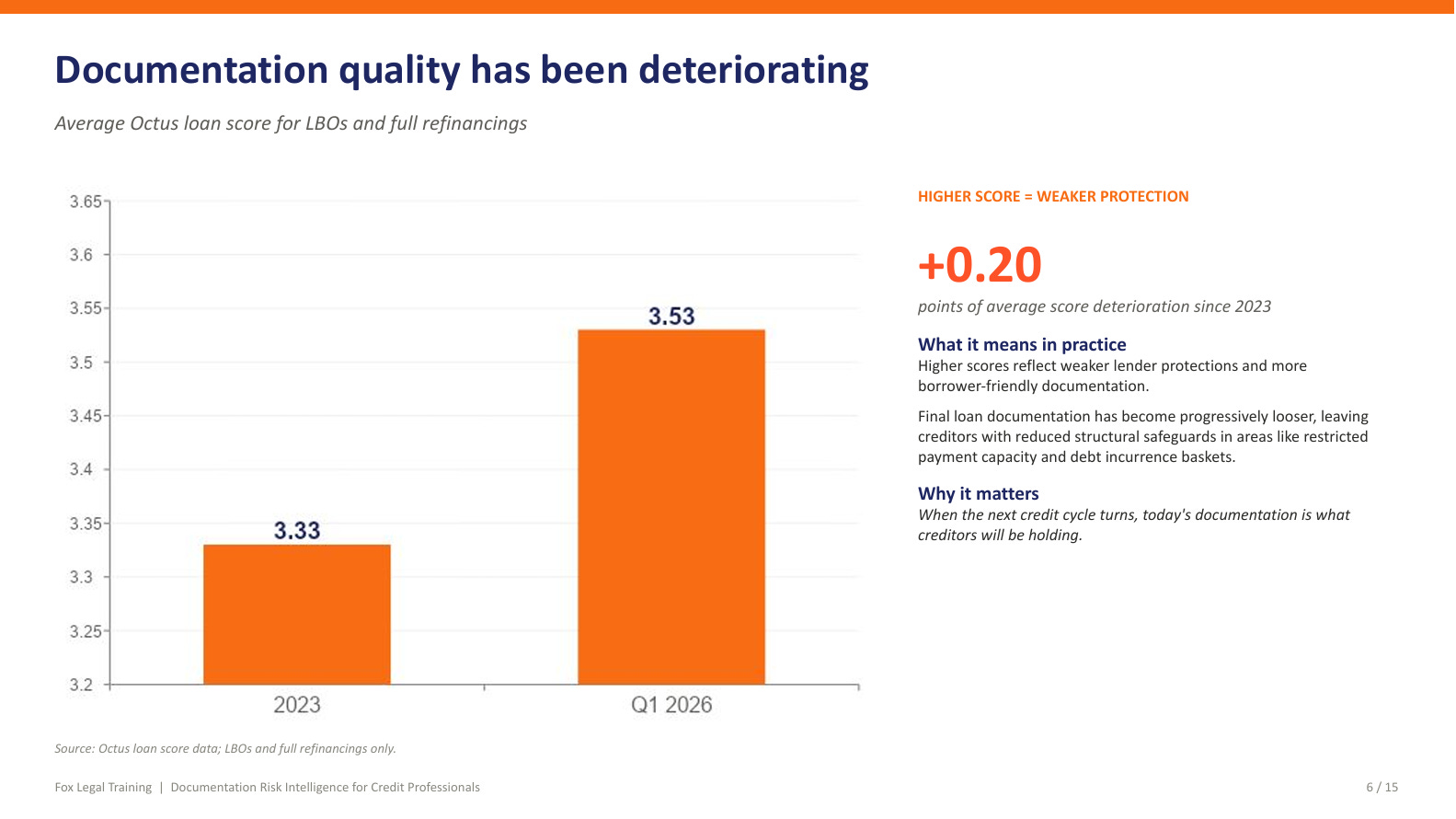

Octus data shows the average LBO and refinancing covenant quality score deteriorated from 3.33 in 2023 to 3.53 in Q1 2026, on a scale where higher means worse. That number understates the problem. The starting point was already weak — covenant quality had been eroding systematically through the 2010s, meaning the recent decline compounds on a base that would have alarmed most credit committees a decade ago.

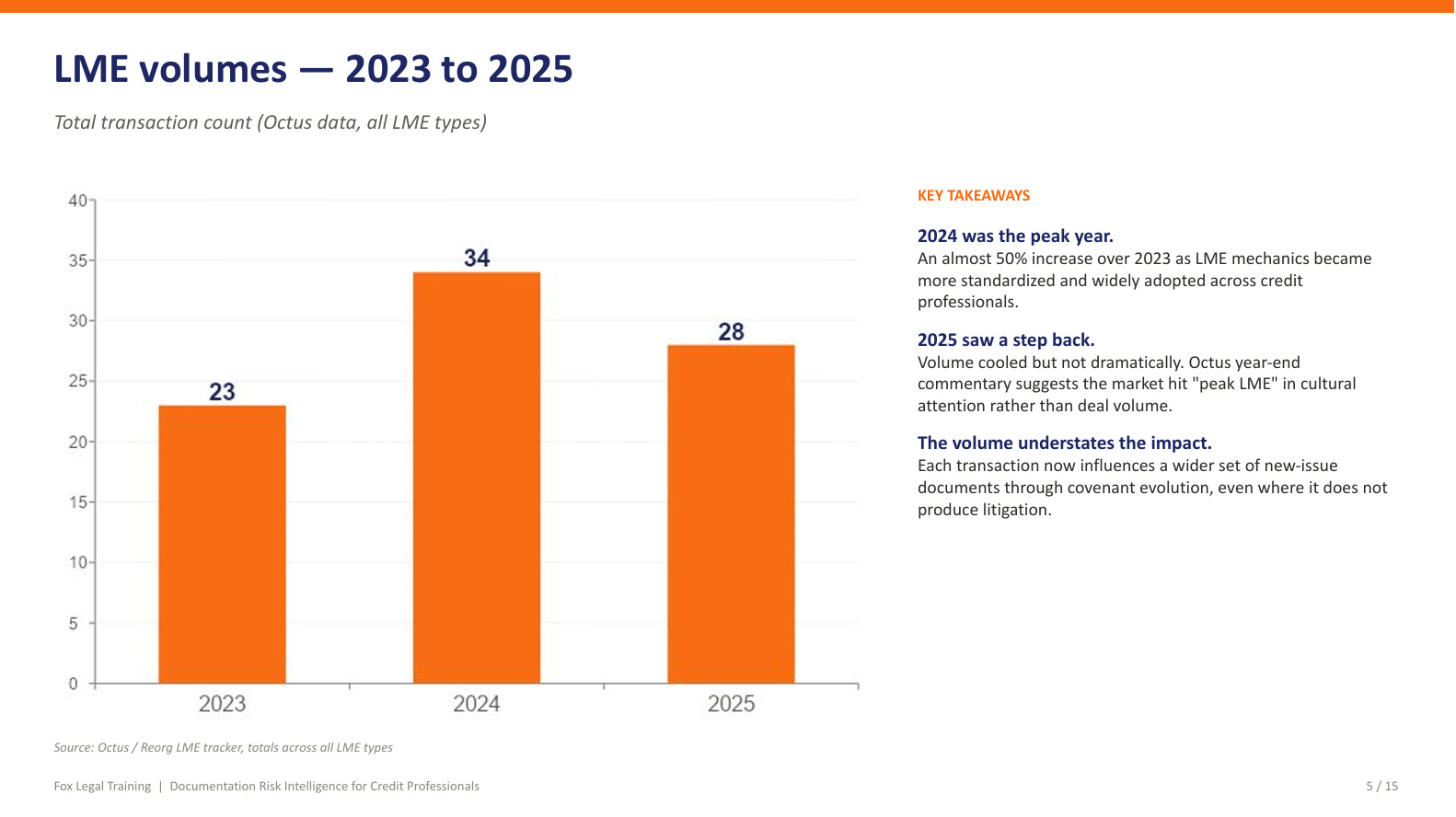

In 2024, 34 liability management exercises were executed across leveraged credit markets, up from 23 in 2023, before moderating to 28 in 2025. LMEs have become a recurring feature of credit markets, not an anomaly. And software credits — the sector that now dominates leveraged finance deal flow — carry the same covenant packages as any other leveraged buyout, despite having an asset profile that makes them uniquely vulnerable to the mechanisms LMEs exploit.

First Principles: What Covenants Are Actually Protecting

Before examining specific LME structures, the analytical framework requires grounding in what covenants are designed to do. The most important promise in a credit instrument is repayment of principal at maturity. Every other covenant exists to protect that promise — either by protecting the credit quality of the borrower or by protecting the lender’s position in the capital structure.

Credit quality covenantskeep value inside the restricted group.

Restricted payment covenants prevent the borrower from distributing cash to equity holders.

Asset sale covenants ensure that when assets are disposed, proceeds either stay in the business or are used to repay debt.

Affiliate transaction covenants prevent value transfers to related parties at non-arm’s-length terms.

Change of control provisions give lenders an exit if ownership shifts in ways that could alter the credit profile.

Capital structure covenants protect the lender’s relative priority.

Debt and lien covenants control the borrower’s ability to raise additional secured or structurally senior debt, preventing dilution of the existing lenders’ recovery position. These are the covenants that, when loosely drafted, enable up-tier and double-dip transactions.

Imagine the borrower exercises every flexibility the documentation permits — every permitted payment, every permitted investment, every incremental facility, every asset sale basket. Would you still lend at this coupon? If the answer is no, the covenant package is mispriced.

“If you invest based only on your analysis of the credit, you’re only investing based on half the story because the contract tells the other half.”

That framing is deceptively simple. In practice, most credit analysts spend their time on enterprise value, cash flow, and leverage — the credit fundamentals. The contract analysis is often delegated or treated as a checklist exercise. This approach systematically underweights the optionality embedded in the documentation — optionality that becomes decisive precisely when credit quality deteriorates and LME teams begin looking for openings.

Pricing Covenant Quality: Why a Single Number Falls Short

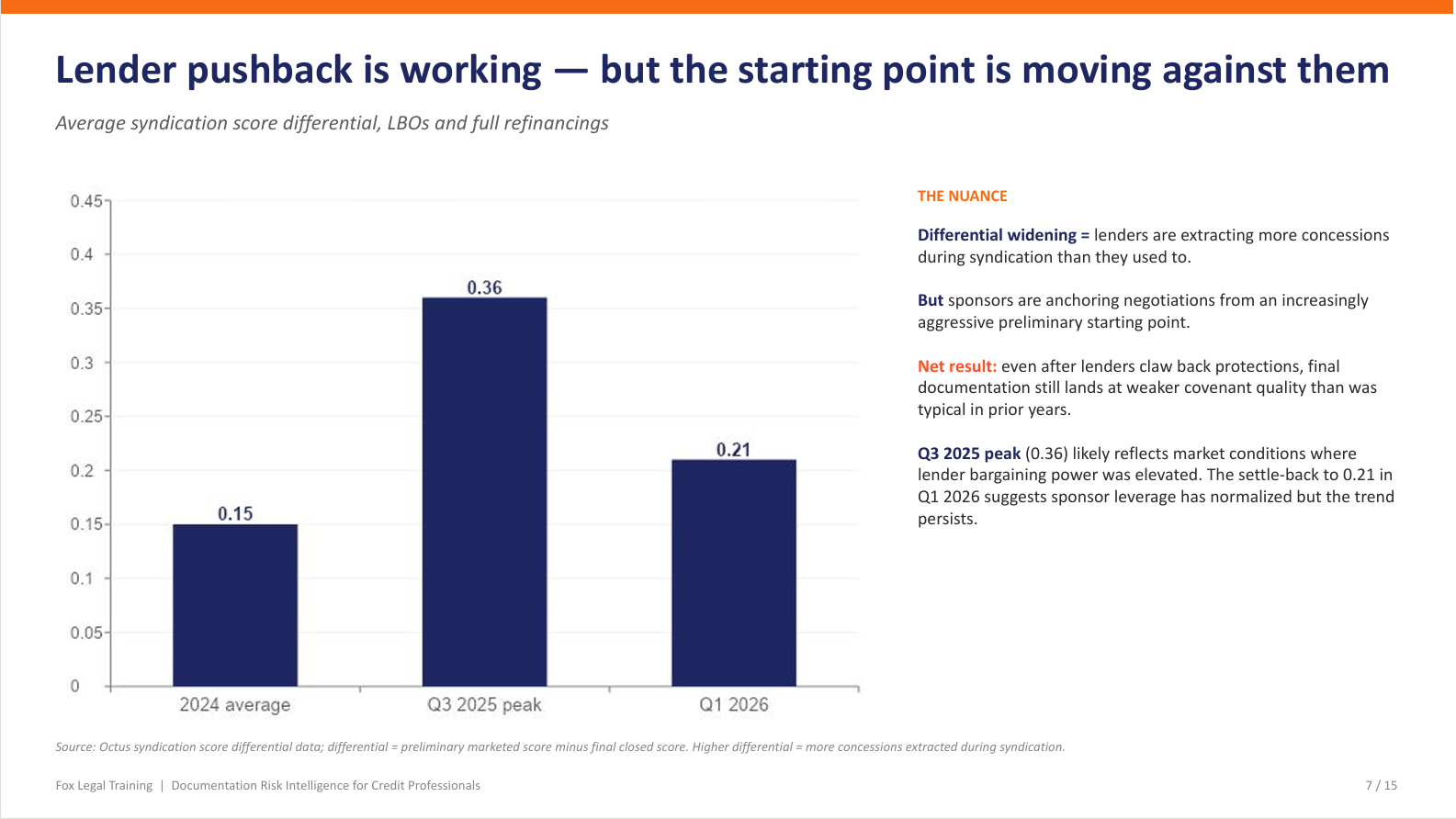

One question I raised with Sabrina was whether covenant quality can be reduced to a basis-point adjustment — some quantitative measure that maps weaker covenants to wider spreads. Her answer was unambiguous: it cannot.

The difficulty is that covenant provisions are not independent variables. A generous permitted investment basket is benign for a borrower with no transferable assets but lethal for a software company whose entire enterprise value resides in intellectual property that can be moved between entities overnight. A loose FMV determination clause — one that allows fair market value to be assessed by the board without independent third-party valuation — is irrelevant when the borrower holds physical plant and equipment but becomes a mechanism for value extraction when the primary asset is IP that can be valued flexibly.

In the Akzo Nobel deal, lenders were able to force a materially higher coupon in exchange for keeping specific asset sale and distribution protections. That transaction shows that the market will sometimes price documentation — but the spread premium was highly specific to that issuer, capital structure, and set of clauses. Generalising from a handful of such cases into a “covenant basis-point premium” is analytically unsound.

In simpler terms, covenant quality is a facts-and-circumstances analysis. It depends on who the borrower is, what assets they own, what they are likely to do under stress, and which specific provisions interact to create or foreclose flexibility. The Octus score is a useful directional indicator. It is not a substitute for reading the documents.

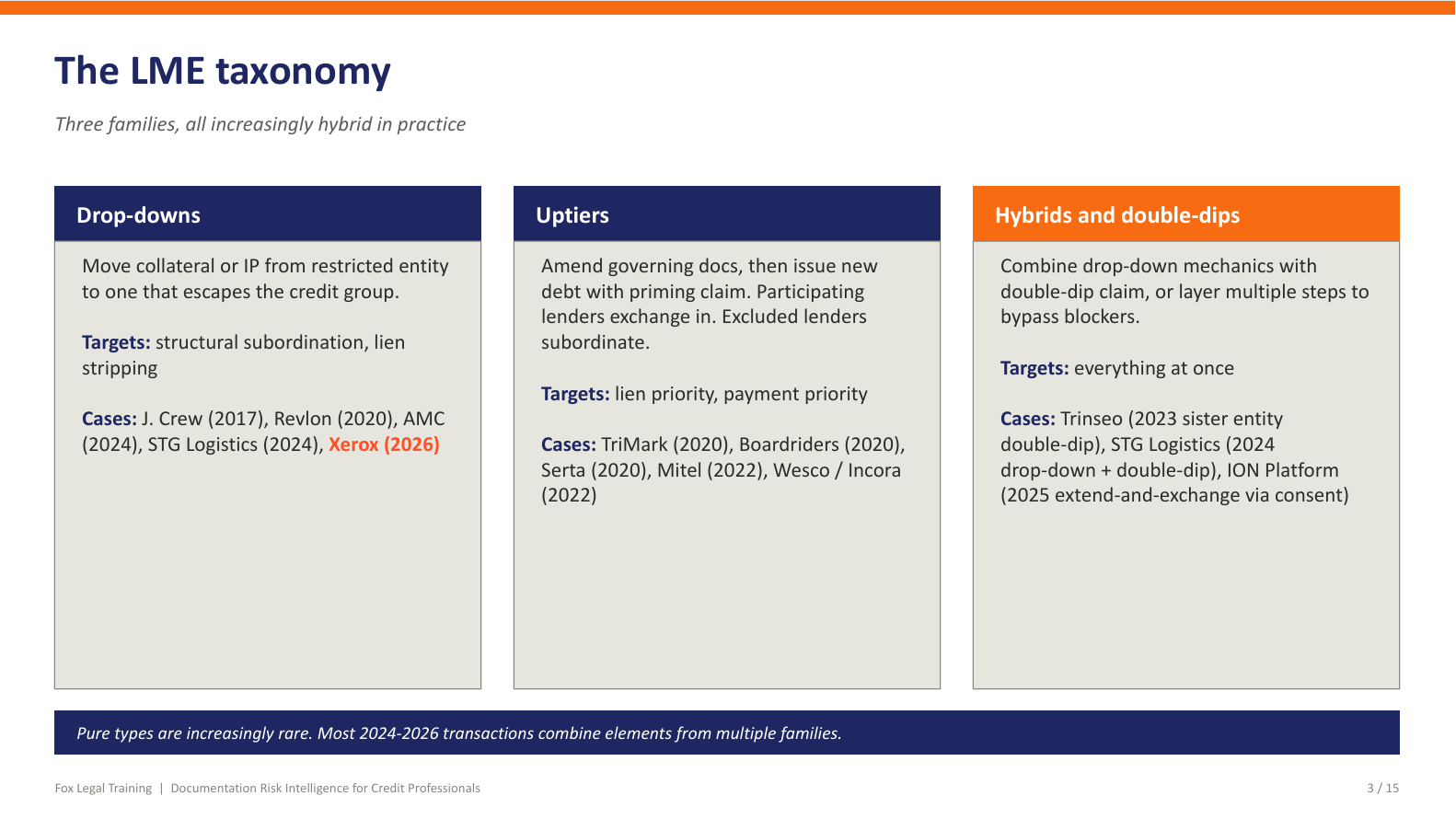

The LME Taxonomy: Four Mechanisms, One Objective

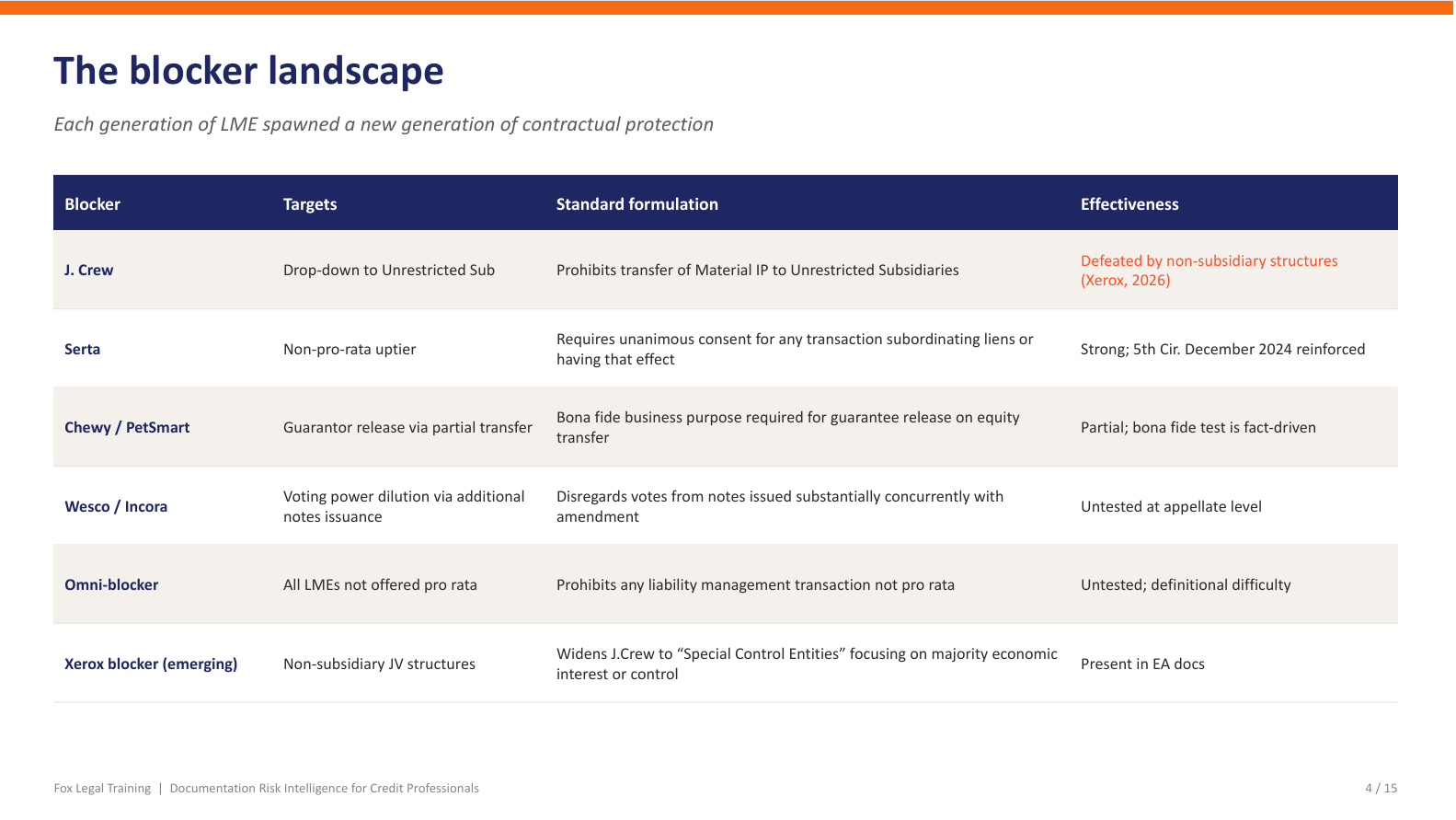

LMEs are not a single transaction type. They are a family of related strategies, all aimed at improving the position of the borrower (or a subset of lenders) at the expense of remaining creditors. The taxonomy has expanded rapidly since 2020, and each new structure tends to prompt a corresponding blocker clause — which in turn prompts the next innovation.

Drop-Down Transactions

The drop-down is the oldest and most intuitive LME structure, and the J.Crew transaction of 2017 remains its archetype. The mechanics are straightforward: the borrower identifies valuable assets — typically intellectual property — and transfers them to an unrestricted subsidiary. An unrestricted subsidiary sits outside the restricted group, meaning it is not bound by the covenants in the credit agreement and its assets are not encumbered by the existing security package. Once the IP resides in the unrestricted subsidiary, the borrower raises new debt against it, effectively priming existing lenders by removing their best collateral.

The process in a software credit follows a predictable sequence. The borrower designates or creates an unrestricted subsidiary. It transfers IP to that entity, relying on permitted investment baskets that allow investments in unrestricted subsidiaries up to a defined capacity — often linked to a percentage of total assets or an EBITDA-based formula. The board determines the fair market value of the transferred IP, typically without any requirement for an independent third-party valuation. The IP is then licensed back to the operating company, ensuring no operational disruption. The unrestricted subsidiary raises secured debt against the IP.

Software IP is uniquely suited to this mechanism. It is the most valuable asset in the enterprise. It is the most portable — unlike a factory or a fleet, it can be transferred between entities with a board resolution and a licensing agreement. It can be valued flexibly because there is no liquid market establishing a reference price. And it can be licensed back without any observable change to the business’s operations. A manufacturing company that transferred its plant to an unrestricted subsidiary would need to shut down production. A software company that transfers its source code licenses it back the same day.

“Software deals have the same covenant packages as other leveraged finance deals — but the flexibility applies like a ticking time bomb because of IP portability.”

This is the central paradox. The documentation was designed for industrial borrowers with fixed assets. Applied to software companies, the same provisions create vastly more flexibility because the asset characteristics are fundamentally different.

Up-Tier Transactions

The up-tier — with the Serta transaction as its defining case — operates differently. Rather than moving collateral out, the borrower provides preferential security or priority to a select group of existing lenders willing to provide new money or consent to amended terms. The remaining lenders — those who did not participate — find themselves subordinated within the capital structure without having agreed to anything.

The mechanics rely on open market purchase provisions or voting thresholds that allow a simple or qualified majority of lenders to amend key terms, combined with covenant flexibility that permits the issuance of new super-priority debt. A subset of lenders negotiates directly with the borrower, often under NDA. Non-participating lenders may be “finding out in the paper the next day.”

The provisions that enable up-tier transactions are primarily found in the debt and lien covenants — specifically, in the definitions of permitted debt, permitted liens, and the conditions under which new debt can be issued with priority over existing obligations. When these provisions allow secured debt to be raised at entities above or alongside the existing borrower group, existing lenders’ recovery priority is diluted.

Double-Dip Transactions

The double-dip — with the At Home transaction as the reference case — is structurally more complex. It uses existing contractual provisions in combination to provide certain lenders with multiple avenues of recovery against the same asset base. The mechanism typically involves transaction security provisions that allow specific intercompany arrangements to create additional claims — effectively enabling a single dollar of new money to have two separate paths to recovery.

In practice, a double-dip might involve a lender providing financing at one entity and simultaneously receiving an intercompany loan claim at another entity within the group, such that both claims have security over group assets. The result is that the participating lender’s effective recovery rate is significantly enhanced relative to non-participating lenders, without additional capital being injected into the business.

Extend and Exchange

The most recent evolution in the LME toolkit is the extend and exchange — a category that encompasses consent solicitations to extend maturities, create new loan classes, and restructure existing instruments. The transactions at Better Health, Oregon Tool, and ION Platform illustrate this approach.

These transactions have become more prominent in part because post-Serta contractual innovations have made traditional up-tier transactions harder to execute. Borrowers and their advisors have adapted by using exchange offers and consent solicitations that achieve similar economic objectives — improving the position of participating lenders and extending the borrower’s liquidity runway — while working within or around the contractual restrictions specifically designed to prevent Serta-style up-tiers.

Why Software Is the Sector That Should Concern You

The intersection of deteriorating covenant quality and software-specific asset characteristics creates a compounding vulnerability.

Software credits have no maintenance covenants in their loan agreements — a trend that has become near-universal across leveraged lending. Maintenance covenants — tested quarterly, requiring the borrower to maintain leverage or coverage ratios — provided an early warning mechanism. When a borrower breached a maintenance covenant, lenders had the right to negotiate, amend, and potentially accelerate. Without them, the first sign of credit stress may be a missed coupon payment, by which time the borrower’s restructuring advisors have already been working on an LME for months.

The IP transfer mechanism described above applies with particular force to software. The most valuable asset is also the most portable. Board discretion over fair market value, the absence of third-party valuation requirements, and the ability to license IP back without operational disruption — all standard features of leveraged finance documentation — combine to make the drop-down a low-friction exercise for software borrowers.

The covenant packages themselves are undifferentiated. Software deals receive the same incurrence-based covenant architecture as any leveraged buyout — chemicals, healthcare, industrials. The permitted investment baskets, restricted payment capacity, and unrestricted subsidiary designation mechanics are functionally identical. But the consequences of exercising that flexibility are radically different when the borrower’s enterprise value is concentrated in transferable intangible assets rather than dispersed across physical plant, inventory, and customer contracts.

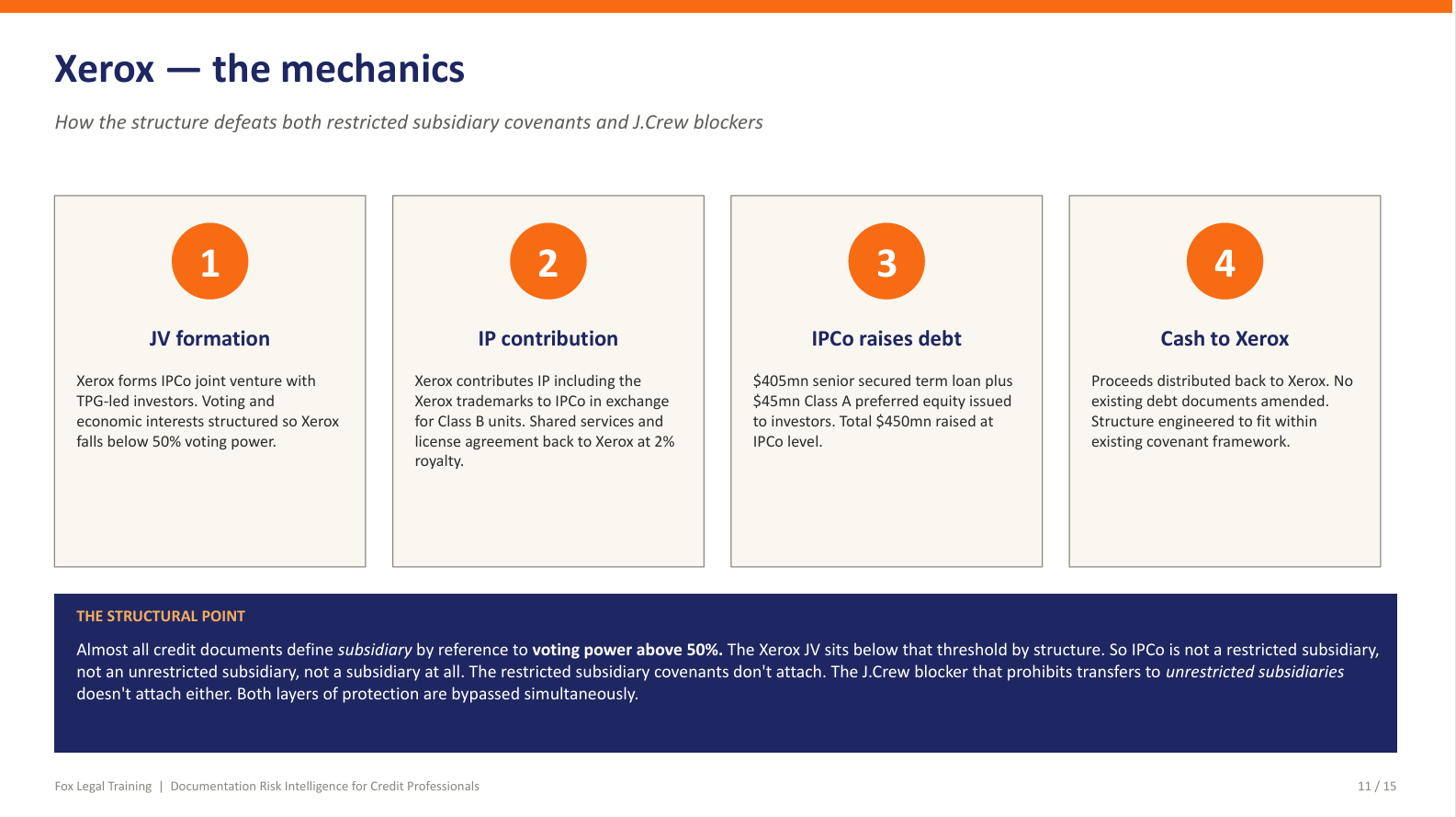

Case Study: Xerox and the Joint Venture Innovation

The Xerox transaction illustrates how LME innovation outpaces the contractual blockers designed to prevent it.

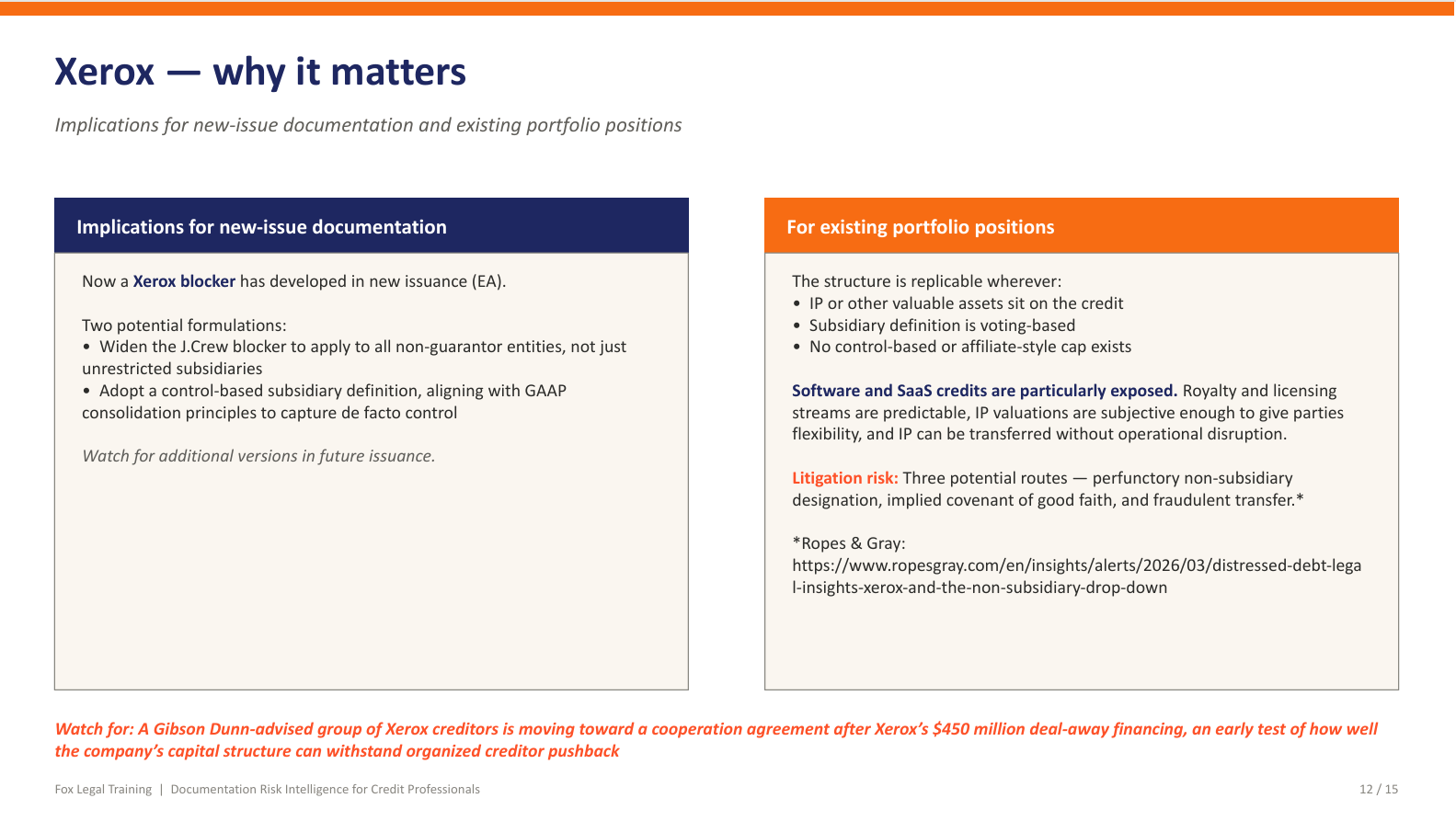

Xerox is a legacy hardware issuer in the process of pivoting to software, carrying a heavy maturity profile. The company needed to raise capital and restructure its liabilities. The standard drop-down playbook — transfer IP to an unrestricted subsidiary, raise debt against it — was foreclosed by a J.Crew blocker in the existing documentation. J.Crew blockers, which became standard in post-2017 documentation, specifically prohibit the transfer of material intellectual property to unrestricted subsidiaries.

Xerox’s advisors found an alternative. Instead of transferring assets to a subsidiary, they moved assets into a joint venture. The JV was structured so that Xerox retained majority economic ownership but held less than 50% of voting power. The critical insight is definitional: under standard leveraged finance documentation, a subsidiary is defined by reference to voting power — specifically, ownership of more than 50% of the voting stock. A joint venture in which the borrower holds less than 50% of the votes is not a subsidiary under the documents, even if the borrower receives the majority of the economic returns.

Because the JV was not a subsidiary, it was not an unrestricted subsidiary. Because it was not an unrestricted subsidiary, the J.Crew blocker — which applies specifically to transfers to unrestricted subsidiaries — did not apply. The IP was transferred to the JV, which then co-invested it to produce proceeds that flowed back to the Xerox structure.

This is what we can call the Easter egg approach to documentation. Restructuring teams execute a novel transaction, and then advise the capital markets teams at their firms to embed the enabling provisions — or the absence of blockers — in the next round of new issuance documentation. The market adapts, but always with a lag. The Pfleiderer transaction demonstrated a related innovation: rather than transferring assets to an unrestricted subsidiary, the borrower simply sold them outright, generating proceeds outside the restricted group.

The broader takeaway from Xerox is that capital structures are becoming more complicated without solving the underlying credit problem. No deleveraging occurred. Maturity was extended. Liquidity was created. But the fundamental question — whether the enterprise can generate sufficient cash flow to service its obligations — was deferred, not resolved.

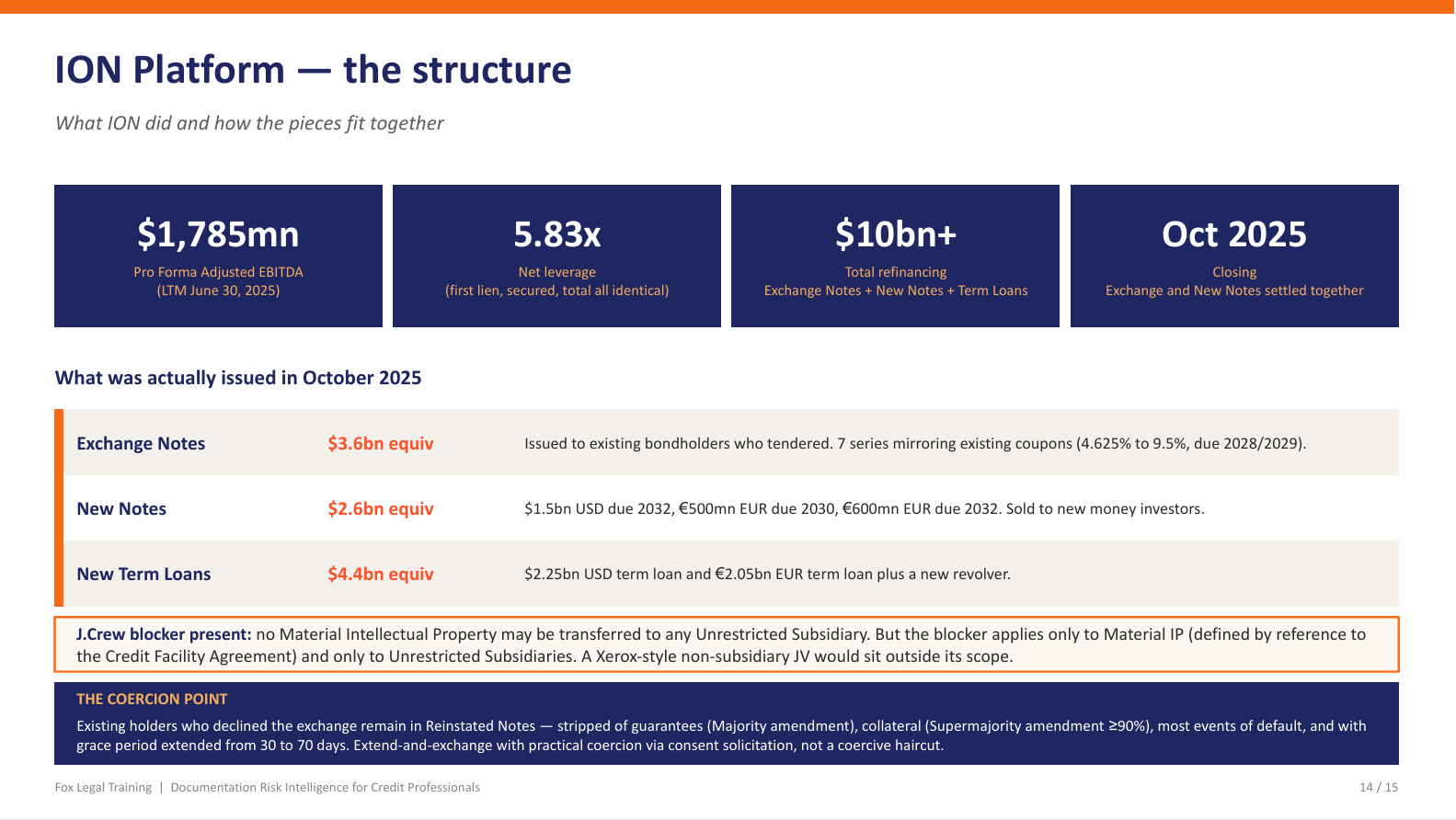

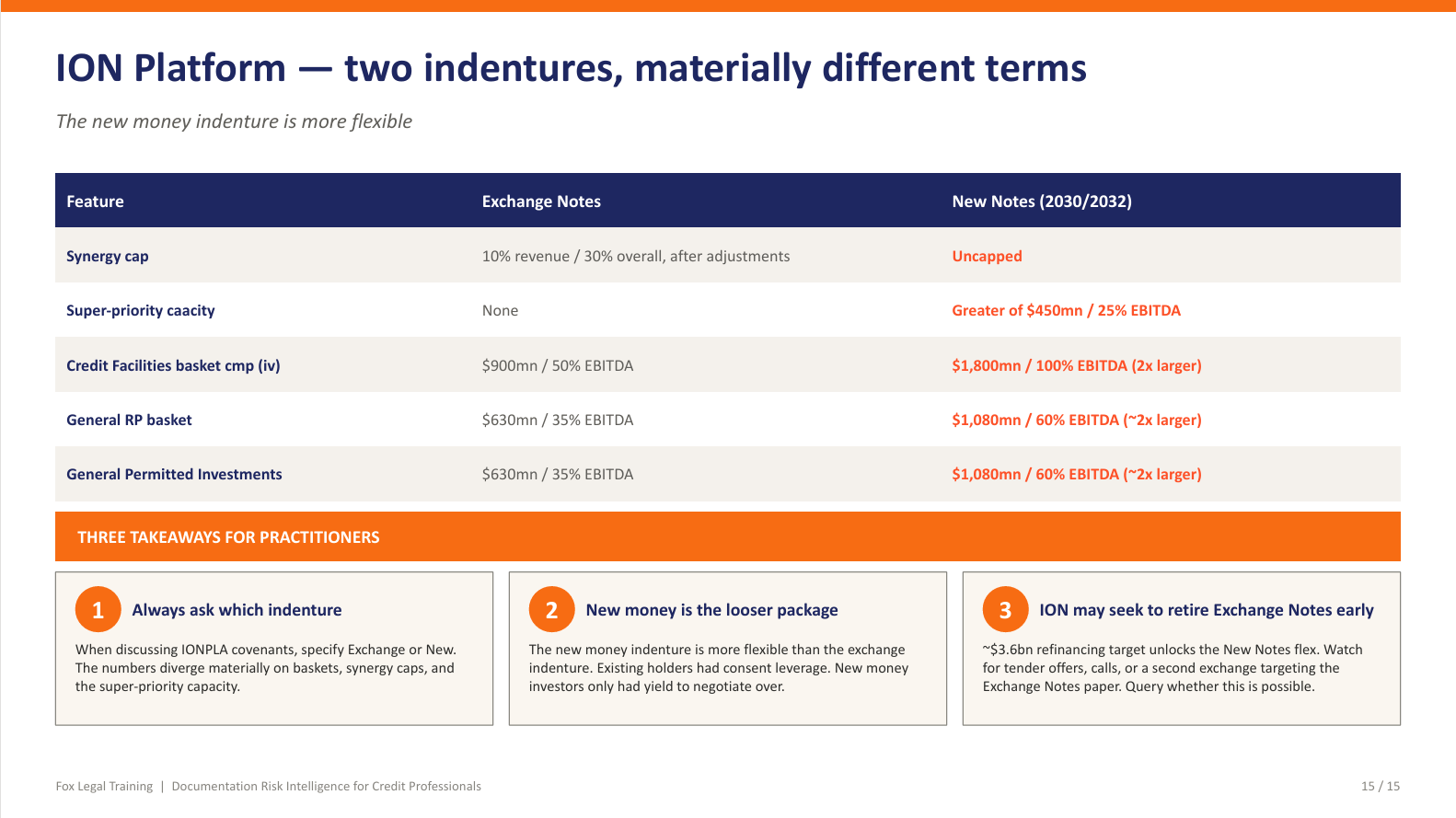

Case Study: ION Platform and the Limits of Blocker Clauses

ION Platform — a software conglomerate with a complex capital structure spanning bonds and loans — provides a real-time case study in how blocker clauses interact with LME incentives.

In September and October 2025, ION Platformexecuted a dual transaction: issuing new notes and exchange notes simultaneously, creating two distinct classes of creditors with different levels of protection. The exchange note holders had leverage — the borrower needed their consent to extend maturities — and negotiated materially tighter covenant protections. The new note holders, facing time pressure and competitive dynamics in the primary market, received a looser package.

The resulting capital structure contains a J.Crew blocker, but its scope is limited. The blocker applies only to material intellectual property, defined with reference to conducting business “in all material respects” and to the concept of material adverse effect. ION operates as a conglomerate of distinct software businesses. The question is whether transferring the IP of one business unit would constitute a transfer of “material” IP when the remaining businesses continue to operate. A reasonable argument exists that dropping a single platform would not prevent ION from conducting its business in all material respects — precisely because the remaining platforms would still function independently.

ION’s documents also predate the Xerox transaction, meaning there is no Xerox blocker — no provision preventing the JV structure that Xerox pioneered. ION could, in principle, replicate the Xerox approach. Paradoxically, the market has already begun responding: Recent new‑issue documentation is already starting to include Xerox‑style blockers, demonstrating how quickly the innovation–response cycle turns.

There is a parallel to Altice, a French TelCo, which restructured recently. Altice had one tightly covenanted tranche within its capital structure. When that tranche was refinanced in 2015–2016, the tight protections disappeared, and the borrower gained substantial additional flexibility. The lesson for ION is directional: the exchange notes — the tighter tranche — represent a constraint on the borrower’s flexibility. ION has a clear incentive to refinance or retire those notes, unlocking the full optionality embedded in the looser new note documentation.

A double-dip transaction at ION is less probable, because the intercreditor agreement contains restrictions on the subordination of intercompany debt that would complicate the mechanics. But the other avenues — drop-down via the JV route, or refinancing the tight tranche to unlock flexibility — remain available.

The Five-Line Software Credit Checklist

Sabrina provided a framework for rapid initial assessment of LME vulnerability in any software credit — a ten-minute exercise that identifies whether deeper covenant analysis is warranted.

EBITDA definition: Check the breadth of permitted addbacks and whether synergy addback caps exist. An EBITDA definition with uncapped pro-forma adjustments and wide management addback discretion inflates the denominator of every leverage-based test in the documentation, expanding capacity across all incurrence-based baskets simultaneously.

Leakage possibilities: Identify whether there are non-guarantor entities within the restricted group and whether unencumbered collateral exists that could be used as the basis for an up-tier transaction. The presence of significant assets outside the guarantor and security package is a precondition for several LME structures.

Restricted payments and permitted investments capacity: Assess the ability to move value out of the restricted group — through dividends to equity, investments in unrestricted subsidiaries, or other permitted transfers. This is the capacity that enables drop-down transactions. The relevant metrics are the builder basket, the general permitted investment basket, and any grower-based components that expand with EBITDA.

Blockers: Determine whether J.Crew blockers, Xerox blockers, or other specific anti-LME provisions exist. But blockers are not binary. A J.Crew blocker limited to “material intellectual property” provides less protection than one covering all IP. A blocker that applies only to unrestricted subsidiaries does not address the JV route. The quality and scope of the blocker matter as much as its presence.

Co-ops: Assess whether lenders are organising. Are creditor groups forming? What is the broader lender dynamic? Co-ops — formal or informal groups of lenders coordinating to protect their position — have become an essential part of the LME landscape. Their existence signals that sophisticated holders have identified risk; their absence may signal complacency.

The Blocker-LME-Blocker Cycle and What Could Break It

The evolution of LME practice follows a predictable pattern: a novel transaction exploits a gap in existing documentation, the market responds with a new blocker clause, restructuring teams find the next gap, and the cycle repeats. J.Crew prompted J.Crew blockers. Serta prompted Serta restrictions. Xerox prompted Xerox blockers. Each iteration adds complexity to documentation without eliminating the underlying incentive — which is that borrowers under stress will always seek to extend their liquidity runway, and advisors will always find mechanisms within the documentation to enable it.

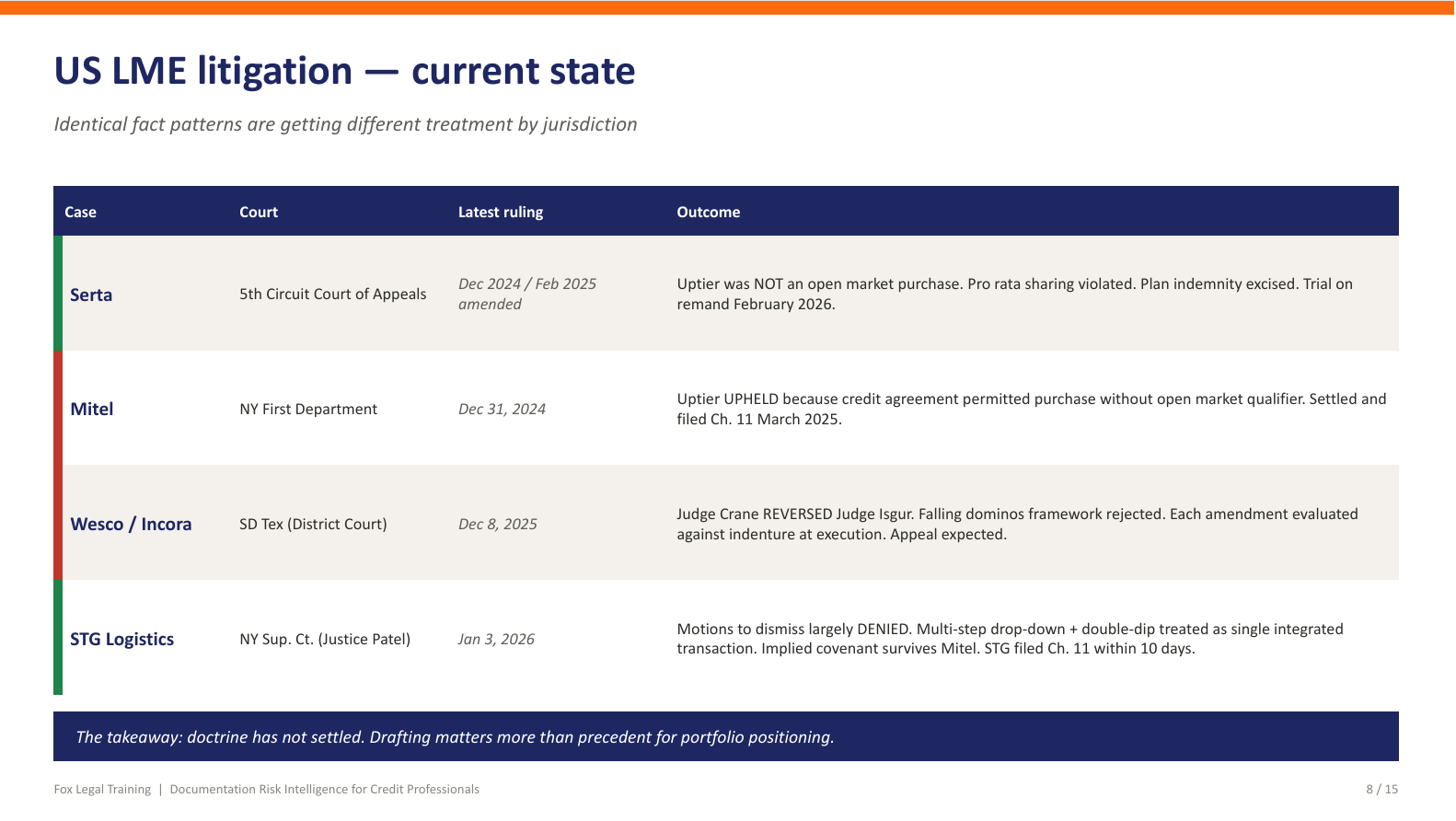

The most significant potential development for 2026 are the pending court decisions on creditor co-ops. Two cases are currently testing the legality and scope of co-op activity. If a court ruling makes lenders nervous about joining co-ops — by finding, for example, that co-op participation creates liability or violates credit agreement provisions — the consequences would be asymmetric. Borrowers would retain all their existing flexibility. Lenders would lose their primary mechanism for collective defence.

A negative ruling on co-ops “would be open season for borrowers to do LMEs.” The coordinated lender response that has, in some cases, deterred or moderated LME activity would be undermined. Individual lenders acting alone have neither the information nor the leverage to resist a well-advised borrower executing a complex restructuring transaction.

The Structural View

The analytical conclusion from this conversation is uncomfortable but clear. Software credits carry the same covenant architecture as industrial leveraged buyouts, but the asset characteristics of software businesses — concentrated IP value, portability, licensing flexibility, board-determined FMV — interact with that architecture to produce vastly more LME optionality than the documentation was designed to accommodate. The blocker clause cycle will continue to iterate, but each new blocker addresses only the last transaction, not the next one.

For software credit investors, the decisive variable in the near term is not spread or leverage — it is documentation. The five-line checklist is a starting point. The Xerox and ION case studies demonstrate that even credits with blocker clauses carry residual vulnerability. And the pending co-op litigation could remove the last meaningful check on borrower behaviour in distressed situations.

I do not think the LME wave is cresting. I think it is becoming more sophisticated. The practical question for credit investors is whether their covenant analysis has kept pace with the restructuring advisors on the other side of the table — especially in software. For most, the honest answer is no.

Listen to the full episode for Sabrina’s takes on covenants and LMEs.

This article is based on Episode 11 of Fixed + Floating, featuring Sabrina Fox of Fox Legal Training. The views expressed are those of the speakers and do not constitute investment advice. For more information, please visit https://www.foxlegaltraining.com/.

Fixed + Floating is a credit podcast for institutional investors and finance professionals — exploring the forces shaping global credit markets. Hosted by credit PM Josef Pschorn, the show features conversations with leading voices from investing, research, and academia.

Support Material: