The Auto‑Supplier Problem That Refinancing Cannot Fix — Part 2: How StaRUG and Jurisdiction Shape Restructurings

E14 – Dr. Hendrik Hauke (Willkie Farr & Gallagher) on the instruments that actually get used when operational fixes are no longer enough — and how they combine with the structural picture from Part 1.

Part 1 argued that European auto‑supplier distress is structural: capital structures sized at pre‑2020 volumes, the highest interest‑to‑EBIT ratios globally and persistent overcapacity mean that operational stabilisation does not automatically repair the credit story.

The Auto‑Supplier Problem That Refinancing Cannot Fix — Part 1: Why European Distress Is Now Structural

European auto‑supplier distress no longer looks like a cycle that will burn off on its own. Roughly a third of the supplier base sits in the distressed zone and that proportion has barely moved in two years — at levels that used to mark the bottom, not the middle, of a downturn.

This part looks at what happens when operations alone cannot carry the maturity wall — which instruments are actually being used, how they work in practice in auto suppliers, and where their limits sit in light of German law and jurisdiction choices.

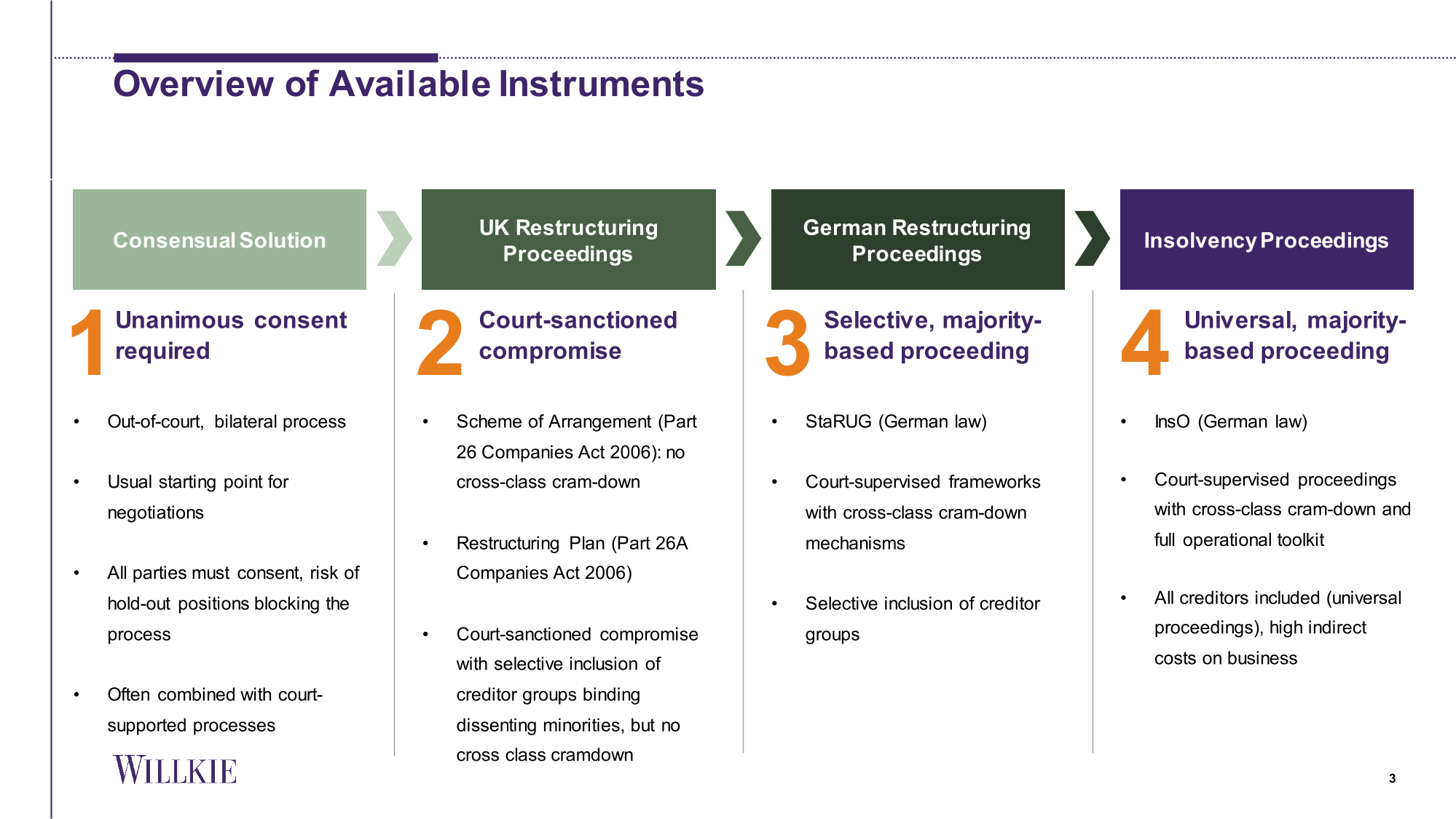

The menu of instruments

The toolkit Hauke works with runs along a spectrum:

Purely consensual, out‑of‑court deals — exchange offers, waivers, covenant amendments agreed on a contractual basis.

UK schemes and Part 26A restructuring plans — used where English law governs a meaningful portion of the debt.

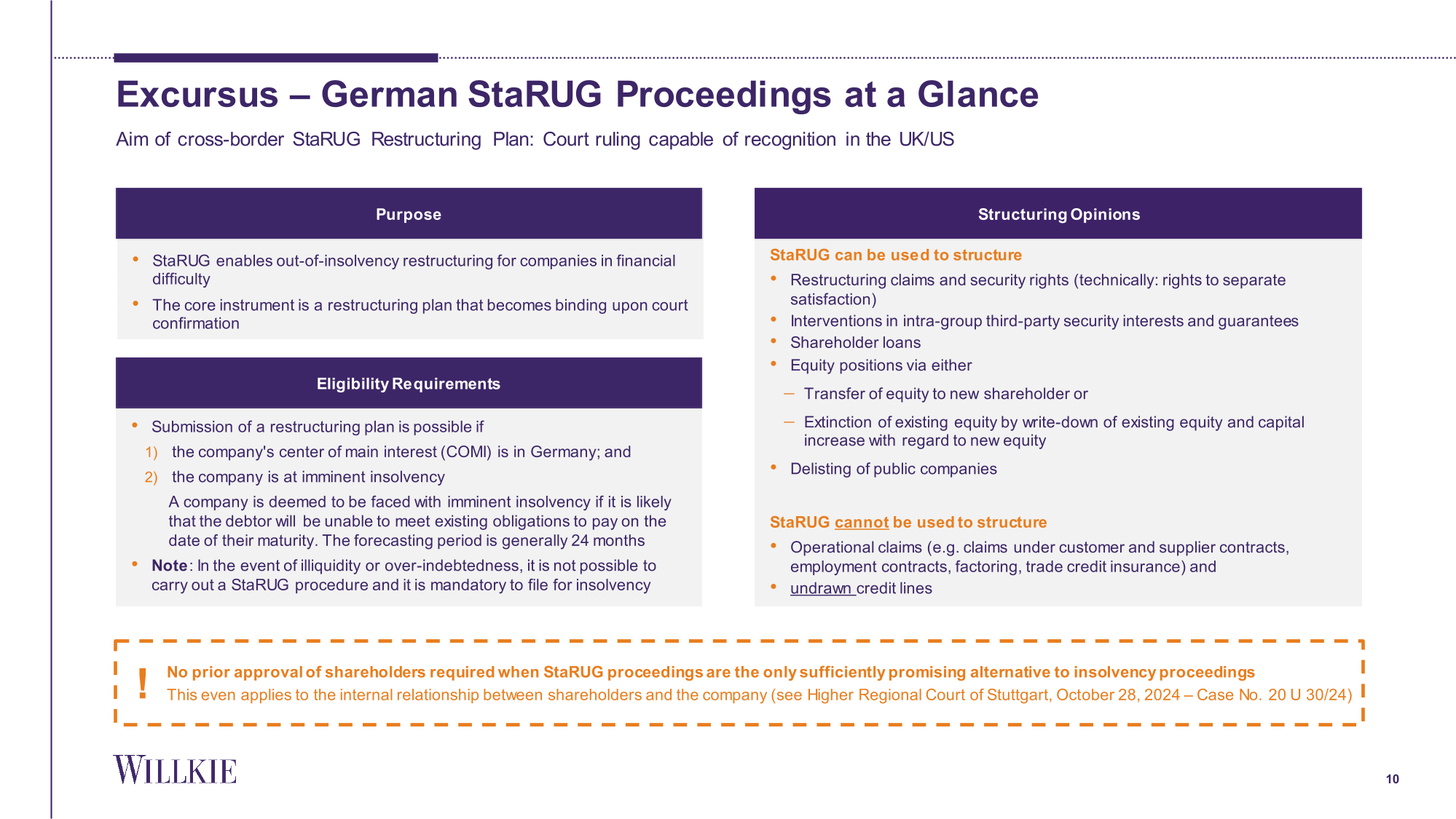

German StaRUG procedure — the preventive framework that allows a court‑supervised restructuring of financial liabilities before insolvency.

Full insolvency under InsO — when liquidity is exhausted or a going‑concern plan cannot be agreed.

Which tool fits is a function of the capital structure, not legal taste: where the liabilities sit, which law governs them, where COMI lies, how fragmented the creditor base is, what shareholders will accept and, as Hauke keeps emphasising, how much cash runway remains. A solid commercial plan can often be implemented consensually; the statutory tools become decisive when holdouts, shareholder resistance or timeline make that impossible.

LEONI: StaRUG at scale in an auto supplier

LEONI is the first large, listed auto supplier to run a full StaRUG process, and it is the template most people now have in mind. The financial restructuring covered roughly EUR 1.6bn of debt and combined three key elements:

A capital reduction to zero and subsequent capital increase of EUR 150m, subscribed solely by a vehicle of Stefan Pierer, followed by a delisting.

The transfer of around EUR 708m of bank and Schuldschein claims to that vehicle and their contribution into LEONI’s capital reserves, effectively removing those liabilities from LEONI’s balance sheet.

A recovery instrument giving former financial creditors a 45% economic participation in any value rebuild via a virtual profit‑sharing mechanism, without formal shareholding.

Existing shareholders were fully wiped; the free float of roughly 25,000 retail and institutional investors exited at zero; Pierer’s vehicle became sole shareholder. The debt stack was reduced by just over EUR 700m and the company received EUR 150m in fresh liquidity. All of this was implemented via a StaRUG plan using cross‑class cram‑down against dissenting shareholders and some creditors; appeals were dismissed and the plan is now binding.

For auto‑supplier credit, the relevance is clear. StaRUG can now be used to:

Take a listed tier‑1 private.

Wipe out equity completely.

Impose a deep haircut and equitisation structure on distributed bank and Schuldschein lenders, provided the 75% class majorities are reached.

It is a demonstrated route to a genuine deleveraging of a tier‑1 auto supplier — not just an amend‑and‑extend — but it addresses financial claims only.

What StaRUG does and does not do

StaRUG reaches financial liabilities, security packages and shareholder positions. It does not reach customer and supplier contracts, employment, leasing or most operational arrangements. It is a financial‑claims tool, not an operational one.

For an auto supplier, that distinction is central. A StaRUG plan can reset the balance sheet, change the shareholder and push out maturities, but it cannot close an unprofitable plant, exit a structurally loss‑making product line or extract the company from a bad long‑term supply contract on its own. Where the core problem is a mismatched capital structure and funding profile, StaRUG can remove the immediate financing constraint. Where the core problem is structural overcapacity and the wrong portfolio, StaRUG can only clear time and capital structure; the heavy lifting has to happen in operations via plant closures, asset sales and footprint change.

In practical credit work the question is therefore: is this a LEONI‑type situation — viable business, wrong balance sheet — or one where the economics of the portfolio and footprint do not work even after deleveraging? StaRUG is well suited to the first category. In the second, it may still be used, but only as the legal wrapper around a much more intrusive operational restructuring.

Trusteeships: holding structures for run‑offs and sales

The other instrument that appears repeatedly in German supplier cases is the double‑sided trusteeship (Treuhandlösung). A trustee holds the shares in the operating company in trust, typically with secured creditors as primary beneficiaries and former shareholders subordinated behind them.

The tool serves two main purposes in auto suppliers:

In a run‑off, it provides a neutral governance structure while the business is wound down, contracts are performed and value is distributed over time. Equity that is deep out‑of‑the‑money is effectively sidelined; creditors have an economically aligned fiduciary.

In a distressed M&A, it allows lenders to mandate a controlled sale process without becoming direct owners themselves and without being constrained by shareholder consent problems — whether a difficult controlling shareholder or a fragmented family register.

Trusteeships show up where equity is clearly out of the money, but a full insolvency is seen as value‑destructive or too disruptive to OEM supply chains. They are not a substitute for StaRUG; they are a governance and execution tool that can sit alongside StaRUG or InsO processes.

Cross‑border reach and recovery reality

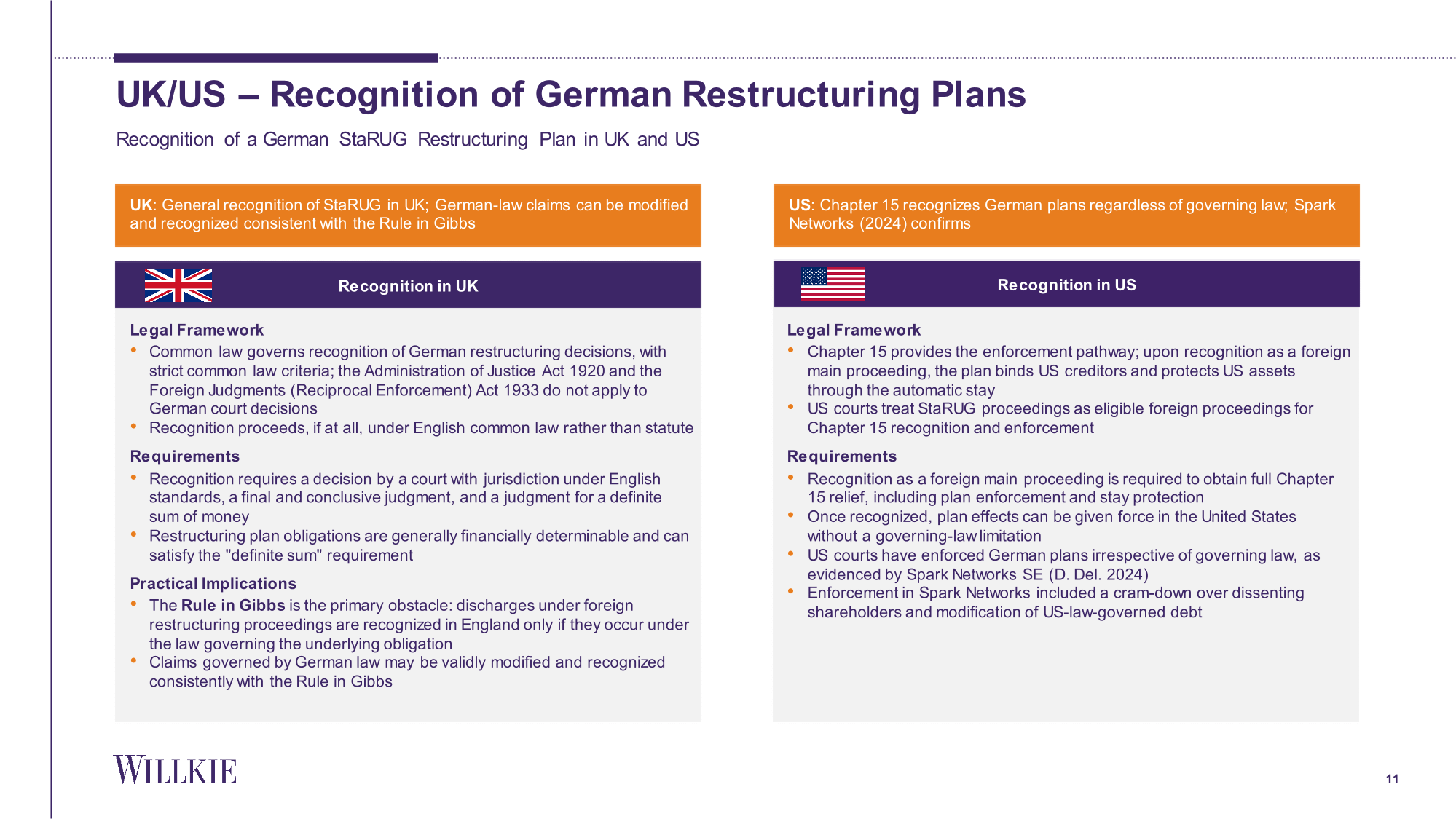

Auto suppliers are rarely purely German businesses. Plants sit in Central and Eastern Europe, Turkey, North America, sometimes China; JVs and local entities hold working capital and hard assets. StaRUG is a German tool; its effect outside Germany depends on recognition regimes.

A StaRUG plan compromising German‑law claims will generally be recognised in the UK (under the Rule in Gibbs framework for German‑law claims) and in the US via Chapter 15, as Spark Networks and other cases have shown.

It does not automatically extend into China; taking and enforcing security there is slow and uncertain; cash and value can be trapped regardless of what a German court orders.

Value sitting in non‑EU jurisdictions with weak recognition regimes (particular emerging markets) may be only partially recoverable even if headline EV looks acceptable.

For recovery analysis, the relevant question is not only “what is EV?” but “where is EV?”. A structurally important Chinese JV or Turkish plant that cannot be effectively pulled into the perimeter reduces practical recovery, even if consolidated leverage looks manageable on paper.

The creditor mix: who is in the stack and what that enables

The creditor base in German automotive has shifted away from purely house‑bank syndicates towards a mix that includes loans, bonds and Schuldscheine.

That shift is uneven:

Larger tier‑1 structures with syndicated RCFs, Schuldscheine and listed bonds — attract international restructuring capital and can support StaRUG‑type solutions with deep deleveraging and new‑money packages.

Smaller Mittelstand suppliers with €100–500m revenue and bilateral lending often sit below the threshold of interest for global funds and remain dominated by local banks, public‑sector lenders and families.

Where specialist capital is present, it changes what is feasible. Funds that bought into the capital structure at a discount can accept equity, PIK instruments and hard haircuts in order to get to a sustainable post‑restructuring profile. Traditional at‑par lenders, constrained by regulation and internal policy, often cannot. The LEONI transaction — roughly EUR 700m of liabilities removed, EUR 150m of new equity, equity wiped, sole new shareholder — is the size of adjustment that typically requires that kind of capital.

Where specialist capital is not present, and bank groups are unwilling or unable to accept that depth of write‑down, the pattern tends to be tighter: smaller amendments, more incremental covenant fixes and a higher probability that the name returns to the workout list when the next shock hits. The legal toolkit is the same; the willingness and ability to use the full extent of it is not.

How I read restructuring choices in auto suppliers (Part 2)

1. Where in the structure the restructuring is run — German OpCo versus holdco / foreign finance entity. A piece i have coauthored lays out the perimeter problem: once a restructuring reaches a German operating entity as issuer or guarantor, director duties, capital maintenance rules, the worse‑off test and IDW S6 bound the economic outcome tightly. At that level, StaRUG and InsO transactions are constrained to a corridor between insolvency‑floor recoveries and what a going‑concern opinion will support; aggressive creditor‑on‑creditor outcomes are the exception, not the rule. By contrast, where debt sits at a Luxembourg or Dutch holdco and German entities are only indirectly involved, US Chapter 11, UK plans or WHOA can still be used to implement materially non‑pro‑rata trades without immediately triggering German filing obligations. In auto suppliers, that split decides whether a case feels like a German corridor‑type process or more like an offshore capital‑structure trade.

2. Whether the problem is “only” financial, or structurally operational — which determines whether StaRUG is enough. StaRUG works best when the business model is still viable and the issue is a balance sheet sized for a different world: LEONI is the clean example. There, the plan combined an equity wipe, c. EUR 700m of debt removal and EUR 150m of new money, followed by a delisting — a genuine balance‑sheet reset for a business that still has a role in future supply chains. Where the core issue is structural overcapacity, a fundamentally wrong portfolio, or a footprint that cannot be made economic, StaRUG can only clear time and capital structure. The decisive question then is not “StaRUG versus insolvency”, but whether the operational changes that are actually needed — plant closures, exits, asset sales — are being executed alongside the legal process.

3. Who sits in the creditor stack and which tools that actually makes usable. For larger tier‑1 structures with bonds, Schuldscheine and international lenders, StaRUG combined with new money from special‑situations funds can deliver LEONI‑style deleveraging — deep write‑downs, equitisation, new control owner and a clean runway. For mid‑market suppliers dominated by local banks and statutory German‑law bonds (SchVG), the tools and economics look different: German bond law hardwires pro‑rata outcomes; bank groups are more constrained on haircuts; restructurings tend to be earlier, more incremental and more consensus‑driven. Overlaying that with the perimeter question from point 1, the pattern is simple: if the capital structure is small, German‑centric and issued at OpCo, expect corridor‑type outcomes. If the structure sits above Germany, has foreign‑law instruments and has specialist capital in the book, more aggressive, documentation‑driven solutions are on the table — but usually only as long as the German entities have not yet tripped into their own filing obligations.

Taken together, Parts 1 and 2 describe one problem: European auto suppliers are running with too much capacity and the wrong portfolios into a world where capital is scarcer and cheaper competitors are setting the price. The operational and legal toolkits can fix that, but only when they are used together and only at the cost of real capacity and equity.

Listen to the full episode for Daniel’s and Hendrik’s takes on auto suppliers.

This article is based on Episode 14 of Fixed + Floating, featuring Daniel Steiner of PwC and Dr. Hendrik Hauke of Willkie Farr & Gallagher. The views expressed are those of the speakers and do not constitute investment advice. For more information, please visit https://www.pwc.de and https://www.willkie.com.

Fixed + Floating is a credit podcast for institutional investors and finance professionals — exploring the forces shaping global credit markets. Hosted by credit PM Josef Pschorn, the show features conversations with leading voices from investing, research, and academia.exploring the forces shaping global credit markets. Hosted by credit PM Josef Pschorn, the show features conversations with leading voices from investing, research, and academia.

Support Material: